Nvidia (NVDA) is the big earnings report forthcoming this week, as the AI chip giant will report it’s fiscal Q3 ’24 after the bell on Tuesday night, 11/21/23.

Clients have no direct position in NVDA, but own it indirectly in the SMH or the VanEck Semiconductor ETF. NVDA is the #1 weight in the SMH at 20% of the ETF’s market cap. Taiwan Semi is #2 at 12% of the ETF.

Social media was all “atwitter” (no pun intended) this week about the potential breakout in the SMH. You’d have to think a lot of that breakout (or breakdown) would be a function on NVDA’s fiscal Q3 ’24’s financial results Tuesday night, and the guidance given for Q4 ’24 and potentially fiscal ’25.

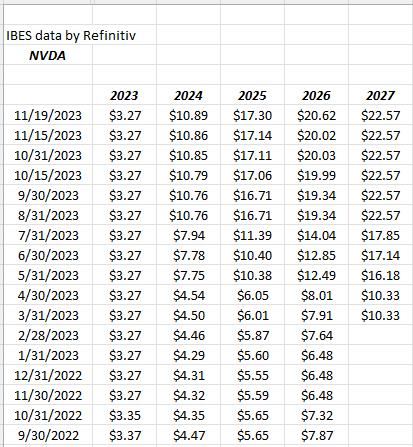

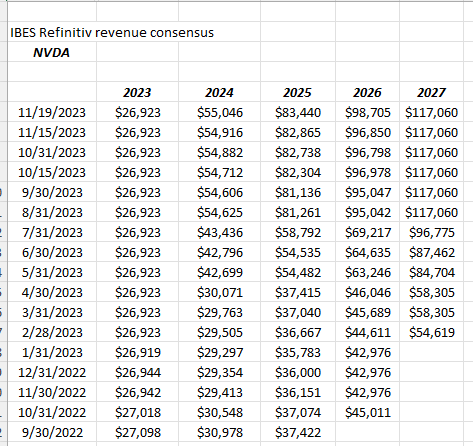

Here’s NVDA’s EPS and revenue revisions:

Note the big increase in EPS and revenue estimate revisions in both May ’23 and August ’23, the months when NVDA previously reported.

Those are huge estimate revisions (pardon the hyperbole).

This blog has no opinion on the stock or the EPS / revenue momentum.

—————

Refinitiv is now publishing small-cap EPS estimates as of last week. Reach out to tajinder.dhillon@lseg.com if you’re interested in the estimate data.

What’s interesting to me about the Russell 2000 data is that while technology is 27% of the SP 500 by market cap, and the SP 500’s largest sector, for the Russell 2000, the industrial sector is the largest market cap weight at 20%, while the financial sector is 17.7%.

The financial stocks – large cap – had a good week this week, with JP Morgan (JPM), rose +4.4%, Charles Schwab (SCHW) rose +4.4%, Bank of America (BAC, rose +8.31%, Goldman Sachs (GS) rose +4.2%, the KRE (regional bank ETF) rose +9.28%, and well, you get the picture.

With the Fed / FOMC / Jay Powell now on hold in terms of monetary policy, is the financial sector anticipating a future rate cut ? It’s still too early to know since year-over-year (y.y) core CPI was still 4%, but financial stocks much prefer a normally-sloped yield curve (short end yields below longer-maturity yields), and will start to move well in front of an actual interest rate reduction.

The top 4 Russell 2000 sectors by market-cap weight (per the Refinitiv data):

- Industrials: 20%;

- Financials 17.7%;

- Health Care: 14.6%;

- Technology: 11.6%;

- Total: 63.9%

Top 4 sectors in SP 500 by market-cap weight:

- Technology: 29.3%

- Financials: 12.8%

- Health Care: 12.6%

- Consumer Discretionary: 10.7%

- Total: 65.4%

SP 500 data:

- The forward 4-quarter estimate (FFQE) slipped to $235.95 from last week’s $236.29;

- The PE ratio on the forward estimate is 19.1x versus the 18.3x last week thanks to 2.25% gain in the SP 500 this week;

- The SP 500 earnings yield ended this week at 5.23% versus the prior week’s 5.35%

- The SP 500 EPS “upside surprise” (or beat rate) is still +7.1% at the end of this week;

Summary / conclusion: The 10% gain in the SP 500 since late October ’23, has brought the SP 500 earnings yield down to the low 5% area (again), which is where it was in late July, early August ’23. There is no perfect timing indicator for the SP 500, but the SP 500 earnings yield is both a red and green flag when it gets to certain levels.

This blog will be out with some comments shortly on the Walmart quarter reported Thursday morning, 11/16. The stock fell 14% after reporting earnings Thursday morning, which was somewhat surprising given that the EPS and revenue guidance was raised slightly for Q4 ’23, but forward EPS estimates were revised lower, while forward revenue estimates continue to be revised higher after Thursday’s release. This signifies lower margins, than I had thought for the near future.

Anyway, more to come on Walmart this week.

With the “Magnificent 7” being the market leadership this year, and Nvidia being a big part that leadership, with it being the 4th largest position in the SP 500, sporting a 3.23% weight and being up 237% YTD trailing return as of Friday, 11/17/23, you have to think how tech trades for the last 5 – 6 weeks of ’23 will be somewhat dependent on Nvidia’s results and guidance.

The semiconductors have always been a coincident indicator to tech leadership, something that’s been repeated frequently in Bespoke’s research, so Nvidia will matter come Tuesday night.

International ETF’s had a good week. Client’s largest position is Oakmark International which was up 5.3% on the week, but the Emerging Markets ex-China ETF and the Vanguard Developed Markets (non-US) also outperformed the SP 500.

Corporate high-yield had another good week and continues to trade well despite worries over the slowing economy. Amongst the bond-market asset classes, corporate high yield has been one of the top performers in ’23. If the US economy slows too quickly, that will change.

The 10-year Treasury yield looks fairly valued (to me) at 4.44%.

None of this is advice or a recommendation and past performance is no guarantee of future results. Take everything you read on this blog with substantial skepticism, and make your own decisions. Capital markets can change quickly as the recent 10% rise in the SP 500 attests to, but it can give all that back (and more) even more quickly so gauge your own appetite for volatility and adjust your portfolio accordingly.

Thanks for reading.