This blog post addressing Financial-sector earnings came out Thursday night, which didn’t help readers, so i wante dto do one more dissection of expected SP 500 2019 earnings and make the case for Financials from a different perspective.

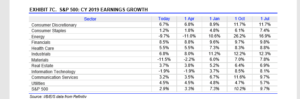

The above I/B/E/S by Refinitiv table from This Week in Earnings shows that of the 11 SP 500 sectors, Financial’s are expected to show the strongest EPS growth this year.

Will that change this week with the number of Financials reporting ? Sure it could, but after Friday’s results, it’s not expected.

However lets dissect the above data a little more: which sectors had the biggest percentage declines in earnings estimates from October 1 ’18, or the point when the correction started ?

- Cons Disc: fell 500 bp’s or 43%% from Oct 1;

- Cons Spls: fell 490 bp’s or 80% from Oct 1;

- Energy: fell 3590 bp’s (wow!) to -9.7% from +26% – the buyout of APC will put a bid under parts of Energy;

- Financials: fell 120 bp’s or 1.2% for a 12% decline in 6 months;

- Health Care: fell 280 bp’s or 2.8% for a 33% drop. Health Care always follows this pattern – actual sector growth should end up near 10%;

- Industrials: fell 540 bp’s or 5.4% for a 44% drop;

- Basic Materials: fell 1850 bp’s or 18.5% to – like Energy huge drop from big positive to big negative;

- Real Estate: fell 270 bp’s or 42%;

- Technology: fell 1040 bp’s or 10.4% from 8.5% to -1.6%;

- Communication Services: fell 840 bp’s or 8.4%;

- Utilities: fell just 20 bp’s from 4.7% to 4.5% or just 4%;

- SP 500: fell 730 bp’s or 7.3% from 10.2% to 2.9%;

(Source: IBES by Refinitiv, page 19 of This Week in Earnings. Calculations are my own)

Moral of the Story ?

Financials show that the Street is expecting not only the highest rate of absolute earnings growth heading into the bulk of Q1 ’19 earnings, but that of all the sectors – except Utilities – Financials have shown the least degradation of expected earnings growth of all the SP 500 sectors.

In other words, the expected 8.5% growth rate for Financials has held up despite heavy negative revisions for the rest of the SP 500.

Have SP 500 earnings been revised too low i.e. have Street expectations gotten too negative ? I do believe that’s the case, but that is one opinion.

Take all forecasts and opinions with a healthy dose of skepticism.

The numbers show that there is a good case for being overweight Financials in 2019. To be fair to readers, Ive been overweight the sector for several years. Too many positives for the sector, not the least of which is a bull market in stocks and credit this year, but the valuations are reasonable and the sentiment is poor.

Thanks for reading.