GE is looking better from a technical perspective, which is a positive given the dramatic underperformance of the stock from its December, 2000, peak at $60 per share.

After the July ’13 2nd quarter earnings report, ThomsonReuters estimates for earnings per share are the exact same as they were prior to the report, with the Street looking for $1.66 and $1.82 in 2013 and 2014 for 9% and 10% growth respectively, leaving GE trading at 14(x) and 13(x) respectively, or inline with its growth rate.

The only fundamental aspect that has changed regarding GE is the start of outperformance in Europe, with the European stock markets having started to outperform since around July 1st, 2013.

We wrote an earnings preview on GE in early July, and noted that GE could be prepping a spin-off of GE Capital, and they have been returning more free-cash-flow to shareholders in the form of dividends and share repurchases.

Still, the stock appears fairly-valued to me on a p.e basis, and is trading about 8(x) cash-flow.

I think the wild-card is GE Capital. Management is doing their best to talk down the business, yet GE Capital – like all financial services – has rebounded nicely is now paying a dividend to the parent company. And the fact is, GE Capital is still a third of GE’s operating income, and that will be the case for some time.

Management and the Board of Directors have to do something to stimulate the stock price. Maybe it means getting rid of Immelt.

Technically, Gary Morrow is growing more bullish on the stock. Technicals always precede fundamentals.

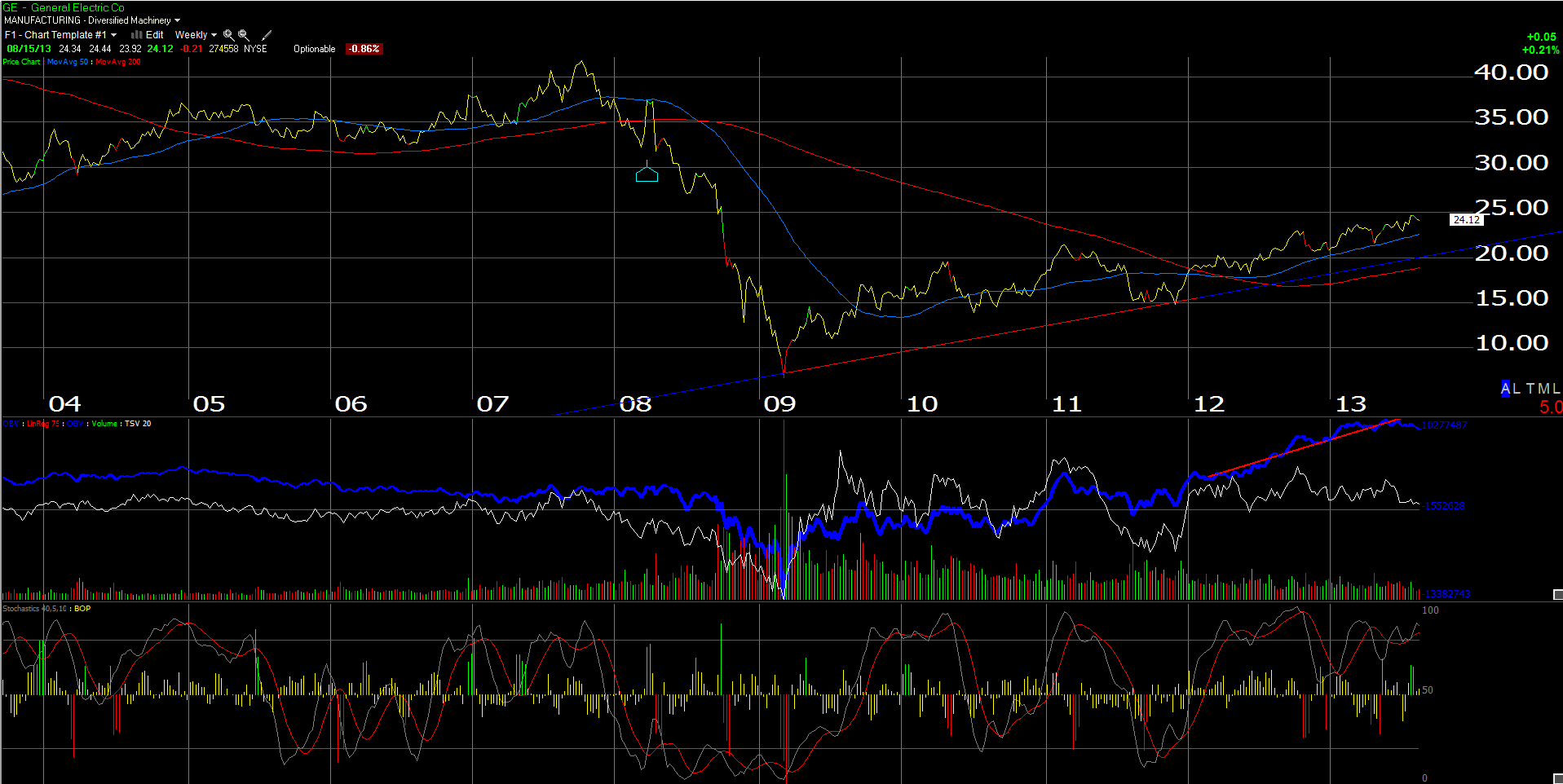

Here is Gary’s technical commentary on GE. (We couldnt attach his daily chart, given technical issues, so we attached the weekly Worden chart.)

“Since its powerful earnings inspired breakout back on July 19th General Electric has completely stalled out. GE zoomed over 4.5% the day it reported its second quarter results. Volume jumped dramatically as the stock moved into new 52 week high territory. The move was very bullish and was strong enough to put some distance on a heavy supply zone near $24.00. The four week aftermath has been less than inspiring. The high reached during the July 19th ramp was never challenged indicating a lack of follow-through momentum.

The fade off the July peak has been quietly consistent. Volume has remained below average during the pullback. Today shares have filled the breakout gap that was left behind on the 7/19 open. GE is now back down to a key support zone and may finally find a resting place. This key zone includes the stock’s March high as well as an upward sloping 50 day moving average. Slightly below is an important trendline that links GE’s April and July lows. The April low being the stock’s 2013 bottom. I would like to see the stock spend some time basing in this area. This type of action would be constructive and allow shares to build strength for a new rally leg. If GE fails here, which would take a close below $23.50, a key support area will have given way and more downside would be on the way. Under this scenario GE would be headed for a retest of the 200 day moving average near $22.75. Also here is the stock’s June/July lows. A recovery from this area would take quite a bit of time to develop. At this point I’m more inclined to believe the $23.50 to $24.00 area will hold.”

Not to steal Gary’s thunder, but I think the stock needs a catalyst, either a management change, or a spin-off, or some shareholder-friendly action to show that management is interested in improving shareholder return.

Given Gary’s technical analysis, maybe one is in the works.

Long GE (both Trinity and Yosemite)