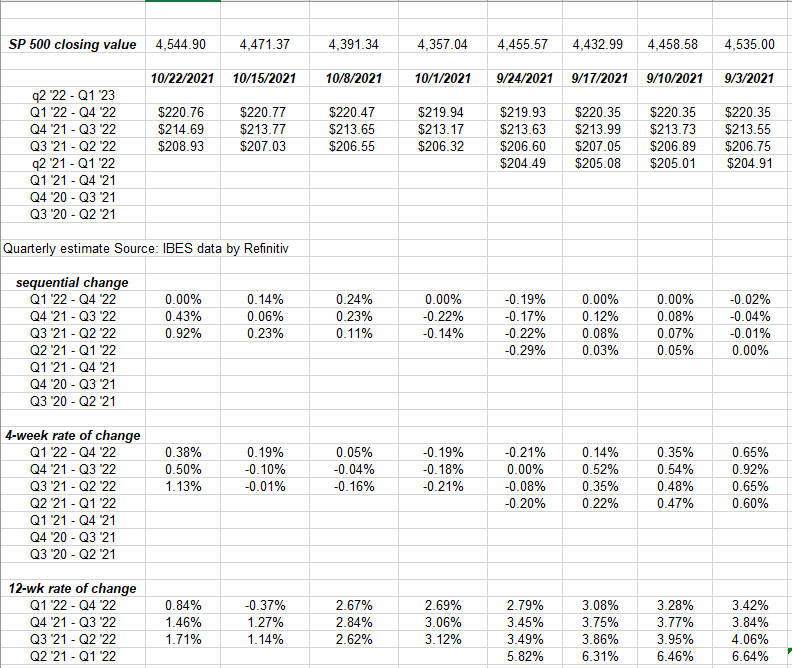

This table was cut and pasted from IBES’s weekly This Week in Earnings report as of Friday, 10/22/21.

Readers should remember that investors are still getting just 3rd quarter, ’21 SP 500 earnings and with 177 companies reporting as of Thursday night, October 21, ’21, 383 companies are still left to report and then 4th quarter earnings do not finish up until mid-February ’22.

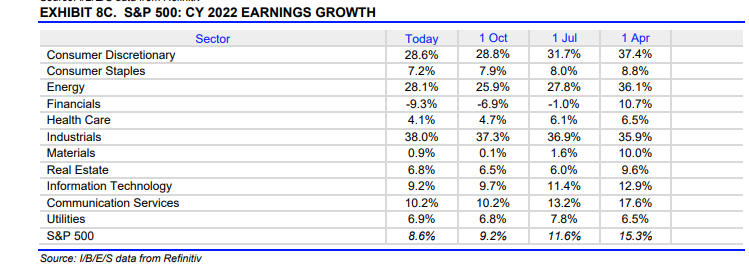

What struck me in the above 2022 expected sector growth rates was the fact that Financials are seeing lower expected growth rates since July 1 ’21. JP Morgan (JPM) and Bank of America (BAC) are showing EPS for 2022 lower than 2021 – probably true for any major bank with a large consumer operation – since credit provisions were so large this year and will dwindle in 2022.

This data was posted Friday, 10/22/21 to this blog showing “expected” growth rates by quarter for 2022.

It’s clear analysts are very reluctant to get too bullish about 2022. Next year was going to be a year of a “return to normal” growth rates for SP 500 EPS and revenue, but now with expected tapering by the end of 2021 (I guess the only question is whether the Fed starts in November ’21 or December ’21), analysts are even more cautious.

“Rate-of-change” analysis:

Before we all get too bearish, looking at the rate of change for all forward quarters up to and including 2022, readers can see the 12-week rate of change has started to turn positive once again. Sequential increases have been the hallmark of the SP 500 EPS data since May, 2020, with some softening towards the end of each quarter when the reporting dries up.

Big week for the “Big 5”: (all info per Breifing.com)

- Facebook (FB) reports Monday, 10/25 after market close (AMC);

- Alphabet (GOOG / GOOGL) reports Tuesday 10/26 AMC;

- Microsoft (MSFT) reports Wednesday, 10/27, AMC;

- Amazon (AMZN) reports Thursday, 10/28, AMC;

- Apple (AAPL) reports Thursday, 10/28, AMC;

This blog will post a deeper preview of each company showing EPS and revenue revisions for the last year. The preview will likely come Sunday of this weekend.

SP 500 EPS data – by the numbers:

- The forward 4-quarter estimate rose this week to $214.60 from last week’s $213.77;

- The PE ratio on the forward estimate is 21x vs 21x last week;

- The SP 500 earnings yield fell to 4.72% this week from 4.78% last week;

- The Q3 ’21 EPS estimate is now above $50;

There is a key point about the pattern of weekly SP 500 EPS estimates that needs to be made: using the recent October ’21 data when September ended and the month of October began, the forward estimate jumped from $206 to $213. As mentioned above, the hallmark of the stock market recovery beginning in late March ’23rd was that SP 500 EPS estimates increased sequentially every week, which really isn’t normal.

Again, using the $206 to $213 example, in normal economies and times, the $213 estimate would gradually erode over the ensuing 3 months – meaning from early October to late December – and as long as it didn’t drop below the final estimate of the last quarter, the upward trend in SP 500 EPS estimates would be intact.

The whole point of this pattern analysis is that what we have seen post-pandemic is abnormal and at some point the familiar pattern will return but it could bring out a lot of bearishness since the weekly SP 500 EPS pattern will look a lot more ambiguous.

(That’s way more than you want to know about SP 500 earnings analysis.)

Summary / conclusion: The sell-side is starting to get a little more cautious about 2022, probably thanks to the looming start of tapering and other issues, but my suggestion is – while you should pay attention to the data – watch the data, and maybe more importantly the market’s price action, a little longer.

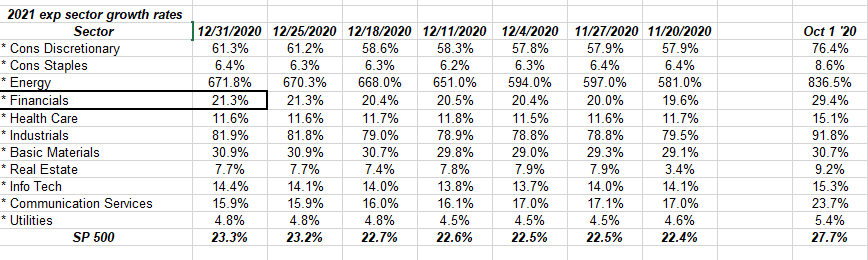

Last year at this time the 2021 data was looking like this: (expected sector growth rates that is):

As of today, the actual expected 2021 growth rates are this:

This blog will have an analysis of the Big reporting this week, with EPS and revenue revisions and some other data.

Remember, the Big 5 reported their Q2’s the last week of July ’21 and it had a pretty sizable impact on the SP 500 data as was detailed in this blog post last week.

The one thing i didnt like about Friday night’s action is that – after closing at a new all-time-high Thursday night, 10/21, the SP 500 slipped back below 4,545 to close the week.

Thanks for reading, More to come this weekend.