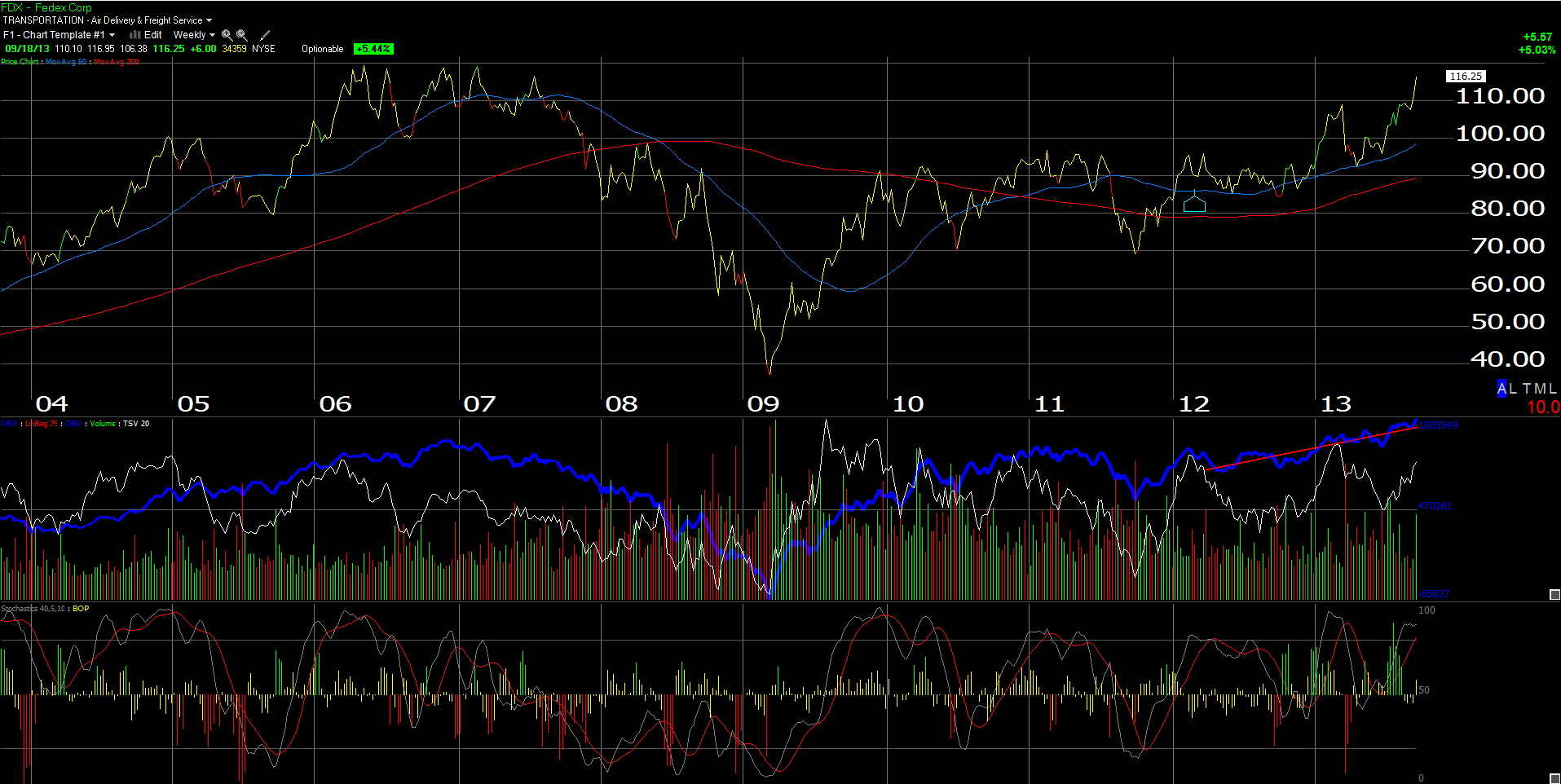

Lost in the Fed and the taper news yesterday, was the Fedex Corporation (FDX) fiscal q1 ’14 earnings report which drove a 5% rally in the stock on heavy volume.

FedEx Express which is FDX’s largest segment at 61% of revenues and a shrinking part of operating income, as the unit has been FDX’s problem child, reported flat Express revenues and an increase in operating income of 14.4%. A note out of Credit Suisse’s analyst Allison Landry, noted that US Deferred better than expected volume of +3.7% driven the better volume in Domestic Express, while International Export volumes of +3.6% drove the better-than-expected volume in International Priority.

No question this was a better quarter for FDX Express.

In addition, total FDX expense growth of +2% was the lowest year-over-year growth rate for total expenses in 5 years.

Express volumes have fallen in the last 6 years and in October, 2012 FDX announced a “profit improvement inititiative” of $1.6 – $1.7 billion in size, which really amounts to nothing more than a cost reduction program for FDX.

The cost reduction program is starting to bear fruit, and more importantly is occurring at a time with a recovery in global economies, so FDX should benefit from additional operating leverage as their fixed costs decline and volumes improve.

However Fred Smith did note that the business and market has changed, as the asset intensive freight companies look for cheaper alternatives to direct transportation, thus there continues to be revenue pressure from FDX’s customer base.

Current EPS estimates for fiscal 2014 and 2015 are $6.99 and $8.68 for expected growth this year and next of 12% and 24%, with FDX’s stock trading at 17(x) and 13(x) those forward estimates.

We would buy a pullback in FDX to the $107 – $110 area.

Morningstar has an intrinsic value on FDX of $122, while our internal earnings-based model ballparks intrinsic value in the $130 area.

Here is our SeekingAlpha earnings preview for FDX, written on Monday. The valuation is reasonable, and FDX will benefit from improving global economies, faster volume growth and lower expenses.

Trinity Asset Management, Inc. by:

Brian Gilmartin, CFA

Portfolio manager