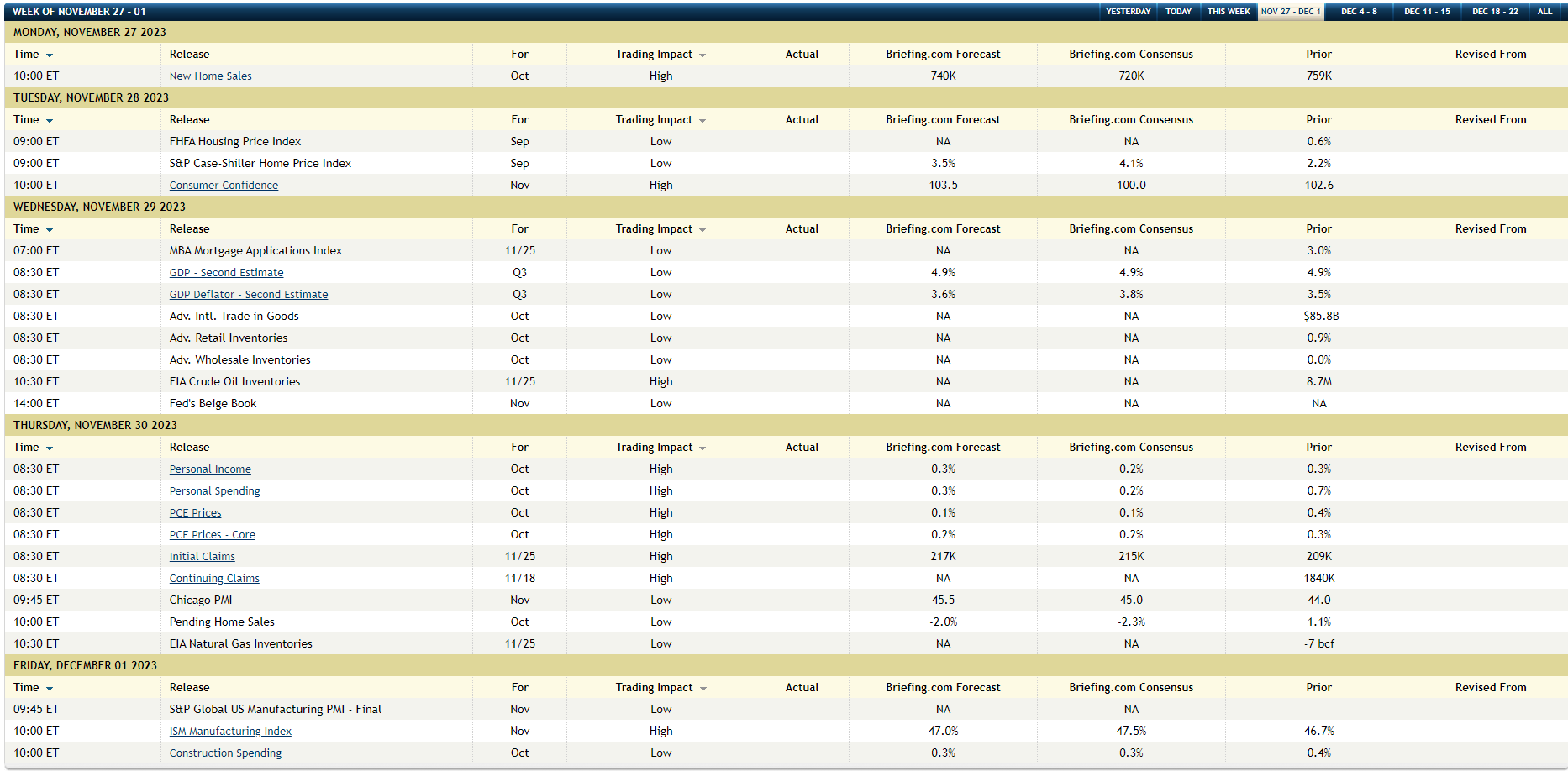

For this post-Thanksgiving week, the important economic release is the October PCE and PCE Core data coming out Thursday morning, November 30 ’23.

