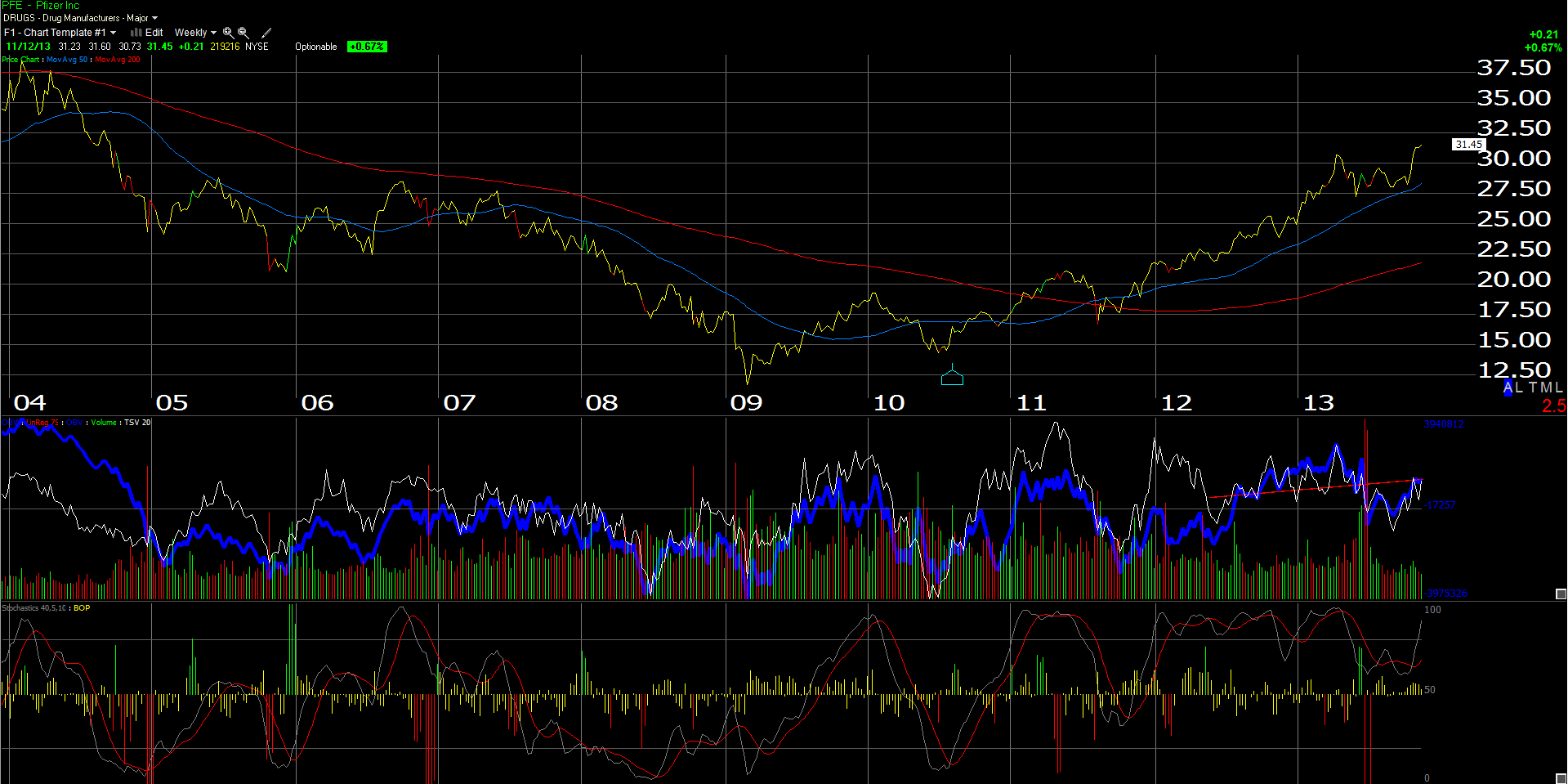

Above / attached is a weekly chart of Pfizer (PFE) showing its slow and steady ascent from the late 2011 lows near $18 – $19 to today’s trade just above $31.

Fundamentally, our ax in the pharma /biotech group is Dr. Mark Schoenebaum, ISI’s brilliant analyst.

Mark, along with his technician John Mendelson, was early on the group, and got us into the stock in early 2012, still at attractive levels.

There is a lot of shareholder value creation occurring in large-cap pharma, and Pfizer in particular: the animal health businesses are being scrutinized as PFE spun-off Zoetis in 2013, and returned the cash to shareholders in the form of a larger share repurchase.

Using a DCF analysis, we sold one half our Pfizer shares near $30 in the spring of 2013 (noted here from this blog) as the stock became fully-valued.

We’ve been watching that April ’13 high of $31.15 as well as the fundamentals, and this morning, as PFE continues to trade above the April ’13 high, we repurchased our remaining positions, that were sold in February ’13.

PFE seems to be at the forefront of the rest of the large-cap pharma names in terms of “enhancing shareholder value”. Operating expenses continue to get pared as revenue and EPS growth remain in the low single digits, and their recent decision to break out the income statement into 3 distinct business lines and “open the kimono” so to speak, led Dr. Mark to conclude that PFE could be spinning off some additional businesses over the next few years, and using a “sum-of-the-parts” analysis, upped his intrinsic value estimate to $39 per share.

We have always hung our hat on the cash-flow statement, and PFE’s looks pretty good. with that 8% free-cash-flow yield. PFE generates about $18 – $20 billion in cash-flow per year, with most of that free-cash, as drug pipeline R&D is expensed rather than capitalized, which actually understates their earnings power to some respect. PFE is returning a lot of that capital to shareholders in the form of dividends (3% current yield) and share repurchases, which were boosted this year by the Zoetis proceeds.

Here is a quick look at PFE’s Statement of Cash Flows as we have sliced and diced it:

That 8% free-cash-flow yield is what interests me. For our clients, with very little earnings and revenue growth expected the next few years, and thus expectations very subdued, the dividend and the share repurchases should set a floor under the stock, and limit the downside. In q3 ’13, PFE revenues declined just 3% y/y, which is better than the last few quarters, as the Lipitor generic drag slows.

Dr. Mark Schoenebaum’s point regarding the group was that with a PFE in the $20’s it wouldn’t take a whole lot of the pipeline drugs to hit to impact the stock price, and the price essentially discounted very few pipeline successes.

Merck and Lilly, both large-cap pharma with animal health businesses, could also follow suit of PFE gets the desired results from their “shareholder maximization efforts”.

After a 6-month consolidation, PFE is trading better and we have a little breakout, although volume is still light. We can be patient with it.

I do love cheap stocks with low expectations and good technical action, which is what PFE represents in the low $30’s.

Trinity Asset Management, Inc. by:

Brian Gilmartin, CFA

Portfolio manager