Microsoft (MSFT) and Alphabet (GOOG / GOOGL) report after the closing bell on Tuesday, January 30 ’24.

Microsoft (MSFT): Microsoft reports their fiscal Q2 ’24 financial results after the closing bell on Tuesday, January 30 ’24, with sell-side consensus expecting $2.78 in earnings per share (EPS) on $54.5 billion in revenue for expected yoy growth of 26% and 3% respectively. (It needs to be noted and highlighted to readers that Briefing.com’s estimates show an expectation of $2.77 in EPS on a revenue estimate of $61.14 billion. That is a $7 billion estimate difference in MSFT’s expected Q2 ’24 revenue and it’s a material difference. Another estimate source is also showing $56.5 billion for the Dec ’23 quarter.)

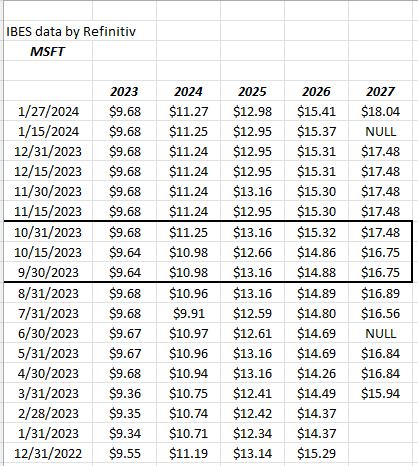

This table shows MSFT’s EPS revisions for the last 12 months, with the bordered block noting the revisions following the October ’23 earnings release.

Readers can see the ’24 – ’26 EPS estimates creep higher, with the exception of ’25.

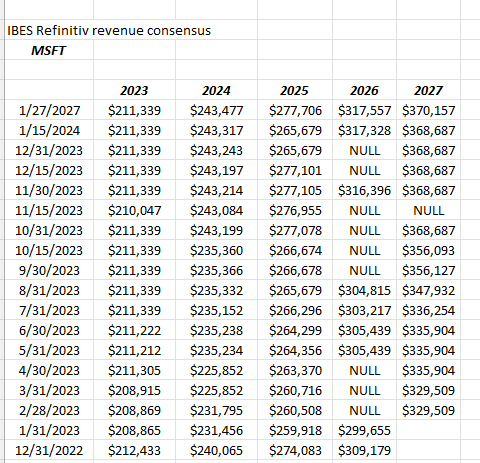

MSFT revenue revisions also saw a nice bump after the October ’23 financial release, with expected ’24 revenue for MSFT increasing about $8 billion for fiscal ’24.

Valuation: at $403 per share (up from $335 as of the October ’23 earnings release), MSFT is trading at 36x the expected ’24 EPS estimate of $11.27 and 31x the ’25 estimate, with yoy growth expected at 15% and 16% respectively for the software giant. The cash-flow valuation is about as expensive, maybe a little more, but “ex-cash” (balance sheet cash) MSFT is trading at 30x and 46x trailing-twelve-month cash-flow and FCF numbers. MSFT’s cash balance was $143 billion as of the Oct ’23 quarter which is about 4% – 5% of MSFT’s market cap.

Someone put out a note this week on the cash-flow generation of the mega-cap tech names, and you have to wonder where they’ve been. Apple’s trailing-twelve-month free-cash-flow is about $100 billion, while MSFT’s as of the October ’23 quarter is $62 – $63 billion, which is a little depressed after the Activision acquisition, (acquisitions are added to capex), but free-cash-flow should continue to improve yoy in fiscal ’24 as ATVI washes through the financials.

The difference in Apple and Microsoft is Apple spends about 3% of it’s market cap on share repurchases while Microsoft’s repo’s are just 1% of MSFT’s market cap. (More will be forthcoming on Apple before they report this week.)

MSFT summary: MSFT broke above it’s 2021 high of $350 in 2023, long before the SP 500 did last Friday, January 19th, which is a technical positive. Fundamentally, my own opinion this quarter is that the focus will be on CoPilot, MSFT’s AI product which launched November 1 ’23, and how that is evolving after 8 weeks in fiscal Q2 ’24 and then again in the first 4 weeks of calendar ’24. Investors will like to see metrics, after the industry hype, but my guess is MSFT will try and shield the numbers, but will disclose growth.

MSFT guided to 26% – 27% Azure growth in fiscal Q2 ’24 (Azure and CoPilot, are part of MSFT’s Intelligent Cloud segment) after Azure grew 28% in the first quarter , and MSFT also guided for flat margins in fiscal ’24 thanks to Activision’s acquisition and possibly some margin pressure thanks to an accounting change (maybe that explains the revenue estimate difference), so the quarter could be noisy on Tuesday night.

There is always something to worry about with any position, so MSFT’s return both in ’23 and YTD, and it’s valuation, might have outrun the reality of AI growth, given all the hype since some analysts are commenting that “AI is bigger than the internet”.