GDP data for Q3 ’23 is also scheduled for release on Wednesday, November 29th, but the markets are typically worried about what’s ahead, and the development of the Fed “Nowcast” models and their growing acceptance, indicates Q4 ’23 GDP has already slowed from the white-hot Q3 ’23 pace of +4% to the more acceptable 2% – 2.5% range expected for Q4 ’23 (which is subject to constant change), although there can be a lot of variance between those regional Fed Nowcast model forecasts.

Attached above is the Briefing.com template which shows the coming economic data this week. Briefing does a good job of detailing the estimates and looking at the expectations for October PCE and PCE Core data, the +0.1% and the +0.2% (PCE Core) estimates are quite subdued, particularly given the September actuals of +0.4% and +0.3%, and if those estimates are hit on Thursday morning, I think it’s reasonable to expect another positive market reaction, as we saw with October CPI data two weeks ago.

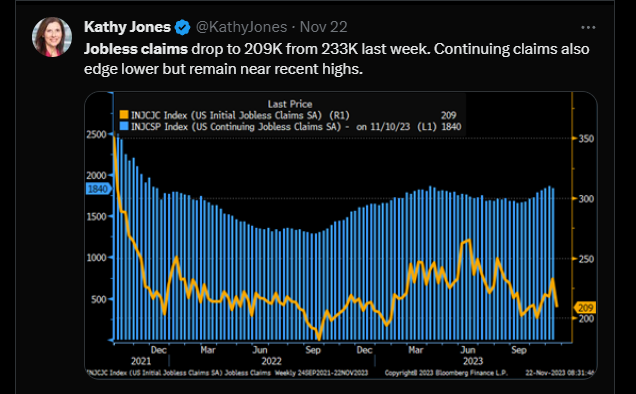

The fly in the ointment once again continues to be jobless claims. Perhaps the UAW strike had some influence on the data, but jobless claims jumped to the 250,000 in the last 4 – 5 weeks, but have now come down (rather sharply I might add) again to the 209,000 range, with last Wednesday morning’s report.

Kathy Jones, Schwab’s Chief fixed-income strategist, put up this graph last Wednesday, November 22nd after the pre-Thanksgiving release of the jobless claims data. Continuing claims are more supportive of a bottom in bonds, but that sharp downward spike in weekly claims always makes me nervous.

While the unemployment rate has risen off it’s lows, the persistence of jobless claims in the low 200,000’s tells me the job market is still pretty healthy.

SP 500 earning this week:

While there has been a sharp decline in the expected Q4 ’23 SP 500 EPS growth rate from 12.7% on 9/30/23 to 5.4% on 11/24/23, this is less worrisome given the y.y compare with Q4 ’22. This was discussed on this week’s earnings update posted to this blog on Saturday, 11/25/23.

Q4 ’22 SP 500 EPS results were pretty grim. That leaves me more sanguine about any decline in the expected Q4 ’23 growth rates today.

SP 500 data:

- The forward 4-quarter SP 500 EPS was $235.82 this week, versus $235.95 last week and 9/30/23’s $232.95;

- The PE ratio on the forward estimate is 19.3x versus last week’s 19.1x and late October’s 17.3x;

- The SP 500 earnings yield is down to 5.17%, which is getting into the “overbought” area;

SP 500 earnings this week:

- Crowdstrike (CRWD) and Workday (WDAY) report Tuesday, 11/28 after the close;

- Foot Locker (FL) report Wednesday, 11/29/23 before the open. It will give readers some insight into Nike’s 12/21 scheduled earnings release;

- SalesForce (CRM) and SnowFlake (SNOW) report Wednesday after the close;

- Kroger (KR) reports Thursday.

