It was tempting to ask in the headline whether readers were looking for the “over” or “under” on Q2 ’20 SP 500 earnings this quarter ?

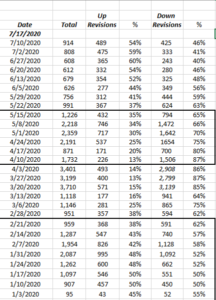

My own bias coming into Q2 ’20 given the very low expectations, is that the numbers are “better-than-expected”. We’ll talk about the banks and financials in a second, but this table we compile every week of “SP 500 estimate revisions” higher vs lower, indicates that since the bottom in March ’20, the number of revisions each week has been trending ever-more positive.

Here’s the table:

The data is sourced from IBES data by Refinitiv, but the s/sheet kept internally goes all the way to 2009.

The IBES report only shows revisions over the last 4 weeks.

The bordered areas show the Q4 ’19 earnings season from early January ’20 to mid-February ’20, and then Q1 ’20 earnings, but readers should follow the middle column the percentage of revisions that were upward or higher over the time periods.

I didn’t realize it at the time, but Q4 ’19 SP 500 earnings may have been an early tell for Covid-19 weakness. Note how positive revisions during Q4 ’19 earnings season during January and early February ’20 didn’t get above 50%.

Big Banks start reporting this week:

The banks / financials that are owned for clients and reporting this week are JP Morgan (JPM), Bank of America (BAC), Charles Schwab (SCHW), and Goldman Sachs (GS). Our other financial is CME Group and won’t report for another week or two.

In the recent post on “Prepping for a March, 2000, Moment” clients top 10 positions were disclosed and have been pretty constant for years. Within client accounts the Technology overweight versus the Financial sector overweight is a way of barbelling client portfolios to not become top heavy with large-cap Tech or growth or traditional “momentum” names.

Callum Thomas, the decent Kiwi technician from “Down Under” charted Tech vs Financials this weekend, which is a microcosm of “growth vs value”.

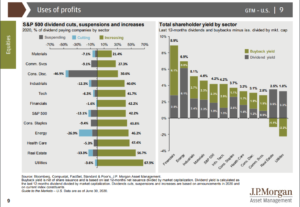

Here is an interesting chart from JP Morgan’s “Guide to the Market” on the 11 sectors of the SP 500 and how “shareholder yield” (buyback yield + dividend yield) is distributed by sector.

The second bar chart to the right is the eye-opener, since I would have thought that Technology would have been closer to Financials. Apple is buying back 5% to 6% of their market cap every year, and the sector seems small by comparison to the Financial sector.

With the CCAR (Comprehensive Capital Analysis and Review) reports of late June, the Fed is prohibiting share repurchases and capping dividends to 2nd quarter payouts.

“During the third quarter, no share repurchases will be permitted. In recent years, share repurchases have represented approximately 70 percent of shareholder payouts from large banks. The Board is also capping dividend payments to the amount paid in the second quarter and is further limiting them to an amount based on recent earnings. As a result, a bank cannot increase its dividend and can pay dividends if it has earned sufficient income.” (Direct quote from the June 25th, 2020 CCAR test results press release.)

The question is, “Is this already in the stocks ?”

Summary / conclusion: Looking at JP Morgan’s estimate revisions, the bank seems to have gotten some recent bumps to EPS estimates in the last week. Capital Market activity should be robust with $1 trillion in corporate debt issuance thus credit losses and net interest margin remain the only issues. With the fiscal stimulus actually providing for more household income than what the lower-end was earnings pre-Covid-19, there is a chance credit losses might not be as harsh as expected. Goldman could be a big winner with FICC (fixed income, currencies, commodities), and I think JP Morgan and Bank of America will at least hold serve until share repurchases can continue.

Another plus is that sentiment turned on banks in the last 2 – 3 weeks of the 2nd quarter. A number of CNBC “guru’s” were shorting the banks coming into earnings. That could work since we have another 10 weeks before the next round of CCAR results are released, but of bank EPS and revenue revisions stay stable or even move positive, that short covering could help the stocks.

John Butter of Factset noted this earnings season will be as bad as 2008. I noted that it could be as bad as the Great Depression which was a bit hyperbolic, and I was talking about y/y growth rates in revenue and EPS.

Either way it’s likely to be bad, but the question again is “is this baked into the stocks ?”

Thanks for reading. Take everything with a gran of salt.