The SP 500 earnings data won’t be much different than last week, and next week, Walgreens is the only company of note reporting.

In a note to clients tonight after the final bell of 2022, the last line of the email stated that 2022 was badly needed to reset the shot clock on the secular bull market.

In this post of December, 2021, it was noted that “annualized” or annual returns for the SP 500 were getting too robust. In this post written 6 weeks later in mid-January ’22, the article went into more depth on “annual” returns and how they were quite elevated, particularly 2019, 2020, and 2021, and what that could mean for 2022.

This post a few weeks ago talked about this secular bull market being only 10 years old.

The “annual” return data will be updated this weekend. It should be interesting.

SP 500 data:

- The forward 4-quarter estimate fell to $222.91 this week from $223.31 last week.

- The quarterly “bump” will happen next Friday, January 6th, 2023, and that estimate as of today is $229.52, so readers can see the mathematical impact of the dropping off of one quarter and the adding in of a forward quarter. The $229.52 is actually the current calendar year estimate for 2023.

- The PE on the forward estimate today is 17.22x, up a little from 9/30/22’s 15.6x;

- The SP 500 earnings yield this week is 5.81%, the same as last week, and down from 6.43% on 9/30/22;

- The final Q3 ’22 bottom-up estimate for the SP 500 was $56.02, which is a plus, it’s ended up above $55;

Ed Yardeni still has a $215 EPS estimate for 2022 on the SP 500. To hit that number with Q4 ’22 earnings, which start getting reported in two weeks, the bottom-up estimate for Q4 ’22, currently at $53.87,will have to fall under $50. That could easily happen given sentiment, but it would be unusual.

It would seem to me that pre-announcements would start next week almost immediately if Q4 ’22 earnings were going to be that bad.

Again, Yardeni is pretty good in terms of his SP 500 EPS estimate forecasts.

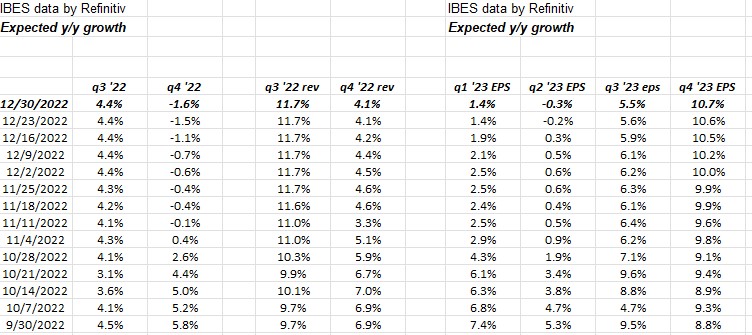

2023 Quarterly SP 500 EPS and revenue growth rates:

Readers need to see this table. This blog has been publishing this table for the last several weeks, but today the numbers start at 9/30/22.

Starting at 9/30/22, look at the change in expected, quarterly EPS growth rates for the SP 500 for 2023.

- Q1 ’23 has slid to +1.4%, losing almost all of it’s +7.4% expected growth since 9/30/22 so assume the quarter will be bad;

- Q2 ’23 started at +5.3% on 9/30/22 and is now negative;

- Q3 ’23 is now expecting +5.5%, almost half the expected +9.5% on 9/30/22;

- Q4 ’23 is now up 190 basis points to +10.7% vs 8.8% on 9/30/22;

That’s a pattern that’s holding up the last 90 days.

It’s telling readers – at least so far – that SP 500 EPS could bottom sometime in the middle of 2023.

It will be important to see how this changes with Q4 ’22 earnings and guidance.

And there is NO reason for SP 500 corporate guidance to be anything but subdued, and probably straight out depressing when Q4 ’22 earnings start.

The only trend that has begin to crack that was evident all year in terms of asset returns or market trends is the weakening in the dollar the last 90 days.

Watch the numbers.

Summary / conclusion: Starting with Q1 ’22 numbers in April ’22, the Wall Street mindset was that earnings were going to be “disastrous” and it never really happened, all year. That doesn’t mean the first half of ’23 can’t be ugly, but we’ve had a considerable discounting of bad news in the stock market already, particularly large-cap and mega-cap growth.

The earnings data above – being updated weekly – provides good clues to the SP 500 and the individual sectors.

There will be plenty more published this weekend, which will bore you to tears, so if you need help getting to sleep, this blog’s your answer.

Subscriptions are free (i.e. the email list that is) so throw in your email, and argue with me all you like. The only thing I ask is that you be reasonable, measured and somewhat thoughtful about your response.

Take all of this with a grain of salt and note that past performance is no guarantee of future results. This blog’s prognostications were roughly on target for 2022 as I told every client at every winter meeting, “2022 was going to be a tougher year” BUT even if you can predict direction, it’s far more difficult to predict magnitude. The one unfortunate element to this business is the necessity for everyone to be making predictions to get attention from the mainstream media and it’s the one aspect that’s sure to fail consistently.

No one – and I mean NO one – has any ability to predict the future accordingly.

The dollar weakening is the first “trend break” of 2022. That’s a start.

Thanks for reading.