If there is a better chart for measuring the trade-weighted dollar, or the dollar against the world’s major currencies either on a normalized, or a trade-weighted basis, shoot me an e-mail, and I will give you a shout-out with the chart.

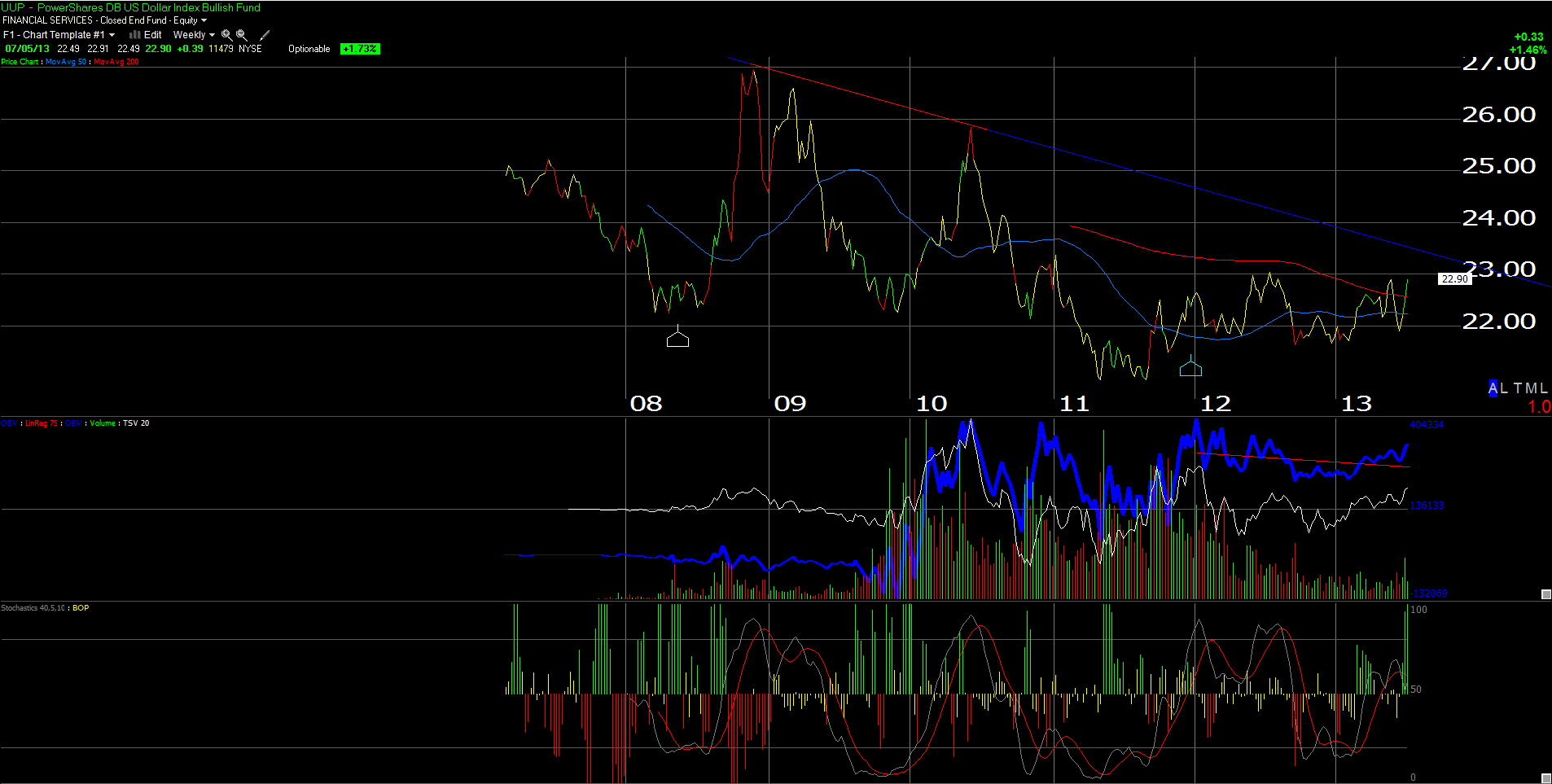

The above chart is the UUP, which is a combination of the Euro and Yen, but it is one of the few trading proxies I see for the greenback. The Euro is about 55% of the ETf, while the Yen is 15%. Technically there are 6 currencies that the UUP tracks or holds, but the Euro and Yen 70% of the total.

The dollars strength that has been discussed of late, still looks pretty tame on the chart, since the downtrend line that starts with the 2008 peak near $27.00 is still intact.

My first real job on a trading desk, back in 1990, was when the yen was trading at 220 to the dollar, and the Midwest was still working off the crushing strength that saw the dollar soar after Reaganomics, and the explosive growth in the US economy saw massive capital flows into the dollar.

There are a lot of different factors that effect a nation’s currency levels:

1.) Relative monetary policies – not an issue today since most of the globe’s major developed economy’s central banks have easy money policies;

2.) Relative fiscal policies – again, most countries like the EU, and the USA have reduced budget deficits and are following more austere policies, so for the most part nations are leaning the same way;

3.) Relative interest rates – the dollar might be strengthening based on the preception that thed Fed might be raising rates first, thus “real” interest rates might be higher in the US over longer periods of time;

4.) Relative capital flows;

5.) Relative Income and product levels;

6.) Perception – I believe the perception today is that the US is first and the festest to generate real economic growth;

The US dollar could be strengthening due to the fact that the US economy is still #1 in the world in terms of size, and is again, growing the fastest when ranked by GDP growth. The perception and the reality now that the SP 500 is trading at an all-time high, and US interest rates have started to rise, is that the US economy will start to be the real engine of growth for the world’s various economies, and that that growth phase is starting to become real.

If you ask me which of the above factors are most critical to the currency moves, it would be #3 or interest rate differentials, driven by real (in flation-adjusted) rates of return.

The UUP is one way to play the strong dollar. Another way to play currency is to figure out which sectors are major importers or exporters and adjust accordingly.

It is pretty clear the Yen will likely trade weaker over the next 6 to 12 months. The Euro might actually strengthen as that part of the globe moves to growth from stagnation.

We are simply broaching the topic for readers. There are many, many reasons currencies appreciate and depreciate.

We think the dollar continues higher, as the US economy recovers the fastest. Here was our “Macro Trade” link from early, May ’13.

The dollar’s extended strength becomes a threat to major exporters, which is what happened to Caterpillar, Deere, and the steel companies, turning the Midwest manufacturing belt, to the “Rust Belt” in the mid 1980’s.

It will take prolonged strengthening to really impair US growth in this cycle.

Trinity Asset Management, Inc. by:

Brian Gilmartin, CFA

Portfolio manager