Walgreens is set to report their fiscal Q2 ’24 financial results before the opening bell tomorrow morning, Thursday, March 28th, 2024. Analyst consensus is expecting $38.9 billion in revenue, $672 million in operating income and $0.82 in EPS, resulting in +3%, – 45% and -29% yoy growth for the three metrics.

Rather than bury the lede, here’s what’s fascinating about Walgreens: WBA revenue has shown almost no degradation since the stock price collapsed, with most of the weakness coming from negative EPS estimate revisions:

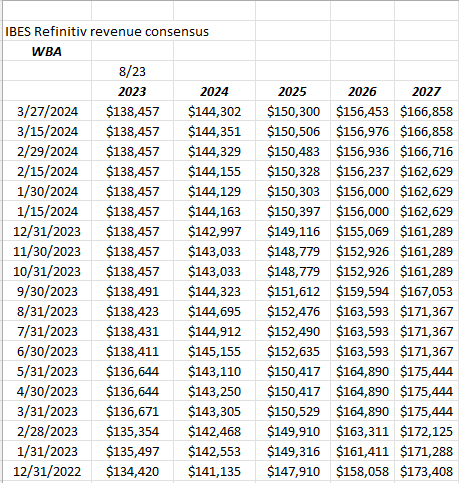

WBA revenue estimate trend:

Source: LSEG

Note how WBA’s revenue estimates have actually trended a little higher in fiscal ’24 over the last 15 months, as has fiscal ’25. Fiscal ’26 and ’27 have weakened a little but that could be from planned divestitures and the downsizing of WBA’s business.

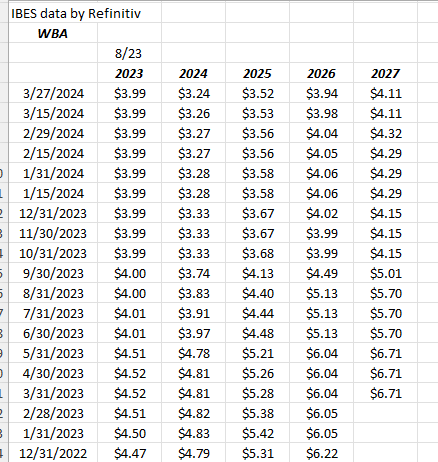

WBA EPS estimate trend:

WBA’s EPS is not so lucky, unfortunately. The pressure is a margin issue and could be from the scattered business model strategy of Steffano Pessina the last 10 years, and the leadership of Roz Brewer, who never seemed to be able to communicate any enthusiasm for the business, or even a viable path forward for the various aspects of the business.

Tim Wentworth – WBA’s new CEO – on the other hand is moving quickly: in the early Jan ’24 conference call ( fiscal Q1 ’24 results), Wentworth reiterated the $1 bl projected cost savings, the $600 ml in capex reduction, (which will help free-cash-flow), and the $500 million in projected working capital improvement (which will help cash-flow).

The US Healthcare segment, which was Roz Brewer’s baby (or so it seemed) was expected to show significant year-on-year profit improvement in fiscal ’24, per the conference call notes.

The ironic aspect to WBA is that the US Retail Pharmacy biz appears to be in good shape: in Q1 ’24, the US retail comp’s increased +8.1% yoy, although retail sales fell 6% and front-end comp’s – a metric I used to watch closely in Walgreens better days – fell 5%. This tells us, while the retail drug store giant is still generating foot traffic in the store, there is less “convenience” buying of traditional retail convenience items, i.e. milk, cereal, ice cream, etc. (although I still do my part with the ice cream).

Do Amazon’s PillPack and CostPlus represent a threat to WBA’s scrip biz ? You’d certainly have to think so, at least eventually, but there doesn’t seem to be the pressure yet, given the continued increase in revenue estimates.

The most troubling valuation metric WBA’s “price-to-revenue” or price-to-sales metric at 0.12x. That’s lower than when Sears Holdings was taken out, or when Michael Dell took Dell private in the early 2000’s.

At 6x expected ’24 EPS and expected 4% revenue growth over the next 3 years, WBA is on pretty thin ice. There is a little cash-flow and not much free-cash-flow, but I suspect Tim Wentworth is going to try and improve these metrics over the next 6 – 9 months, and see if WBA can improve it’s cost structure and margins.

If forward revenue estimates remain stable, and the EPS is declining as it is, the math tells you it’s a margin, or cost structure problem.

Summary / conclusion: If you’d talk to most retail equity analysts, they’d tell you, as long as a retailer is generating considerable revenue and it’s not declining, the stock has a fighting chance. Some are comparing WBA to Bed, Bath & Beyond, which looked good for a while even as the stock price fell from the $40’s to the $20’s, but Walgreens front-end and scrip business is “essential use” and is still generating foot traffic, while Bed, Bath had business model that could be replicated by anyone.

One time asset liquidations and asset divestitures at WBA are a plus for now, but the business needs to stabilize margins and eventually improve operating income on a reliable basis.

Another positive is that Standard & Poors still rates Walgreens senior unsecured debt at A-, while Moody’s rates the senior unsecured debt of WBA at A1. Truthfully, I expected those credit ratings to be lower.

Technically, a close below $19 on heavy volume for WBA would not be a good thing. The 52-week low for the stock is $19.58. Use $19 for a stop-loss for readers that own the stock.

A few clients are long the stock between $21 – $23, but it’s not a big position. To own more stock, I would need to see the EPS estimates stabilize and even better, move higher. That would tell me earnings are more in line with revenue.

Tim Wentworth has has work cut out for him. The next few quarters are critical. The positive is he is moving quickly.

None of this is advice or a recommendation. Past performance is no guarantee of future results. Investing can involve loss of principal even over short periods of time.

Thanks for reading.