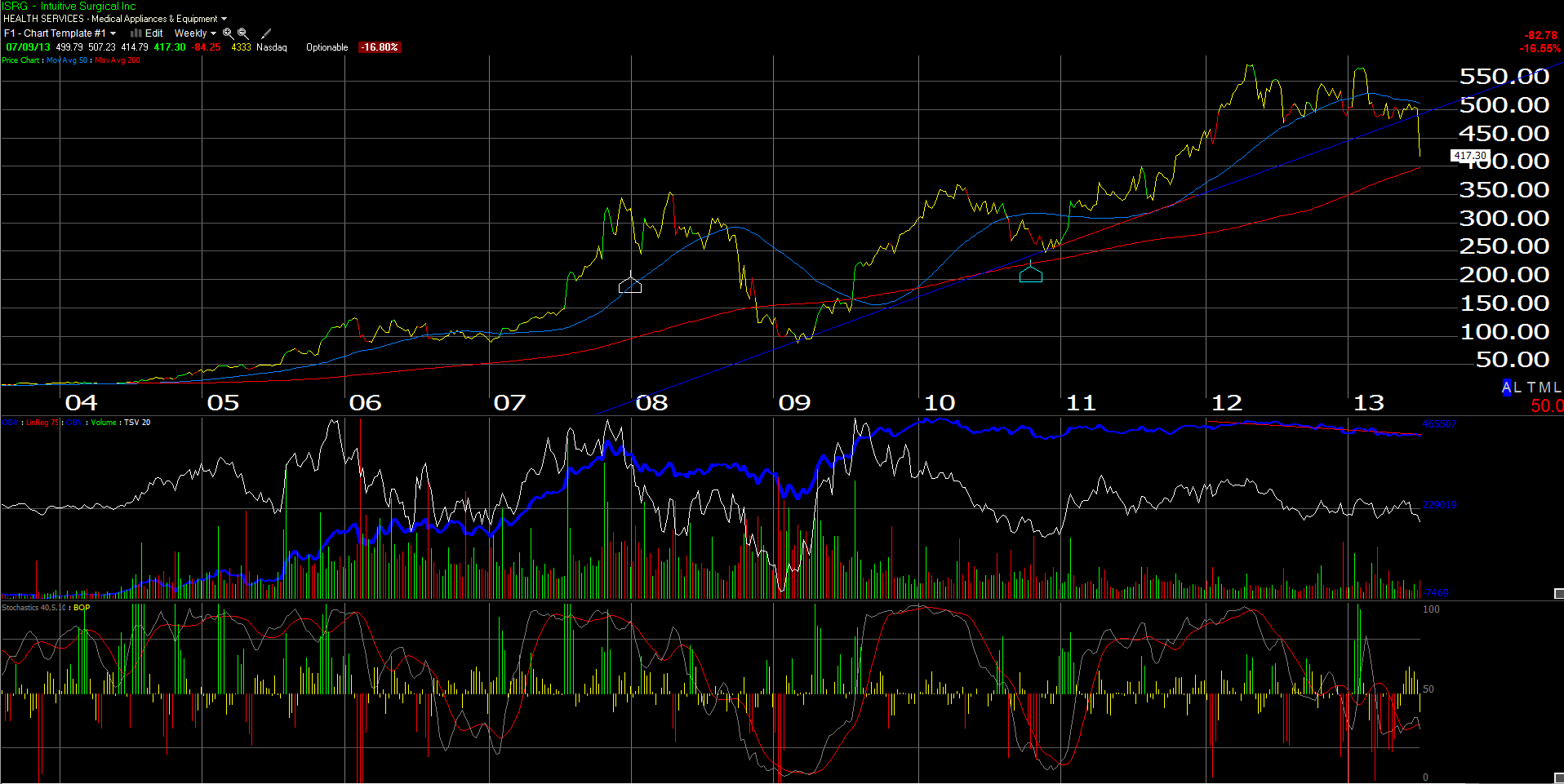

In the “it is better to be born lucky than smart” category, we sold all of our Intuitive Surgical (ISRG), with the last position being purged from client accounts, at $510 per share, about 60 days ago.

The double-top in the chart, from mid-2012, and then early 2013, meant the stock was on our radar screen, and its failure to move materially higher after decent earnings reports, also left me puzzled.

As a growth stock, we were always leery given ISRG’s lofty valuation, at 22(x) price to cash-flow and 8(x) price to 4-quarter trailing revenues, not to mention the 27(x) p.e ratio, for the 17% expecetd growth in 2013.

(Some investors are absolutely opposed to owning such a stock to begin with, but our philosophy is to own a blend of growth and value, and to keep the growth stocks with the higher valuations on a very short leash.)

That being said, today’s 17% price drop to the $410 area has us interested again in getting long ISRG, albeit with some qualifications. Morningstar – prior to the pre-announcement – had an intrinsic value on ISRG of $420 per share. We would really like the stock under $400, with the caveat that we will look at the change in forward revenue and earnings estimates over the next few days to see how bad the damage is.

One of my favorite technicians and a guy whose work I have very high regard for – Gray Morrow of Yosemite Asset Management in San Luis Obispo, California – wrote the following technical summary for ISRG given today’s action. Gary is a far better technician than I, although he does very little fundamental analysis.

————————–

From Gary S. Morrow:

Intuitive Surgical has taken a crushing blow this morning. The earnings inspired flush began with a huge gap lower open that dropped shares over 15%. This breakdown move has pushed ISRG below not only its 2013 lows but its 2012 bottom as well. Its no surprise that volume is running extremely heavy in the early going. By the close of trade today will be the heaviest downside day since the first quarter of 2009.

Despite this powerful breakdown a low risk entry opportunity may soon develop. The longer term charts show considerable support near the $400.00 area. ISRG’s 40 week moving average, which has not be tested since mid ’09, rest at $405.00. Slightly below is a major retracement level. With the exception of a steep pullback in the second half of 2010, ISRG traced out a huge bull run from its 2009 lows. This mega bull move carried the stock from $100.00 all the way up to the 2012 peak of $600.00. At the $400.00 area ISRG will have retraced 1/3 of this rally. Slightly below this important level is the 2010 high just above $390.00. This was a key turning point during the stock’s 2009-2012 rally. A spike high was left behind here before ISRG began working through a nine month pullback. The second, and more powerful, leg of the bull run began when this pullback ended in January of 2011.

I expect the $400.00 area to provide significant support as this week’s breakdown plays out. A base built in this support zone would be ideal rather than a quick upside reversal. A laddered entry would be the optimum strategy with initial purchases made as shares dip below $405.00. Additions would be made below $400.00 and again under $395.00. As this basing process plays out an oversold reading matching that of the 2010 bottom could be reached. Once this bottoming action is complete I believe patient ISRG bulls will be rewarded with a healthy recovery move. Initial target would be the previous 2013 lows set back in March at $455.00.

————————–

Finally, on a personal note, as someone who was diagnosed with a malignant, cancerous, prostate tumor that required surgical removal in December, 2007, the DaVinci and the quality of life that it offers I’m sure has left many males with a high regard for the company, the machine and the urological surgeons that spent the time to get trained on the machine. However, the company may have tried to push the procedure into too many other areas, too quickly.

This decline will re-set expectations.

We think opportunity looms for ISRG. We’ll try and keep readers updated as we move along, although we can’t promise such.

Trinity Asset Management, Inc. by:

Brian Gilmartin, CFA

Portfolio manager