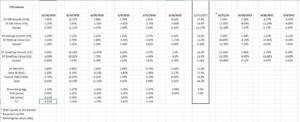

The style-box update as of 11/16/18 is actually a little late: for some reason, the update wasn’t made for September 30th. It is typically done every 6 weeks for readers.

The big change since mid-August is that mid-cap and small-cap “value” styles have not held their value as much as would otherwise be expected for “value” segments, in fact mid-cap value has fallen roughly 8% and small-cap value 11% since mid-August. Growth has fallen more in percentage terms but is still at a substantial performance premium in large-cap and small-cap segments.

In mid-cap, the growth style’s performance premium has narrowed considerably since 2017 and throughout 2018. I’m not sure why that is happening.

The Bloomberg Barclays Aggregate (the bond market equivalent of the SP 500) is now roughly flat in terms of total return over the last 23 months.

Summary / conclusion: Even with the crushing of FAANG stocks in the 4th quarter, large-cap growth continues to be the best returning style-box asset class as of mid-November, 2018. It was 2016 where we saw a substantial performance premium by value over growth, and then since 2017, that flipped back to growth. In 2016, there was Brexit and then there was the US Presidential election. Looking at charts of the 10-year Treasury yield and the US dollar (UUP) in 2016, it was a tale of two halves to the year: the US dollar was weak, and the 10-year Treasury rallied to its 2012, 1.38% yield retest, and then after Brexit and after the US Presidential election, the 10-year yield and the US dollar rallied rather sharply.

Is there causality between 2016 and the value style outperforming that year ? I certainly can’t draw that conclusion.

The point might be don’t give up on value yet. It will have its day in the sun once again.

Thanks for reading and a safe and restful Thanksgiving to all.