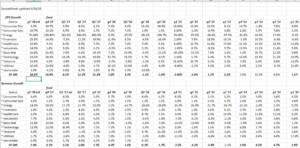

With the plethora of opinions out in the market about Q1 ’18 earnings expectations. the above spreadsheet should give good perspective on sector earnings and revenue growth looking all the way back to 2014.

While the financial media focus on earnings (for good reason) note how “revenue” comes in for the quarter. With the big banks on Friday, JP Morgan (JPM) beat on revenue as did Wells Fargo (WFC) but Citigroup missed slightly.

The remarkable stat to Q4 ’17 earnings was that 77% of the SP 500 came in above-consensus on revenue, versus the normal 60% “beat rate” and Q1 ’18 has started off as strong, but we need to see roughly half of the SP 500 report before drawing firm conclusions.

Thomson Reuters I/B/E/S data by the numbers:

- Fwd 4-qtr est: $162.02 vs last week’s $161.92

- P.E ratio: 16.4x

- PEG ratio: 0.83x

- SP 500 earnings yield: 6.10% vs last week’s 6.22%

- Year-over-year growth of fwd est: +19.86% vs last week’s 19.82%

Conclusion:

Ryan Detrick of LPL Financial wrote about the curse of the Presidential Cycle this past week, noting that quarters 2 and 3 of the second year tend to be “weak historically” so can we expect more of the same ?

The SP 500 is still range-bound between the January 26th high of 2,872.87 and the low of February 9th of 2,532.69 so until one of the range extremes is broken, then the market action is defined. Fundamentals around the SP 500 and the US economy are fair to good, but investor sentiment has turned very negative which is actually a positive for expected returns for stocks.

According to AAII investor sentiment data released Thursday, April 12th, pessimism has risen again over the 40% level while individual investor bullish sentiment has fallen back to 26%.

It’s tough to experience a real bear market with that kind of pessimism.

Think about too what that says about the state of individual investors today when – after a 21% year for the SP 500 in 2017 with little volatility the last two years – we see a minor correction in stocks, and investor pessimism rises over 40%.

Q1 ’18 earnings should be robust, and healthy, but much of that is in the numbers.

Q1 ’18 earnings optimism and investor sentiment today are somewhat like “dueling banjo’s” – they pull on each other, and in the end, the expectation is still a normal 5% – 10%, 7% – 12% year for the SP 500.

The SP 500 earnings yield is still above 6% – still think that portends more reward than risk in SP 500.

Thanks for reading,