The 5-year Treasury yield jumped 27 bp’s last week, from 3.66% the prior week to close, to 3.93% at this Friday’s close. The interesting thing: the first week of January ’23, the 5-year Treasury yield fell 30 bp’s on the week. As someone who isn’t a yield curve specialist, thought it was worth noting, if you want an idea where the monetary policy and inflation debate is being played out.

The 5-year Treasury closed 2022 at 3.99%.

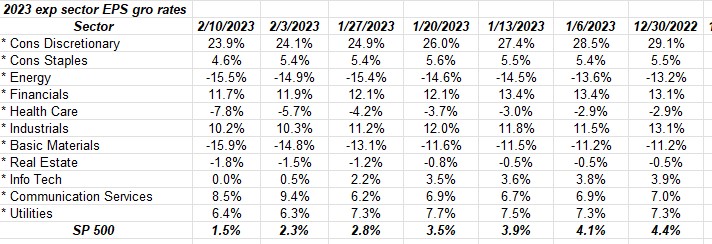

With 4th quarter earnings every year, most company management’s usually give their first look at the coming twelve months guidance, and this year was no exception. Here’s the IBES data by Refintiv table that shows how the 11 SP 500 sector growth rate estimates have changed for 2023 since 12/31/22.

As the reader can see the “estimated” SP 500 earnings growth for 2023 (as a whole) has now slowed to 1.5% as of Friday, February 10, 2023.

4th quarter, 2022, earnings will unofficially close when Walmart reports Feb 21, 2023.

Here’s a quick look at how each sector’s estimated growth rate has changed since 12/31/22:

- Consumer Discretionary: -18% drop from 12/31/22, from expected growth of 29.1% to today’s expected growth rate of 23.9%;

- Consumer Staples: 16% drop from a much slower growth rate from 5.5% to 4.6% as of today;

- Energy: 15% drop from -13.2% to -15.5% for the Energy sector;

- Financials: -11% drop from +13.1% to +11.7;

- Health Care: Has slid sharply from a -2.9% expected growth rate to -7.8%.

- Industrials: a 22% drop in estimates growth from +13.1% to +10.2%;

- Basic Materials: down 42% since 12/31 from -11.2% to -15.9% at present;

- Real estate: down minimally to -1.8% from -0.05%;

- Technology: fallen to 0% from +3.9%

- Communication Services: has risen from +7% to +8.5% as of 2/10/23;

- Ute’s: has slid from 7.4% to 6.3% ;

There is a couple of caveats here, i.e. the reader should ask is growth positive or negative since a sector with a slowing growth rate that is already negative, might be able to absorb negative revisions since a decline in sector growth is already factored in for the full year, such as Energy;

Only Communication Services, whose two largest cap names are Alphabet and META Platforms saw positive revisions to the expected 2023 growth rate between 12/31/2022 and 2/10/23.

Basic materials looks to be seeing more harsh revisions than Energy.

Financial sector looks positive: good growth expected – low double-digits – but would like to see negative revisions slow.

Here’s a quick ranking of highest to lowest growth rates for expected 2023 sector EPS growth:

- Consumer Discretionary: +23.9%

- Financials: +11.7%

- Industrials: +10.2%

- Communication Services: +8.9%

- Utilities: +6.4%

- Consumer Staples: +4.6%

- Technology: 0%

- Real Estate: -1.8%

- Health Care: -7.8%

- Energy: -15.5%

- Basic Materials: -15.9%

Two of the worst sectors in ’22 were Discretionary and Communication services and their ’23 growth rates are positive, while Energy, the best performing sector in ’22 by a wide margin, is now near the bottom.

Looking at the percentage change of the sector’s expected growth versus the overall expected growth rate gives a reader the magnitude of the impact of guidance on 2023’s expected growth.

Summary / conclusion:

While some might think this is “navel-gazing” it pays to pay attention to expected growth rates and how they are changing over times for the sectors. Technology is still the big dog in the yard with a market-cap weight of 27.4% of the SP 500, with Financials being teh next biggest weight at 11.6%, both as of Friday, 2/10/23.

Technology’s flat EPS growth for 2023 might mean investor look at the other market-cap asset classes like mid and small-cap or the RSP (equal-weight) SP 500, but that’s not a recommendation. Do your own homework – I’m just giving readers a feel for where the numbers are leading us, and they can often change, as we saw in 2022, where SP 500 EPS gradually weakened through the year.

There is more to write about but this week will be kept short because of the data.

Take this all in context of the market action. All raw data is sourced from IBES data by Refinitiv, but the calculations are my own. Past performance is no guarantee of future results.

Thanks for reading.