One of the themes written about over on Seeking Alpha the last 10 years is the “Original (Tech) Gangsters” which represented the growth giants from the 1990’s, which includes Microsoft (MSFT), Intel (INTC), Oracle (ORCL), Cisco (CSCO) and even IBM to some extent although IBM was around long before the PC and server-centric Wintel giants that dominated in the 1990’s.

The moniker must have gained traction (and this is being written in with a little tongue-in-cheek) since even Aswath Damodaran, the NYU Stern School of Business valuation guru and prolific valuation author, talked about Old Tech vs New Tech in a recent CNBC interview. Professor Damodaran talked about differentiating between the New Tech like the Cloud/Mobile/Social giants that are Twitter, Facebook, maybe even Amazon to some extent although I think of Amazon as having a foot in both worlds, since Amazon was a thing in the late 1990’s, versus the Wintel market-share colossus from the late 1990’s.

The valuations are more reasonable on Old Tech, as Growth became Value from 2001 through 2009, while the New tech or New Growth behemoths like Facebook, while feeling their first regulatory backlash over data have yet to see the kind of PE compression and growth collapse felt in the early 2000’s.

So here’s the point of the article: with the Cloud and Azure, Microsoft has successfully reinvented itself and using the existing Windows user base, which has once again become an incredible competitive advantage, Microsoft with Azure has transformed into a Cloud giant or “New Growth” giant, with expected 3-year revenue growth of 11% and EPS growth of 15%, respectively.

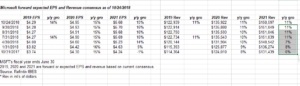

Another metric that might be of interest to Microsoft investors is operating income. Operating income growth has languished since the early 2000’s once the secular buildout of corporate PC’s and servers began to languish, but Microsoft’s operating income growth for the last 4 quarters, (measured on a 4-quarter trailing basis), grew:

- Q4 ’18: +20%

- Q3 ’18: +19%

- Q2 ’18: +12%

- Q1 ’18: +10%

These are the best rates of growth since a period in 2011 and then again in 2008.

Microsoft’s fiscal year ends June 30 and 4-quarter trailing operating income is used to try and be a little more conservative about the calculation.

Summary / Conclusion: Trading at 22x average forward EPS consensus looking for 15% growth and roughly 15x cash-flow (ex cash) Microsoft is not dirt cheap on a valuation basis, but over the years I’ve found that truly attractive stocks on a valuation basis are either dead money or value traps, sp in a secular bull market, buying somewhat expensive stocks may actually keep you away from the Bed, Bath’s, the Ford Motor’s and a whole bunch of other “cheap” names that eat up your capital, but suit the valuation moniker.

The key to Microsoft is that can Azure be a viable #2 to Amazon’s AWS (at a much more reasonable valuation) and can Microsoft’s legacy Windows and PC business support the stock with some growth, unlike Oracle’s and IBM’s and Cisco’s legacy businesses which are contracting at a single-digit rate.

Azure revenue growth is averaging 80% – 100% growth year-over-year while gross margins are expanding, which is a definite plus.

Morningstar’s fair value on Microsoft is $130 (which I think is conservative) and that valuation assumes a five-year revenue CAGR of 12% (consensus is currently at 11%) while Azure’s expected compound revenue growth is 43%, with overall operating margin expansion (10 years) from 32% to 44%.

All this being said, with the SP 500 now correcting as it is, Microsoft could very well selloff tonight after the report, even with a good quarter.

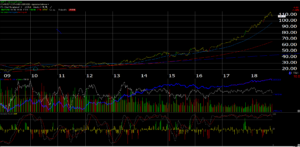

Solid support looks to be in the high $90’s and near $100 on the weekly chart.

Gary Morrow a long-time friend and excellent technician sees Microsoft support at $102 all the way down to the high $90’s which is the blue line on the above chart.

The final wild card is that in periods when growth and momentum underperform, while Microsoft’s valuation is a little more racy than traditional value stocks, the cash position will benefit shareholders. Microsoft had $134 bl in cash on its balance sheet as of June 30, and not only is it earning interest now, but it’s all free to come home to the US thanks to 2018 tax reform. (We can’t forget the $72 bl in term debt that MSFT has issued too.)

The important aspect for readers about Microsoft is that I suspect it will be a tech leader over the next 5 – 10 years, and a 1990’s leader that has successfully transformed its business model.

Use market selloffs to your advantage.

Thanks for reading.