The Technology sector is now roughly 25% of the SP 500 by market cap. (Not as high as what it was in 1999, early 2000 at 33%, but it’s getting there. )

The Tech sector has returned roughly 32.6%% in 2017, YTD, and the QQQ’s have returned 30%, per Bespoke’s Weekly Report.

Technology sector earnings (per Thomson Reuters I/B/E/S) are on track to be up 20% in 2017, and this 20% “expected growth” for 2017 could be higher by the end of February ’18.

We (meaning readers and investors) are in the sweet spot of the Apple iPhone “upgrade cycle” and that’s what I have been thinking about relative to 2018, which presumably is a big part of the Tech sector earnings

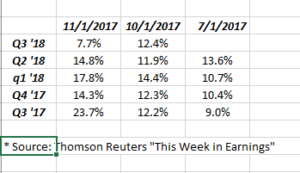

Here is what the next 5 quarter’s Technology sector estimates look like, and their trend the last 6 months:

A couple of things to note:

1.) The trend in Tech sector expected, forward, earnings growth has been decidedly and unambiguously higher since July ’17 (and again, the “normal” trend in forward earnings estimates at this time are usually for lower revisions).

2.) My own opinion is that this “strength” is probably due to the current Apple iPhone cycle.

3.) Note Q3 ’18 and the decline – that is the quarter when Apple will start to lap the iPhone 8 and Apple X, although Q4 ’18 will be the real compare to watch.

So what’s the point of all this ?

Since 2013, Apple (the stock) has had two nasty corrections in the off years of a major iPhone launch. While iPhone 8 and iPhone X are thought to be a “super cycle” an early look at the numbers – while still premature – says the “cycle” might be more normal than thought.

Bespoke has an interesting line in this week’s Bespoke Report: ” in case you’re wondering, the average change for the Tech sector in the year after it gained 20% or more has been 14.69%.”

Analysis/Conclusion:

Thinking about 2018 already for clients, but not ready to commit to a prediction for readers (remember, as a client once said to me, “predictions and opinions are like a—-les; everybody has one”) thus any comment about 2018 should be qualified with the fact that the factors driving stock market growth can change and change quickly.

The tech sector could see a “binary” year, with strong growth in the first half of 2018, and slower growth in the 2nd, with the variable being how “super” the iPhone SuperCycle turns out to be.

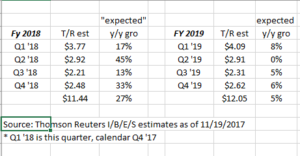

Another way of showing this for readers is to show Apple’s fiscal ’18 and ’19 EPS estimates and expected growth:

The point of all this is that – if the Apple pattern holds – the stock and Tech sector MIGHT have a very different to 2018 than 2017.

Technology is now a quarter of the SP 500’s market cap and Apple alone is 4%. The stock matters to the market.

(Long Apple,overweight Tech for clients (and have been for years) and always nervous.)

Finally, a quick look at the Thomson Reuters data by the numbers:

- Fwd 4-qtr est: $142.30 vs last week’s $142.39

- P.E ratio: 18x

- PEG ratio: 1.7x

- SP 500 earnings yield: 5.52% vs last week’s 5.51% and the 3rd consecutive weekly increase in the SP 500 “earnings yield”

- Year-over-year growth of the forward estimate: 10.77% vs last week’s 10.87% and the 5th straight week above 10% expected forward growth.

Basically 474 of the SP 500 have now reported Q3 ’17 earnings per Thomson. The overall numbers are solid, albeit distorted by both the Financial sector drag (hurricanes) and Energy’s easy comparative growth.

As we move in 2018, Energy will see more “normal” compares, relative to 2017.

Like retailers I wonder if I should start reporting “2-year avg growth rates” or 2-year comp’s for readers to eliminate some of the cyclicality of the sector.

Not a fan of Energy, no positions. Gasoline drives roughly half the distillation demand for crude oil, and nothing about electric cars and the auto industry tells me the US and the world will be consuming more gasoline.

Again, that’s an opinion.

Thanks for reading.