Great chart from Mike Zaccardi on Twitter on the “developing” chart in GLD. Mike can be found on Twitter at @MikeZaccardi. He’s a prolific publisher and technician on Twitter and does great work.

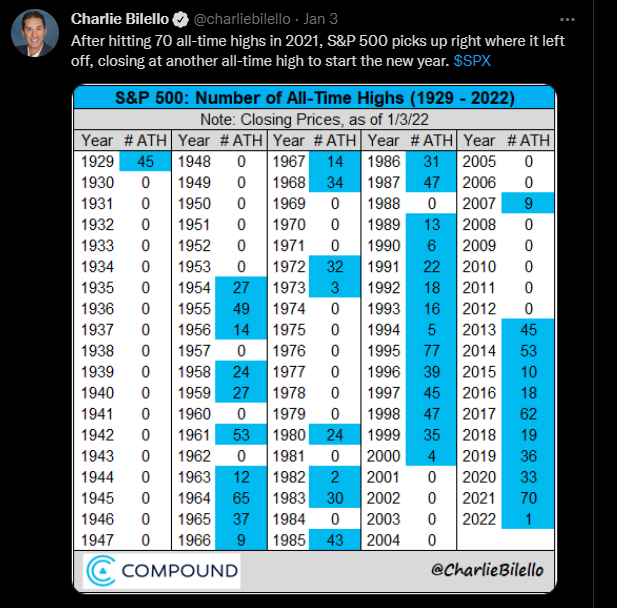

This table from Charlie Bilello, another great technician and Twitter publisher (@CharlieBilello) is – in my opinion – a far more telling chart that explains gold’s true correlation over the last 50 – 60 years than the “inflation” story ever would or could.

What were gold’s strongest periods of return on an absolute basis ? While we don’t (to my knowledge) have a constant measuring stick, most folks who are old enough would say “the late 70’s” or even, “the 70’s” and then again the period from 2000 to 2011.

Gold peaked at $800 sometime in 1979 or 1980 and didn’t bottom until the late 1990’s and from what I can remember, it was around $200 – $250 an ounce when it did bottom in the late 1990’s, and then peaked again at roughly $1,858.50 an ounce in September, 2011.

Think about it: using Charlie Bilello’s table, gold’s strongest period during the 1970’s was the period where the SP 500 made no all-time-highs, and then again again from 2000 to 2012 where again the SP 500 only made very few highs in 2000 and 2007.

Gold – in my opinion – is the best asset to hedge a period of years where the SP 500’s return is flat to negative, if history is any guide.

Gold’s worst periods of returns – whether relative or absolute – were the period from 1980 to 1999, when an ounce of gold traded down from $800 to roughly $250 per ounce, and then again from 2012 to today. Both those periods were extraordinary returns for the SP 500 on an absolute basis. From January 1, 2012 through 12/31/21, the SP 500’s average, annual return was 16.5%, versus GLD’s 1.18%. (Ychart’s performance calculator was the source of this return data.)