One client had a small position in Palo Alto Networks (PANW) that reported earnings about 10 days ago, the stock sold off after earnings and the day following, and then rallied hard in the last week. Cyber-security is an area of interest but I’ve just started following the sector and getting to know the companies. Crowdstrike (CRWD) is another cyber-security or network security firm reporting this week, so it will be interesting to read the notes and see how the stock trades following earnings.

Nvidia (NVDA) has lost all it’s momentum, probably thanks to the China issue. That’s probably not a bad thing either (i.e. less frenzied momentum trading. (Clients are long NVDA through it’s 20% weight in the VanEck Semiconductor ETF (SMH).

Secular bull market question:

The SP 500 has not made a new high since the first trading day of January ’22, while the Nasdaq peaked in late November ’21 near 16,200.

Secular bull markets run in cycles, i.e. 1945 to 1965’ish, 1970, (back then it was more the Dow than the SP 500 that got the attention), and then 1982 – March, 2000, and now 2010 to the present day.

Did this current secular bull market start on March 9, 2009, or did it really begin when the SP 500 made a new all-time-high in early May, 2013 ?

What’s fascinated me over the years is how the US economy has changed from post WW II to today. Manufacturing was 50% – 60% of total GDP in the mid 1940’s and most economist back then thought we’d see a 2nd Great Depression after WW ended. The GI Bill really stimulated college attendance after the end of WW II, and aided the growth in the “services” economy within the US, but the service aspect of the US economy didn’t exceed manufacturing as a bigger share of the “private sector” until the 1970’s and then rocketed higher with the advent of the “technology” economy beginning with the 1980’s.

From just “watching the clock” so to speak, the time frame of this bull market leaves me more cautious, but here’s what I think about when formulating the bullish case:

- The decade from 2000 to 2009 was the worst decade for stock returns (i.e. the SP 500) since the 1930’s or the Great Depression.

- The “annual return” for the SP 500 from 2000 to 2009 was just 1.25%, it’s lowest decade return since the 1930’s negative return.

- Between 1945 and 1999, there was only one 50% correction in the SP 500, and that was the 1973 – 1974 bear market (the SP 500 fell 45% – 50%) and that was around the time of the Arab Oil Embargo, the Vietnam War, Watergate, and former President Richard Nixon’s resignation.

- Between 2000 and 2009, investors experienced two declines in the SP 500 of 45% – 50%, the first being the 2001 – 2002 bear market, and then the 2008 bear market, both for entirely different reasons which won’t be talked about now;

- After thinking about it for years, following 2008, both the 1930’s and the 2000’s decade were marked by significant “deflation”. I still think Jay Powell and the Federal Reserve, (deep in the bowels in the NY Fed) wanted – and were happy to see – the inflation spike driven by Covid in 2021, since inflation is far less damaging than deflation (and the subsequent liquidity trap the US economy experienced after 2008) marking a return to a somewhat-normal US economy and business cycle. (Ben Carlson or Ritzholz Wealth Management wrote a similar article around mid-November ’24, which is another perspective on the same topic. It was a good article on a topic not well understood by even a majority of folks in the investment business. Think Japan after the Nikkei peaked in 1989 and only made it’s first new all-time-high in the last month. )

It’s for these reasons I do think this secular bull market we are in, can last longer than the typical cycle, if only because 2000 to 2009 was so off-the-charts ugly from an economics perspective but readers should also know that – like this current 2-year correction we are in with both bonds and stocks under water since late 2021, early 2002, we could see periods like this where returns remain sub-par for years.

Updated annual returns will be posted after November 30th, but from January 1, 2000 to to October 31 ’23, the “annual return” on the SP 500 is just 6.49%.

It’s always a good debate, but thinking about this market today, it’s nothing like the frenzy of 1995 -1999, or rather March, 2000.

Like the good country lawyer said, “It could be argued either way”.

Anyway, none of this advice, a forecast or a prediction. Past performance is no guarantee of future results. All SP 500 EPS and revenue data is sourced from IBES data by Refinitiv.

Thanks for reading.