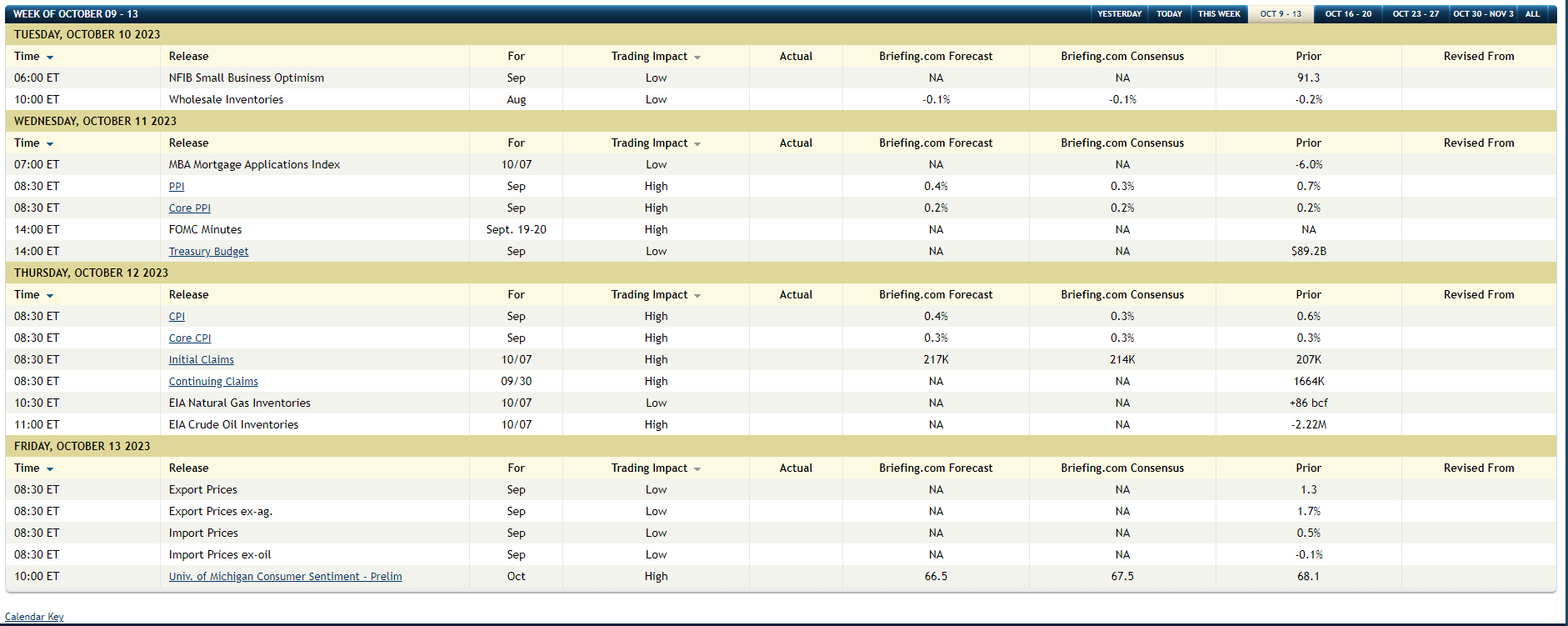

Both the consumer (CPI) and producer prices indices (PPI) will be released this week – PPI on Wednesday morning, October 11th, 2023, and CPI on Thursday morning, October 12th, 2023, according to the above Briefing.com table – so investors get another good look at US inflation data.

Wednesday, October 11th, the overall and Core September ’23 PPI is expected, with overall PPI still expecting to come in a little elevated at +0.4%, while Core PPI is expected at +0.2%.

Thursday morning, October 12th, the overall and Core CPI is expected at +0.4% and +0.3% respectively.

Inflation is expected to gradually recede, particularly “overall” inflation as it’s heavily food and energy influenced.

Last week’s sharp drop in crude oil and gasoline, isn’t likely to show up up until November’ 23 inflation data, so keep that in mind when the September price index data is released this week. If crude oil and gasoline drop further this week, then even a hot PPI or CPI print, might get ignored based on price action currently.

Another twist to the “food” component of the price indices: Walmart’s press release last week that customer tracking data of grocery purchases shows that Ozempic and Wegovy (blockbuster weight loss drugs manufactured by Novo Nordisk) could be having an impact on grocery sales. Now Walmart did say it’s the weight-loss drug impact seems minor for now, but Walmart is expected to generate $640 billion to $650 billion in total revenue in fiscal ’24 (ends January ’24) and anywhere from 50% to 70% of that total is “grocery” depending on the analyst you read.

Walmart (WMT) stock was hit hard on Friday, trading down to $151 and change, before recovering almost $5 in price and ending the day down -1.68% on more than 2x average volume. Same with Coca-Cola, (KO), as KO was hammered on Friday, trading down to a 52-week low of $51.55, before reversing higher and ending up in the green, +1.45% on the day, at $53.14, on more than 2.5x average volume.

The consumer staples sector and food-related stocks have been hit hard the last few months, (check the McDonald’s chart (MCD), with some attributing this to the weight-loss drug phenomenon.

What’s interesting is that Pepsi (PEP) reports this coming week, Tuesday October 10th, 2023 before the opening bell. Like all the staples, PEP has traded down from $195 in mid-May ’23 to the $160 area as of Friday’s close, again presumably on weight-loss drug risk causing American consumers to eat and drink less of their products.

There is a new “disruptor” in America’s grocery aisles. This could get interesting.

Speaking of next week’s earnings:

Here are the companies scheduled to report next week, and the reports that might be worth watching:

Here’s the reports that are of interest to me:

Tuesday morning, October 10th, before the open;

- Pepsi (PEP)

Thursday morning, October 12th, before the open.

- Walgreens (WBA);

- Domino’s (DPZ);

Have to say too, with the weight-loss drug impact, it might be worth seeing what Domino’s (DPZ) says in their conference call on the weight-loss disruption, if any.

Walgreens has a new CEO and a new CIO and they are trying to stop the bleeding and accelerate the healthcare conversion.

Friday morning, October 13th, before the open:

- Blackrock (BLK)

- Citigroup (C);

- JP Morgan (JPM);

- Progressive (PGR);

Summary / conclusion: This blog will be out with a brief summary in the next few days, of the large-cap financial stocks that are ready to report this coming and the week after, with particular interest in JP Morgan, Citigroup, Charles Schwab and other stocks within the financial sector held by clients.

It’s going to be interesting what happens in food and grocery retail, given the weight-loss drug impact. “Grocery” is the holy grail of US retail since it drives foot traffic and is low margin. Everything else in mass-merchant retail like Walmart, Target, Costco, Kroger, feeds off the shopper coming in for grocery.

Maybe it’s nothing.

More to come this weekend. I believe the attached earnings table from Briefing.com sources it’s earnings estimates from SP Capital IQ, where this blog normally sources it’s consensus Wall Street estimates from IBES data by Refinitiv, to which this blog subscribes. There are about three – four different sources of consensus earnings estimates, with Factset, Refinitiv, and SP Capital IQ being the top three.

Past performance is no guarantee of future results. Take everything read here as one opinion.

Thanks for reading.