Microsoft reports tonight, Wednesday, October 23rd, 2019 after the closing bell, with Street consensus expecting $1.25 in earnings per share (EPS) on $32.23 billion in revenue for 10% and 11% growth respectively.

The December ’19 quarter Street consensus currently is $1.27 on $36 billion in revenue for y/y growth of 15% and 11% respectively, while fiscal 2020 consensus (ends June ’20) is expecting 15% ($5.24) and 11% ($139.9 bl) growth, respectively.

Microsoft is lapping a tough quarter of good growth from September ’18 where revenue grew 19% and EPS grew 36% exactly one year ago.

Since the very strong Sept ’18 quarter, revenue and EPS has slowed gradually not unlike the SP 500.

Here is a quick summary of last quarter’s (June ’19) results:

- Revenue grew 12%, op inc +20% and EPS +7%;

- Both gross margin and op mgn expanded by 200 and 260 bp’s respectively y/y

- Mgmt guided to “double-digit” revenue and op expense growth for fiscal ’20

- Azure grew 74% y/y and all three segments saw “upside revenue surprise” in the June ’19 quarter.

- Forward EPS and revenue estimates rose after the fiscal 4th quarter report.

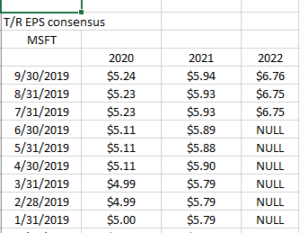

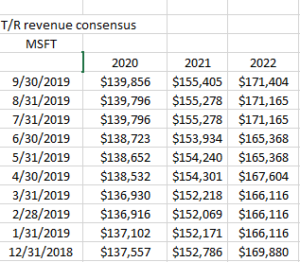

Here is the trend in Microsoft’s EPS and revenue estimates for 2019:

Both Microsoft’s forward revenue and EPS estimates have been gradually increasing both this year and for some time. (Estimate source: IBES by Refinitiv)

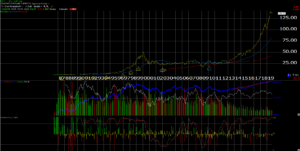

The Chart:

Microsoft’s monthly chart shows the breakout in the stock above the January, 2000 highs of $53 – $54 in 2016, so the stock has been a substantial out-performer for the last 36 months, running from the mid $50’s to the current price in the high $130’s.

Summary / Conclusion: Azure and the Intelligent Cloud business is the big driver of Microsoft’s revenue growth to the point where Intelligent Cloud is now roughly 35% of Microsoft’s total revenue and operating income, as Personal Computing has shrunk and Productivity (like Office 365, etc.) only seems to outpace Intelligent Cloud with a new release of Office 365. Intelligent Cloud has had the fastest revenue growth of the three segments for the last 6 quarters.

Technically, Microsoft is not part of FANG (Facebook, Amazon, Netflix and Alphabet) but it might be the best growth / momentum stock left standing if “value” and the small/midcap space start to outperform.

The Cloud – depending on who you read – is thought to be in the proverbial 3rd inning of the 9-inning ballgame, although cloud stocks have been weak now for the 3rd quarter.

Like a lot of tech stocks, Microsoft had to reinvent itself after the 1990’s PC and server explosion and it took the emergence of the cloud to do it. How the stock reacts tonight to earnings is anyone’s guess, although the EPS and revenue trends leave me confident that there could be continued upside to the stock with mid-teens revenue and EPS growth expected with it’s current 26x and 23x forward multiple. Like a number of tech companies, Microsoft’s cash-flow multiple (ex the balance sheet cash of $134 billion as of June 30) is 18x and 25x cash-flow which is more reasonable than the earnings multiple.

Still there is always short-term volatility risk around earnings reports.

Tech is losing momentum in terms of market leadership. Microsoft and Amazon report tonight and tomorrow night respectively. Both should be a significant tell for prospects around the Tech sector.

Microsoft has been a top position in client accounts since 2013 – 2014. Amazon as well. Right now, there is no reason to change, but every position is continually-evaluated with each earnings report.

(Long all the stocks mentioned above.)

Thanks for reading.

(Take any information on this blog with great skepticism and dubiousness. This information is being published simply to document and “think-out-loud” what is being done for clients accounts. Information like opinions can change rapidly and this blog might not be updated. Any reader should evaluate the above information in the context of their own financial profile.)