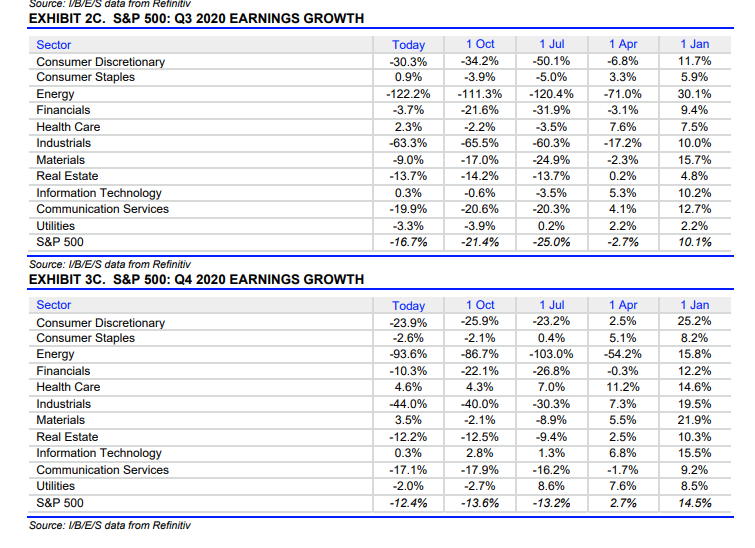

Looking at the quarter-by quarter data from IBES by Refinitiv, the sharp upward improvement to the Financial sector’s expected growth through mid-2021 caught my eye this weekend. Here’s some of the IBES data:

Q3 ’20 & Q4 ’20:

Note the improvement in 3rd quarter ’20 expected EPS growth for the Financial sector, from -21.6% on October 1 ’20, to last week’s -3.7%. That’s a huge improvement in 3 weeks and was likely primarily a function of the better-than-expected consumer losses seen in Q3 ’20 earnings.

Note too, how Q4 ’20’s expected EPS growth has improved as well.

Financials and Materials are two of the sector which the sharpest improvements since October 1 ’20.

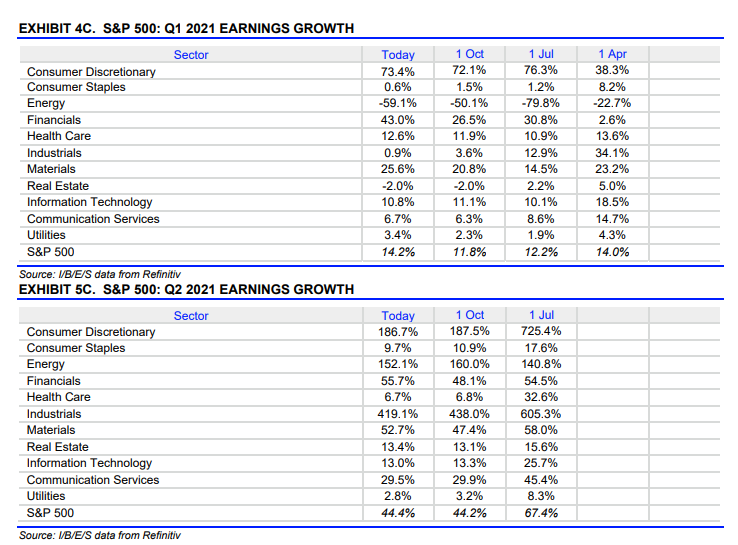

Looking into the first and second quarter’s of 2021, not again the improvement in “expected” Financial sector growth rates, turning from far less negative in late 2020 to positive growth in 2021. Part of that will be easier comp’s in q2 ’21 and q3 ’21 so we will have to average the two actual growth rates to find the combined growth rate for 2020 and 2021.

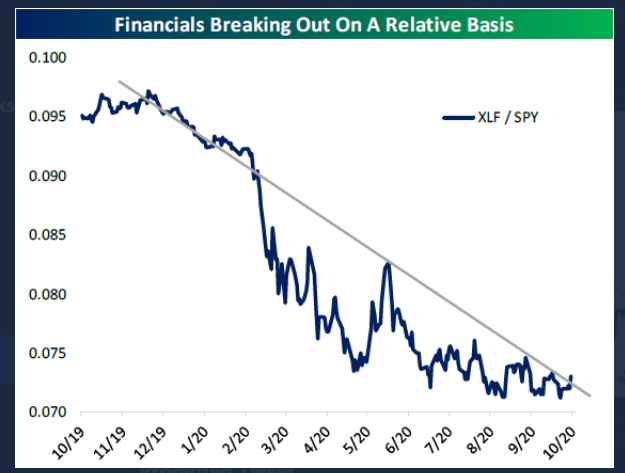

How are Financial’s performing in 2020 ?

This graph from Bespoke shows the XLF divided by the SPY, and readers can see the Financial sector is JUST breaking its downtrend that began in January ’20.

The XLF is down 16% YTD versus the SP 500’s +9.01% YTD as of 10/23/20. The IYF is down 12.92% YTD.

Summary / conclusion: The Financial sector is down to 9.9% of the SP 500’s market cap as of 10/23/20. As recently as 5 years ago, when the real estate sector was spun out of the Financial sector, the remaining weight of the Financial sector was 16% – 17% of the SP 500. Post-2008 interest rates, and heavy regulation, have certainly taken their tool on the sector.

Judging by the loan-loss provisions for Q3 ’20, the banking sector is likely over-reserved for consumer credit losses, with another stimulus program likely to come after the Presidential election.

Unfortunately, banks are prohibited from repurchasing stock today. The Fed came out in late September and announced the share repurchase ban will continue another 90 days.

Clients remain overweight Financials as an offset to the Technology overweight in client accounts. All it will take to lift the sector substantially is the Fed announcing that the banks can begin to repurchase their stock again.

This data changes week-to-week but the overall trends have ben stable for a while. I’d like to see Financial sector expected growth rates continue to improve.

Thanks for reading.