As a long-time believer in the “sector” approach to investing, watching Technology and Financial’s lead the bull market of the 1980’s and 1990’s and then watching those two sectors get taken to the woodshed – first Technology in 2001 and 2002, and then Financial’s in 2007 and 2008 – it only reinforced my belief that starting with the top-down approach around sectors makes a lot of sense for clients. (The new “Communications” sector due to be implemented by Standard & Poors shortly will keep things interesting, It will represent roughly 10% of the market cap of the SP 500, which will put the sector inline with Industrial’s and Consumer Discretionary in terms of market cap weight, and it will / should reduce the Tech sector’s concentration in the SP 500.)

There were only 3 of the SP 500 companies in the “telecom” sector the last few years, so this change was a long-time coming. The new Communications sector should encompass given the composition, Technology, Telco and Consumer Discretionary (media). Norm Conley of JA Glynn out of St. Louis did a good write-up on the new sector, to be found here.

So how are client portfolio’s allocated today ?

Equity:

1.) Technology’s weighting was reduced after the 30% gain in 2017, but to be frank with readers, it was probably cut too much. The FIFO debate over capital gains recognition somewhat forced my hand in taking gains both in late 2017, and then early 2018, mainly the QQQ. The Facebook data and privacy issues also forced some selling and Apple was sold mostly from tax-deferred accounts in April ’18. (Still long Amazon, Google, some Facebook and Apple in taxable accounts.)

Technology’s weighting is now underweight in client accounts but the rotation involved buying out-of-favor small and mid-cap value ETF’s as well as straight Russell 2000 and mid-Cap ETF’s so it truly is better to be born lucky than smart.

2.) Financial’s are probably clients largest sector weighting today – at least temporarily, and the sector didn’t have a great 2nd quarter as the yield curve flattened and there continues to be worries over a global recession, which i think is highly unlikely. 2nd quarter 2108 earnings should be fine for the sector and the CCAR stress tests released last Thursday night, bode well for the sector in terms of dividends and buybacks. The only thing working against the sector is the now obvious bullish sentiment surrounding it. Don’t expect to add more to the sector other than possibly the KRE (regional bank ETF). KRE was up 7% – 8% YTD as of Friday, versus the XLF’s down roughly 4% YTD.

3.) Client’s Health Care weighting is rising but still slightly underweight between 10% – 13% of accounts. Pfizer is the largest position (definitely a value stock) with a 3.75% dividend yield. You can get the best of both growth and value within the sector. I like large-cap pharma like Pfizer, which has “value-trap” like characteristic’s since the company could be split at some point, although that breakup option was looked at in 2016 and then abandoned. (Never say never…)

4.) Consumer Discretionary: Amazon is the big dog in that yard and it’s a top 5 position in client accounts.

Technology, Financial’s, Health Care and Consumer Discretionary – just those 4 sectors comprise over 60% of the SP 500’s current market cap, although the creation of the “Communications” ETF will change some of this.

The utility and telco dividend trades, which were a highlight of 2008 – 2016 market have faded somewhat.

Clients top 10 weightings as of 6/30/18:

- Microsoft (MSFT)

- Schwab taxable money market

- Charles Schwab (SCHW)

- Amazon (AMZN)

- Schwab municipal money mkt

- Unlevered Inverse Treasury ETF (TBF)

- JP Morgan (JPM)

- Chicago Merc (CME)

- Bioetch ETF (IBB)

- KRE (regional bank ETF)

- XLF (large bank ETF)

- Some of these positions have been owned since 2009 – 2010. Some since 1997. Some positions are recently added i.e. in the last year or two.

- The above positions can change at any time.

Client’s bond allocations are explained in 4 positions:

1.) 5% – 10% position in the TBF

2.) A whole lot of cash sitting in the Schwab higher-yielding money market for clients, and the Schwab tax-exempt money market for tax sensitive clients

3.) T-Bills that have been riding up the yield curve and are spread out over the next 6 – 12 months.

4.) Clients do have a decent weight in the JP Morgan Strategic Income Fund managed by Bill Eigen. I like the philosophy, style and monthly fund calls.

Conclusion: Client accounts will likely outperform if the 10-year and 30-year yield continue to rise and Financial’s perform better than they did the last 45 days. The key “factor” to the portfolio as its is positioned today is for higher interest rates, likely driven by stronger economic growth, The key is really higher interest rates. I’m not convinced that the Treasury bulls – which have come out of hiding in the last two weeks – are right. This trade war – if it escalates – is potentially inflationary. The US hasn’t seen a 3.8% unemployment rate for any period of time since the Vietnam war and the last unemployment rate was 3.8%.

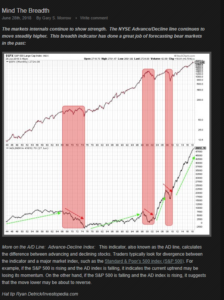

If readers want to hang your hat on something, take a look at this chart from Gary Morrow and his blog: This Week on Wall Street:

For those looking for a market correction of a significant duration, the breadth aspect to the SP 500 should tell you not to worry.

The Industrial sector looks good here, Large-Cap Value does have value here, and I still like Financials.

It will be interesting to see what if any this creation of the Communications sectors results in some temporary market distortions near its launch date in a few months.

Thanks for reading. Have a wonderful 4th of July please.