Yesterday, on this blog, we articulated the bullish case for stock prices for 2016 (here), referencing and linking to some of my favorite sources.

One of the mistakes i learned from the late 1990’s and 2007 was NOT giving freight to the bear case, the case that stocks could correct 20% – 30%, which in a bull market can happen at any time with the last 20% correction seen in the SP 500 occurring from May, ’11 to October, 2011. Since then we’ve seen a series of short, sharp 10% – 11% corrections where volatility and pessimism spiked, but the corrections lasted a series of weeks or months, not years.

The risk for investors in my opinion is not a 20% correction, but a sustained bear market where prices remain well below peak levels for years, like we saw from March, 2000 through March, 2009.

Here is what worries me:

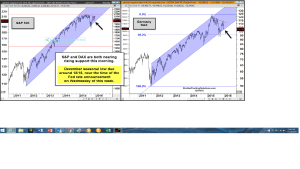

One of my favorite technicians, Ryan Detrick, recently joined forces with Chris Kimble, another excellent technician with his own charting business, and Chris’s first-rate technical work has been warning about how the SP 500 is testing the lower-end of its 5-year rising channel. With the SP 500’s close at 2,005 on Friday, December 18th, the SP 500 looks to be in a precarious spot in terms of the longer-term uptrend.

A break of this 5-year uptrend portends a longer-term bear market could be at hand.

Ryan Detrick’s Statistical Strategy work indicates that historically speaking, the last two weeks of every calendar year is usually one of the strongest of the year in terms historical SP 500 returns.

That is why this next two weeks matters greatly, in my opinion.

If the SP 500 rallies 2% – 3% to end 2015, the prospects for a return to a “normal” return for the SP 500 in 2016 improve greatly. And the fact is, I am still counting on that scenario to unfold, given the bearish sentiment that has arisen in the last week.

However, if the SP 500 sells off in the next 2 weeks, and closes 2015 under November ’15’s, 2,022 low print, then investors might have a bigger challenge.

Obviously, a close above the May ’15 – July ’15 all-time highs of 2,132 – 2,135 would be great, however I think most investors would take a 12/31/15 close above the SP 500’s 200-day moving average of 2,061.

Analysis / conclusion: One of the great shortcomings of the CFA exams (in my opinion at least when I took them), was the lack of any curriculum around technical analysis. Charts can relay important information to investors. Don’t ignore the study or analysis of price and volume in terms of imparting information to an investor. Now, what might the “fundamental case” look like to see a break in the SP 500’s uptrend ?

The US dollar worries me to death. A break of the 100 level which has capped the buck since late March ’15 would not be good, particularly if it keeps heading higher. In fact if the US dollar weakens and starts to trade back to 95 it could be a nice catalyst for the SP 500 to work higher. Since crude is traded in US dollars, it might help provide at least a modest bid for the crude complex, and I do think the Industrial’s have gotten hammered over the last year thanks to the dollar strength.

Per Bespoke, the US dollar strengthened 22% from October ’14 to late March ’15 primarily against the euro and the yen, which just wreaked havoc on the 50% of the SP 500 that has non-US revenue. In most cases the initial impact is translational, but ultimately it is economic.

If commodities stabilize, or even find a small bid, all the better. The XLE and IYE (Energy ETF’s) remain above their late August, September ’15 lows. The Emerging Market ETF’s (EEM, VWO) also remain above their August – September ’15 lows. Clients now have about a 5% weighting (roughly) in Energy and Emerging Markets, and Brazil based on the fact that – despite the headlines and the bearish sentiment – the ETF’s haven’t made new lows for the year.

The next two weeks matter – be careful out there.