It’s hard to think of a more out-of-favor stock coming into Q4 ’23 earnings season than Boeing (BA), with Boeing is scheduled to report their calendar Q4 ’23 financial results before the opening bell on Wednesday, January 31 ’24. Even if the EPS estimate of a loss of ($0.78) and the revenue estimate of $21.1 billion are beaten, much will depend on the conference call, and order cancellations (if any) and whether the original ’25 – ’26 cash-flow and production story is still intact.

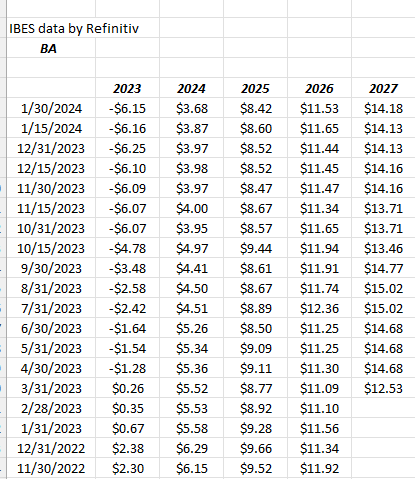

Let’s look at Boeing’s EPS and estimate revisions:

Personally, I think BA’s earnings estimates are meaningless here given the losses in 2023, and while 2024 EPS estimates are still expected to be positive, the 2024 EPS estimate has lost more than half its value in the last 12 – 14 months.

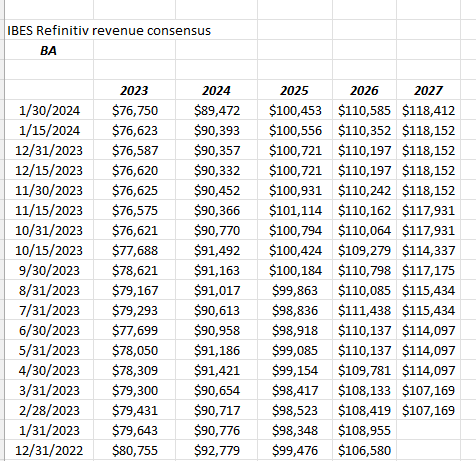

What might be worth focusing on is BA’s revenue estimates and revisions for ’24 – ’26 since the changes will tell us the degree of order cancellations for BA planes, and whether the headlines and the press coverage is far more dire than the reality of the situation.

Note how even after the Alaska Air fiasco and press coverage, the 2024 revenue estimate remains in the $100 ml range the last 4 months, and the 2025 revenue estimate has ticked slightly higher.

That data being said, it’s small consolation.

Boeing summary / conclusion: The ramp in the BA’s stock from November 1 around $180 to the end of 2023’s $260 print, was truly remarkable to behold, and then Alaska Air door flying off mid-flight, and the other mid-flight incidences, caused investors to think, “same old Boeing” much like Detroit Lions fans lamented after Sunday’s NFC Championship.

There appears to be good support for the stock in the $200 area, which is the area of the 200-week moving average, although that average looks wobbly, as it’s pointing lower, so how the stock trades after earnings tomorrow, relative to the headlines and management commentary will matter much.

Boeing’s undeniable strength is it’s competitive position and the oligopolistic nature of the aircraft manufacturing industry. There are only three companies capable of BA’s manufacturing prowess of producing 50 planes a month, and those are Airbus and COMAC, which is the Chinese competitor, and I’m not sure Comac is a viable alternative to either Boeing or AirBus.

Another positive for BA’s prospects is that according to a trusted corporate bond manager source, Boeing’s corporate credits (corporate bonds) aren’t showing any duress or unusual trading pressure as of this week, even with the latest news.

Boeing was always going to be a ’25 – ’26 cash-flow story per the Street consensus and per the conference call notes from Q3 ’23, the goal for BA was to be on track to produce 50 planes a month by ’25 – ’26, so the first thing to watch is to see if there is a material change to that production schedule tomorrow. Let’s see how ’25 – ’26 revenue estimates change – if at all – after tomorrow’s earnings release.

Like Tesla last week, it’s hard to think of a worse media and sentiment environment within which Boeing will report earnings, so the calculation is how much of the endless string of bad news is discounted in the stock price, versus how many airlines can or will cancel forward airline orders.

Morningstar has a fair value on the stock of $232 and quantifies the manufacturing defects at between $1 – and $32 per share, which would leave the new fair value at $200 or where the stock is trading today, under a worst-case scenario.

Clients have a 1.5% – 1.6% position in the stock, and this position will likely be held until after earnings are seen tomorrow morning, and the research has been vetted.

Boeing is a “play the long game” stock, particularly in a market being driven by the mega-caps and the high end of the SP 500. It’s tough to buy a stock like this in front of earnings, given the unknowns, and what else may be disclosed.

Clients are long a 1.5% position in the stock and it will be held at least until Q4 ’23 results are seen and digested.

None of this is advice or a recommendation. Past performance is no guarantee or suggestion of future results. Investing can involve the loss of principal. Earnings releases can trigger bigger moves in a stock price, both up and down, so be careful about buying stocks in front of earnings. Readers should gauge your own appetite with market volatility and adjust your portfolio accordingly.

Thanks for reading.