Microsoft has been clients top stock weighting beginning in 2013, and remains so at present.

Alphabet: (GOOG/GOOGL): Q4 ’22 was Alphabet’s weakest quarter since June ’20

Alphabet also reports after the close on Tuesday night, January 30, ’24 after the close. Consensus estimates are looking for $1.59 in EPS on $85.3 billion in revenue for expected yoy growth of 51% and 12% respectively. (December ’22 was a particularly weak quarter for Alphabet, hence the growth might look a little stronger than expected.)

The search giant has a very weak compare against December ’22’s quarter.

Alphabet’s big problem in Q3 ’23 was Google Cloud growth and it’s rather small margin as percentage of Alphabet’s total operating income. GOOGL traded all the way down from $140 to $120 following the October ’23’s earnings release.

Personally I’ve always felt that if search was fine, then the core Alphabet business model was safe, but with Microsoft and their lead in AI, particularly with the seeming ascension of Bing, and the potential disruption of search, maybe it puts GOOGL on somewhat less firmer footing ?

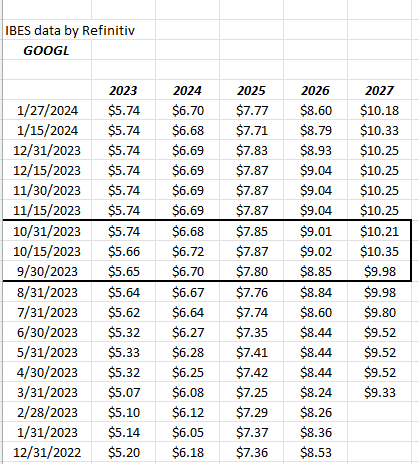

Readers can see with the EPS revisions the April ’23 and July ’23 earnings release saw higher EPS revisions, until the October ’23 release which saw some caution in the EPS numbers.

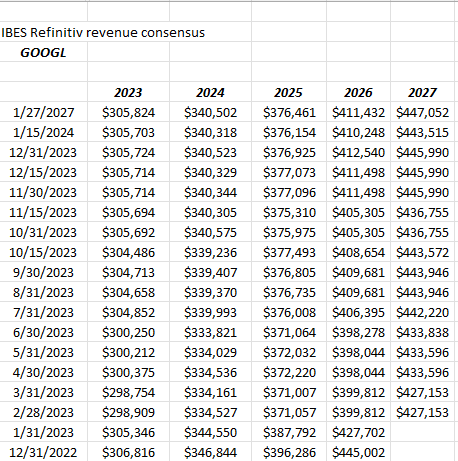

2023 revenue estimates have remained relatively stable but 2025 and 2026 estimates have been have fallen 5% and 8% respectively in the last 12 months. Let’s see if Alphabet can reverse that trend this week.

![]()

This last table shows the slowing yoy revenue growth for many of Alphabet’s segments, particularly Google Cloud. Google Cloud’s revenue growth has slowed sequentially almost every quarter since June ’22.

Google Cloud is supposedly #3 and well behind Amazon’s AWS and Microsoft’s Azure – can it be a viable competitor within the cloud space ?

Valuation: Looking at ’24 – ’26 EPS estimates GOOGL is trading at 23x ’24 EPS with an expected growth rate the next three years if 16%. The stock is not expensive on PE-to-growth basis, but this may be explained by the expected slowing of revenue estimates. Like Microsoft, GOOGL has $120 billion of cash on the balance sheet and thus “ex-cash” the cash-flow and free-cash valuations are 13x and 18x respectively.

Looking at the bigger picture perspective, Alphabet entered 2022 with +20% revenue growth, and then advertising slowed and revenue growth slowed sequentially bottoming in Q4 ’22 and Q1 ’23 at +1% and 3% y.y revenue growth, and now revenue has started growing again.

Here’s how 2024’s EPS estimate has trended the last 5 quarters:

- Current as of 1/27: $6.70

- Sept ’23: $6.65

- June ’23: $6.66

- March ’23: $6.22

- Dec ’22: $6.12

Alphabet summary: GOOGL remains a top 10 holding. Advertising is the straw that stirs the drink (so to speak), with yoy advertising growth weakening considerably in late ’22 and early ’23, thus the segment has easy compares and the search company is gradually growing revenue once again in ’23. GOOGL’s stock ticked to an all-time-high late last week, but needs to break out firmly from the low $150’s.

Most of the Street would think Alphabet is an AI beneficiary, but there will be winners and losers that we don’t expect.

None of this is advice or a recommendation. Past performance is no guarantee or suggestion of future results. All EPS and revenue estimates are sourced from LSEG (London Stock Exchange Group, which was formerly Refinitiv, which was once Thomson Reuters and First Call.)

Thanks for reading.