Accounting for 27% of the SP 500’s market cap, the technology sector is a big deal in terms of both the market cap weights, and the earnings weight in the benchmark. TJ Dhillon, a Refinitiv support rep sent me a quick note, detailing that Apple’s earnings weight in the SP 500 is 6.5% (as of early ’23), versus it’s market cap weight as of 2/24/23 of 6.64%. While the sell-side focuses on “market cap weight” all the time, earnings weight matters.

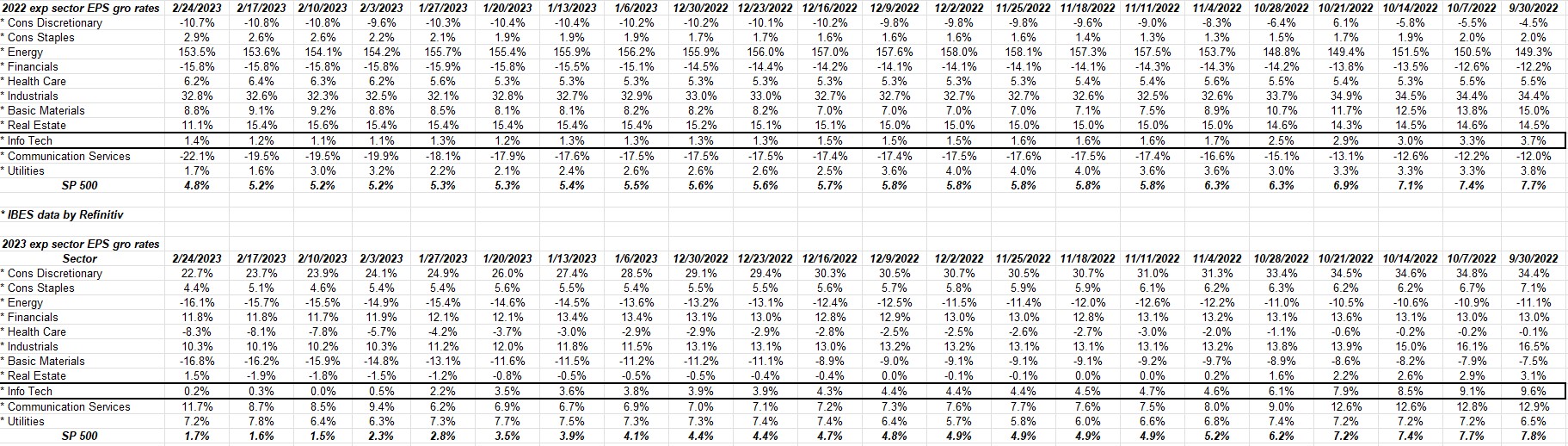

Readers can click on the above “expected” sector earnings within the SP 500 and – looking at the highlighted lines – 2022 and 2023 expected tech sector earnings growth for 2023 is just barely positive.

If 27% of the SP 500’s market cap is expecting flat to negative earnings growth in 2023, that’s not good.

The one small positive to this is that the rate of decline in expected growth in ’23 is still manageable.

SP 500 data:

- The forward 4-quarter estimate slid again this week to $221.71 from last week’s $222.36;

- The PE ratio this week is 17.9x vs last week’s 18.3x

- The SP 500 earnings yield is 5.58%. Bespoke noted that the 1-year Treasury yield is 5.05%, so T-bill yields are approximating the SP 500 earnings yield, (kinda).

Not much to tell readers other than it’s been a slow drip lower for SP 500 earnings starting in the summer of 2022. 2023 expected earnings have seen the biggest negative revisions, which is understandable since we were in the middle of 2022 and thus already knew the earnings health.

No question readers have to take earnings on a company-by-company basis.

The only sector that’s showing positive earnings revisions and higher expected 2023 EPS growth is Communication services, which is META and Google, and while META’s EPS showed sharply higher EPS revisions for 2023, revenue revisions continue to be slightly negative.

This blog updated META estimates this past week and current consensus is expecting +5% revenue growth for an expected -2% EPS growth in 2023, with an 18x forward multiple. Alphabet (GOOGL) is expecting 6% revenue growth and flat EPS growth in 2023 with an 18x multiple.

Alphabet (GOOGL / GOOG) has one more tough quarter of compare with Q1 ’22, then growth starts to slow materially.

Summary / conclusion: The financial sector seemed to get a lot of attention from the mainstream financial media this past week as financials are expecting – per the IBES data by Refinitiv – the 2nd best rate of EPS growth this year, second only to consumer discretionary at +22.7% (although that expected growth rate is coming down), and just ahead of communication services at +11.7%.

Having talked about it the last 8 weeks, Q4 ’23 earnings growth is still showing “robustness” at +10.3%, which Q1 and Q2 ’23 are now showing negative growth y.y and Q3 ’23 has seen lower revisions. It’s still too early to make a call on Q4 ’23 but the trend is the trend – pay attention to it.

Tech sector earnings and revenue growth matter. It’s a big chunk of the SP 500.

Take all this with a healthy grain of salt and considerable pessimism. Past performance is no guarantee of future results. All data is sourced from IBES data by Refinitiv. Capital markets change quickly, both positively and negatively. If there is one thing this business is loaded with and that’s – well – opinions, and they can change quickly.

Thanks for reading.