Usually earnings previews are written over on Seeking Alpha but Oracle’s (ORCL) story is well known and the fact is I could have written the same earnings preview the last 4 quarters and just copied it forward each time, updating the earnings and revenue estimates.

The stock is fairly valued in the mid-$50’s with bias to the upside based on the substantial share buyback, but the meat of Oracle’s story is that the transition to the cloud, and the Saas/Paas/Iass transition is turning out to be a lot more difficult than Oracle thought.

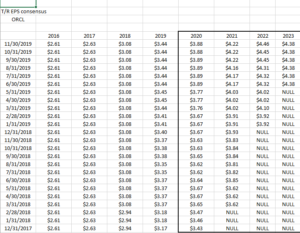

What readers should take away from the above spreadsheet is that Oracle’s fiscal 2020, 2021, and 2022 EPS continue to be revised higher, albeit at slower rate.

Oracle’s “average” expected forward EPS growth rate for the last two quarters is 6%. Pretty ordinary for the software and database giant.

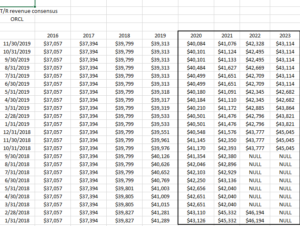

Readers should look down the spreadsheet to late 2017 and 2018 for fiscal’s 2020 and beyond and note how expected revenue growth slowed markedly and then Oracle put the nail in the coffin of those who thought the Cloud transition would reinvigorate growth when Oracle’s management stopped disclosing or breaking out the cloud-related growth,

Expected forward revenue growth for Oracle over the past year has averaged 2% – 3%.

Valuation:

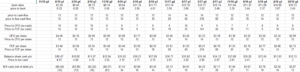

Trading at 10x cash-flow and 12x free-cash is reasonable for a software firm that’s growing mid-single-digits.

Share repurchases and dividends:

As of the August, ’19 quarter, Oracle had repurchased $31 bl of their own shares, down slightly from the $36 billion as of the May ’19 quarter. Normally that kind of repurchase activity, would be a catalyst for the common stock, but Oracle is also a considerable “diluter” using their shares for large acquisitions and then allowing the departing exec’s to sell those shares after the lockup. These shares sales (by my own calculations) absorb about 20% – 25% of the repurchase plan each quarter. The thing is though, anyone who has followed Oracle for any period of time knows they are a serial diluter.

Oracle’s dividend has been kept the same in terms of the dollar amount for ling stretches as the software giant works through the cloud transition and the ongoing erosion in the legacy business, but Oracle did boost the dividend to $0.96 this year, with the only question remaining what they do after the February ’20 quarter.

Capital return and some margin expansion are the two positives for the stock.

Summary / conclusion: With the death of Mark Hurd, it might end the “dual CEO” role that Oracle was using with Safra Catz and Mark Hurd sharing the CEO responsibilities. However the biggest issue longer-term for Oracle is the transition to a cloud-based platform for Oracle’s core database product.

After the close on Thursday, December 12th, 2019, Oracle is expected to report $0.88 in earnings per share (EPS) on $9.645 billion in revenue for expected y/y growth of 10% and 1% respectively. And that 1% revenue growth is an issue. Cloud adoption and revenue growth for the software giant go hand-in-hand as the core database business and services revenue streams, just aren’t growing anymore. Like an IBM, or Cosco, or Intel or any number of 1990’s tech giants, transitioning to the cloud and a new business model isn’t as easy as it once looked for the Larry Ellison led kingpin.

Here is the last decade’s stock performance:

Within client accounts Oracle has been reduced just 2 accounts and a total weight across all accounts of less than 1/2 of 1% of all assets.

When management stopped disclosing or breaking out the cloud segment and added insult to injury by never bothering to tell analysts, it was like Apple saying it was going to stop disclosing iPhone metrics: whatever management tells you that they will stop disclosing, you know its likely bad news for that segment.

Per one sell-side report, the cloud grew just 21% y/y last quarter and cloud is estimated at 10% – 20% of revenue per Morningstar. ERP is another 10% of revenue so – given the legacy business – assume that 70% of Oracle’s revenue isn’t growing or is only growing low-single-digits as the forward estimate growth rates imply.

If and when the cloud does get traction Safra Catz and Ellison will be screaming it from the tree tops. Right now though, “newco” is acting a lot like “legacyco”.

The stock is fairly valued and the capital return is generous, but both cash-flow and free-cash-flow was weaker in Q1 ’20 (last quarter).

Thanks for reading.

(Assume none of this is advice and just a way for the author to do homework on coming earnings releases. Take everything you read on this blog with a healthy dose of skepticism and evaluate the content in light of your own personal financial situation. The capital markets can change quickly.)