While the big news after IBM’s earnings release was that Ginni Rometty would be stepping down as CEO, and would be replaced by Arvind Krishna, (supposedly the IBM executive that pushed for the RedHat acquisition), and James Whitehurst, the RedHat CEO who will become president of IBM, maybe the more important aspect to the earnings release was that the mainframe (System Z ?) business was strong in Q4 ’19 and helped drive results.

Morningstar noted in their summary of IBM’s 4th quarter that typically the mainframe cycle lasts 5 quarters.

My first thought was that “well, that gives IBM a year to get RedHat fully integrated into IBM”.

Morningstar still does not think this is a turnaround for IBM, and that the pop in the stock represents just a rally to catch the mainframe cycle (My words, not Morningstar’s.)

Street consensus is expecting just 1 – 2% revenue growth over the next three years, (2020 to 2023) which is expected to generate 4% – 5% EPS growth, which is still better than the decade of 2010 to 2019, where only three of those years saw positive revenue growth.

Expectations for IBM are still remarkably subdued today.

In an article written for Seeking Alpha prior to earnings, two graphs were posted showing that IBM has underperformed the SP 500 by about 1500 bp’s per year since IBM’s stock price peak near $215 in 2013, and 1300 bp’s per year for the entire decade from 2010 to 2019. (The article is here, but it was posted only for subscribers. )

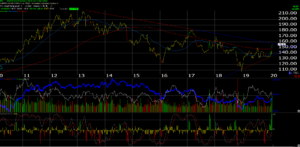

Here is a weekly chart of IBM:

Readers can see the green spike in the last few weeks in the stock price, some of it possibly due to short-covering and some due to (perhaps) optimism over a new CEO and President focused on RedHat and the hybrid cloud and cloud opportunity.

An interesting interview on CNBC last week between Becky Quick and CNBC contributor Jeff Sonnenfeld demonstrated the emotion of the Ginni Rometty’s resignation. Becky – reading the script – called Rometty’s tenure “turbulent” while Sonnenfeld was far more upbeat and glowing.

Maybe a better word for Rometty’s time as CEO was “lethargic: Watson never went anywhere and was heavily-promoted in ads, until analysts started asking questions about Watson’s numbers and then it went away, because Watson (at least 3 years ago) was more hype than reality. The “strategic imperatives” initiatives around the cloud from 2 – 3 years ago fizzled as well. IBM reported the growth every quarter and it really failed to get traction. IBM was a distant player in the cloud business and still is, although the hybrid cloud and RedHat could drive some growth for IBM, if they get it right. (Morningstar describes the hybrid cloud market as a $1.4 trillion opportunity, still in its earlier stages.)

Summary / Conclusion: Readers worried about the length of this bull market today can hedge some of that risk by looking at long-term laggards that have badly under-performed the SP 500, and IBM certainly qualifies in that regard. The above chart shows IBM is seeing some renewed interest from investors BUT the stock needs to trade over $160 on decent volume and remain there to break the 7-year downtrend.

I’ll be looking at the back-half of 2020’s EPS and revenue estimate revisions, and also 2021 to see if analysts have any confidence in Arvind Krishna and James Whitehurst and the IBM hybrid cloud team. Morningstar is skeptical on the hybrid cloud opportunity: the old Mstar analyst saw more opportunity, but the new analyst is definitely more skeptical about IBM being able to turnaround based on RedHat and the hybrid cloud.

Color me a skeptical believer. The right management always matters.

The stock still has an 8% free-cash-flow yield and a 4.5% dividend yield for those who can be patient.

Client’s position is still less than 1% of total invested assets.

Thanks for reading.