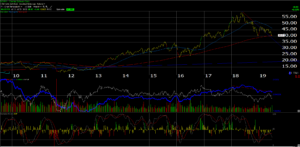

Attached is a weekly chart of Schwab (SCHW), clients 2nd largest holding behind Microsoft, and a mutual fund firm with $3.5 – $4 trillion in assets under management, assets greater than Goldman Sachs, Morgan Stanley and a host of others.

I was out to dinner a few weeks ago, with friends, one of whom is a senior VP with a well-known Chicago custodian bank, and in the last year his Mom had passed and had a couple of accounts at Schwab. This long-time friend noted Schwab’s “operational excellence” in his dealings with them, which given his position at a somewhat-competitor was telling.

This isn’t an advertisement for Schwab (which is this blog’s 3rd party custodian, holding all client assets) but I wanted a stock (or chart) that would highlight how the interest-rate sensitive financials have really lagged since early 2018, and in my opinion are now dramatically oversold.

The December ’18 low for Schwab was $37.83. That’s your line in the sand (so to speak).

Sector PE’s – check this chart:

The Bespoke research we get is some of the best research dollars spent for clients.

This “relative P.E” chart from the Bespoke crew is from the May 10, 2019, Bespoke Report. It caught my eye at the time given how cheap Financials were (and still are) but with the rate cut probabilities approaching 100% for July ’19, can that provide the catalyst for the sector ? Lower short-term rates, higher longer rates, and a yield-curve steepening might just be the “macro” that helps the sector.

Financial stocks received no boost from last week’s stress test results.

Here is a brief recap of YTD returns of client’s major Financial sector holdings:

- XLF: +9.75%

- KRE: +7.83%

- JPM: +12.76%

- CME: +2.88%

- SCHW: -3.7%

(Trailing return data courtesy of Morningstar, as of 6/26/19)

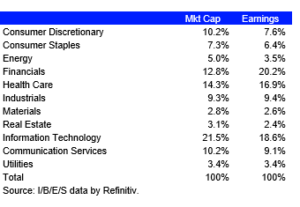

SP 500 sectors “Market Cap vs Earnings Weight”

Here is another stunning statistic: Financials today represent a 12% – 13% market cap within the SP 500, but have a 20% “earnings weight” within the same benchmark.

Summary / conclusion: While the Tech sector remains a substantial weight in client accounts, the Financial’s offset that “growth or momentum” component to client accounts, and seem to be far more “value” than growth today, with dividend yields and capital return. That being said, the problem with value investing is that long-term investors have to await the catalyst to trigger the out-performance for the sector. The 18-month lag in performance is getting tough to endure, which is typically the case when something owned for clients lags the SP 500 badly.

There could be a many reasons why Financials are under-performing: the biggest worry for me – and Jerome Powell even commented on it – was Facebook’s Libra currency and what that could mean for the financial system. Needless to say that could be disruptive to say the least.

But this is value investing. When Joel Greenblatt, the famed author, B-school professor and value investor came to Chicago last December ’18 to speak at a CFA luncheon, he noted an amazing stat:almost 45% of managers with exceptional 10-year track records (upper decile performance) spent at least 3 of those years at the bottom of the rankings (showing patience for the catalyst to arrive, and those are my words, not the Professor’s).

If you are long financials stocks, continue to be patient.

Thanks for reading.