Oracle (ORCL) reports their fiscal Q3 ’20 quarter tonight, March 12th, 2020, after the closing bell, and given the February, 2020 quarter end, and the global scope of Oracle’s business, that reaches into so many sectors and subs-sectors needless to say I would have to think many people will be listening to the conference call.

However, i would have to think that Oracle’s guidance on fiscal 2020 and the rest of the calendar year will be of the greatest interest to the Street.

Oracle’s fiscal 2020 ends May 31 ’20 and their fiscal Q4 – which is typically Oracle’s strongest quarter of the year – has already begun. As they say in life, timing is everything and if Oracle was depending on a strong fiscal 4th quarter to help the year, comments tonight will give investors an idea of whether the typical Q4 will materialize (and we should assume it won’t).

Street consensus (per IBES by Refinitiv) for tonight is expecting $0.96 in earnings per share (EPS) on $9.75 billion in revenue, for expected year-over-year growth 10% in EPS on 2% revenue growth.

The consensus for Q4 ’20 is currently $1.23 in EPS on $11.3 bl in revenue for expected year-over-year growth of 6% EPS on 1% revenue growth.

Full-year 2021 expectations are for 9% EPS growth on 2% revenue growth.

(All these estimates will likely change after tonight.)

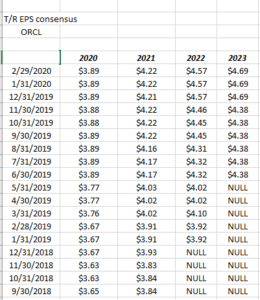

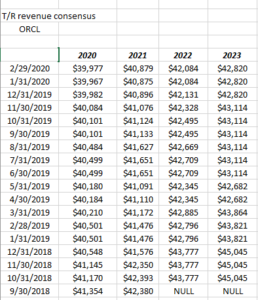

Here are the trends in EPS and revenue estimates for Oracle (per IBES by Refinitiv):

The revision trend estimate is lower while EPS estimates since the 4th quarter of 2018 have actually trended higher, thanks mainly to Oracle’s free-cash-flow generation, and the cash spend on buybacks.

In the last 5 quarters, here is Oracle’s “average” year-over-year share reduction (see the excel line highlighted by the black border) has been a 13% decline in fully diluted shares outstanding:

The only issue with this is that Oracle’s cash and securities balance has declined since the Tax Reform Act passed in December ’17 has allowed Oracle to repatriate the cash and use it for the share buyback.

Since the November 17 quarter, Oracle’s cash and securities has declined from $71 billion to $27 billion.

Hardly alarming but I don’t think Oracle can continue to repurchase shares at the rate they have been over the next few years, since their $50 billion in debt outstanding has left Oracle with a 50% debt-to-capital ratio, and the rating agencies might frown on that level of debt.

Summary / Conclusion: What has been left unsaid about Oracle in this quick preview is that Oracle is struggling to reinvent itself in the cloud environment as the cloud has represented both a competitive threat and an opportunity for the database giant. Organic license growth for Oracle has been negative the last three years (-7% growth) as ERP is 10% of Oracle’s revenue, and the cloud is thought to be 20% of Oracle’s revenue.

It isn’t that Oracle’s cloud business isnt viable, it’s just that the cloud business isn’t growing fast enough to offset the decline in on-premise, legacy database business.

Ultimately, Oracle, like IBM, like Cisco, like so many of the former 1990’s growth babies, needs to show that “new Oracle” is growing faster than the decline in the legacy business of “old Oracle”. In other words, faster revenue growth is the key, but you won’t see any of that (or at least that is highly unlikely) in tonight’s earnings report.

And this will ultimately all be clouded by the C-virus and Covid 19, and what the next few quarter’s of Oracle will look like.

I dont know how Oracle can reasonably guide for the rest of calendar 2020 given some of the hysteria around Covid-19.

As this is being written Oracle is trading below the $45 peak Oracle struck in March of 2000. That’s not a positive but it’s more a function of Covid-19 than what might be a long-term business model disruption issue from a lack of traction in cloud.

Tonight, look at Oracle’s cash position, and just listen for any Oracle management commentary on what they are seeing / experiencing around the globe.

Clients own no Oracle, which was more a function of the struggle to adopt a “new Oracle” strategy rather than anything Covid-19 related.

Thanks for reading.

(Remember all of this is an opinion. I don’t see how any SP 500 company can give any kind of reasonable guidance and we will look at where the Street eventually lands in terms of Oracle EPS and revenue consensus for fiscal and calendar 2020. There is such a range of outcomes around these current events, i don’t envy sell-side analysts trying to put numbers around the next 12 months.)