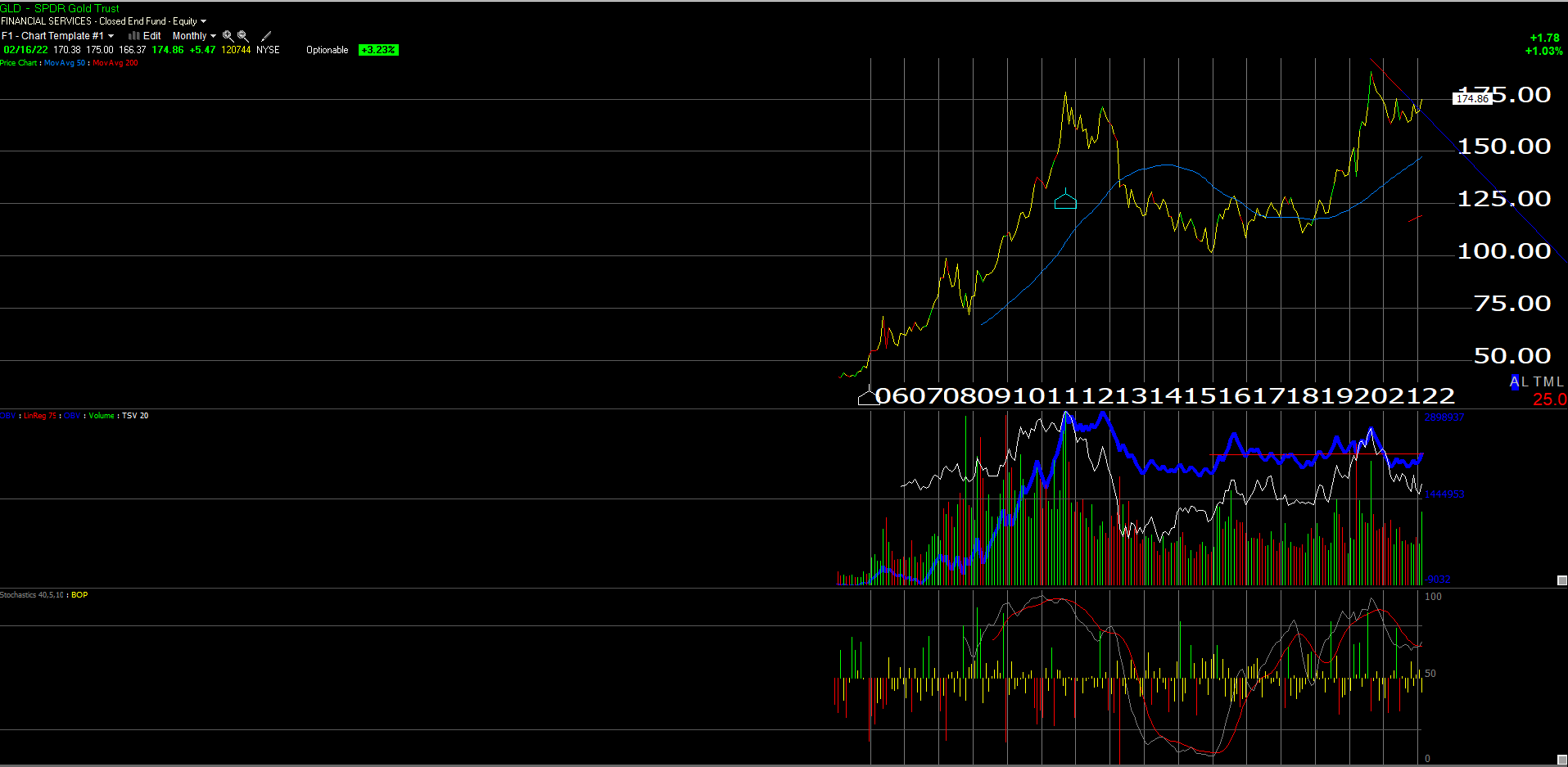

The SPDR GLD ETF monthly chart:

Summary / conclusion: It’s tough to compare returns for Gold / GLD over the last 50 years since gold was traded as straight bullion for the 1980’s and 1990’s and it was quoted in terms of market price per ounce. It was only in 2005 that SPDR’s GLD ETF was created and by the end of that decade become the largest ETF by market value (which was telling us plenty in hindsight). But I paid attention to it in the 1980’s and 1990’s since as a kid during the ’70’s it got a lot of financial press for – as we know now – all the wrong reasons. It’s amazing to me today, 40 years later, that gold is still regarded as an “inflation tell” when it’s best decade from 2000 to 2011, when it traded from $250 an ounce to $1,850 (the GLD peak in September, 2011) was one of the worst “deflationary decades” for stocks and real estate and the general inflation gauges that we’ve seen since the 1930’s. The SP 500 was essentially flat for the decade from 2000 to 2009, and then American’s saw the great “housing depression” the first of it’s kind nationally, again since the 1930’s. It’s truly hard to call 2000 to 2009 anything but deflationary, and the US economy was followed by the great Liquidity Trap from 2008 to 2012, where zero interest rates were met with lethargic demand.

Over the years, the financial media has linked or correlated GLD over shorter periods of time to a weak US dollar, international tensions (like Ukraine today) and other factors, but if you look over the long term, GLD has been an effective hedge against flat to negative SP 500 returns for longer periods if time.

I like listening to Josh Brown and the RWM crew, although they publish so much it’s hard to follow and digest in a way that would give justice to their work, but Josh recently noted (perhaps tongue-in-cheek) that Bitcoin was thought to be an inflation hedge, although my first thought was we don’t have enough time with it yet. The key aspect to GLD is that we have 50 years to look at the metal over various bull and bear markets.

My question today is does Bitcoin’s existence complicate GLD’s future ? Both are mediums of exchange and far less stores of value, although the greater the medium of exchange, eventually the greater the store of value.

This blog cautions readers every week to take the content found here and really anywhere on wall Street with great skepticism and healthy grain of salt. I personally believe the financial media has miscast gold and the GLD for decades as an inflation hedge when – if you actually look at the returns by decade – it’s anything but.

If readers and investors believe that the SP 500 will suffer from flat-to-down returns for the next 3 – 5 years, history has shown us that gold and today’s GLD, is an effective hedge against those flat returns.

Will the future repeat ? We can never be sure, and it’s hard to say what role Bitcoin and crypto will play as equity market hedges.

The GLD high in September ’11 was $185 and change. The GLD traded above that level only once and that was in 2020 and then the GLD fell right back below the old high. GLD’s 10-year return as of 2/15/22 was 29 bp’s or 0.29% (yes, you read that right.)

Some clients are long small amounts of the GLD, but while the SP 500’s average, annual return is a compelling reason to expect flat markets going forward, I’m not yet convinced the secular bull market in US stocks is completely over.

Thanks for reading. The comments on this are sure to be entertaining.