Jim “RevShark” DePorre (@RevShark) writes for TheStreet, Jim Cramer’s operation (or former operation) and the former TheStreet.com, and one of Rev’s favorite and oft-repeated mantra’s is “Bear markets don’t scare you out, they wear you out” and it sure felt like that on Thursday, January 5th, 2023, after the strong ADP and jobless claims spooked both the stock and bond markets.

It was interesting though – despite the strong econ data Thursday – the TLT actually finished higher on the day.

The big banks and financials start reporting this week, actually Friday, January 13th, is the big report card day, and this blog will be out with a preview of the earnings this weekend or early in the week.

Here’s the list of big banks and financials scheduled to report January 13th, according to Briefing.com. The list has not been run against the Refinitiv expected reports, but I have found Briefing.com to be quite reliable.

SP 500 data:

- The forward 4-quarter estimate (FFQE) jumped to $228.38 from last week’s $222.91, which is the expected quarterly bump in the FFQE as we roll into a new forward quarter and drop off the old one. The new 4-quarter period is essentially calendar 2023 estimates.

- What’s interesting is that the FFQE is now $228.81 while the bottom-up calendar year estimate is still above $229 at $229.24 so consider all this.

- The PE ratio on the forward estimate is 17x versus 17.2x last week and 15.5x as of 9/30/22;

- Even w Friday’s rally, the SP 500 earnings yield was 5.86% as of the close Friday, the highest yield since November 4th’s 6%. (Remember, the higher the EY, the more attractively-valued the SP 500 is thought to be);

From a longer-term perspective, both 2022 and 2023 calendar year SP 500 EPS estimates were expected to grow 10% as of July 1 ’22. As of the first week of January ’23, the expectation is that 2022 will finish with 6% SP 500 EPS growth, while 2023, has been cut to an expected 4% EPS growth rate.

Those are sharp revisions in the last 26 weeks, and you have to wonder how much earnings weakness is discounted in current prices.

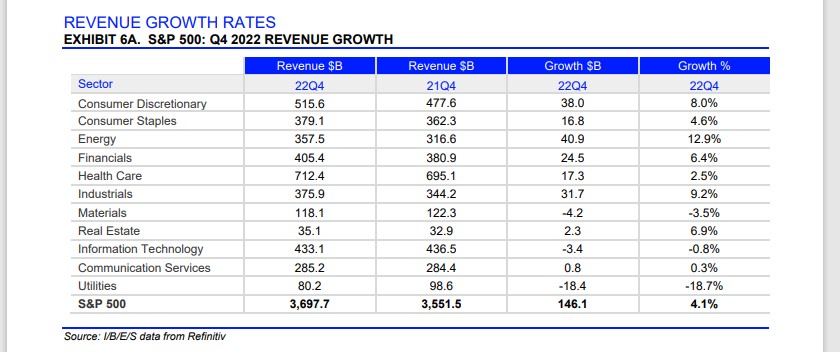

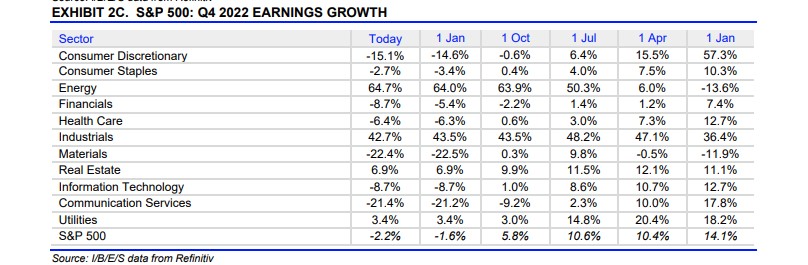

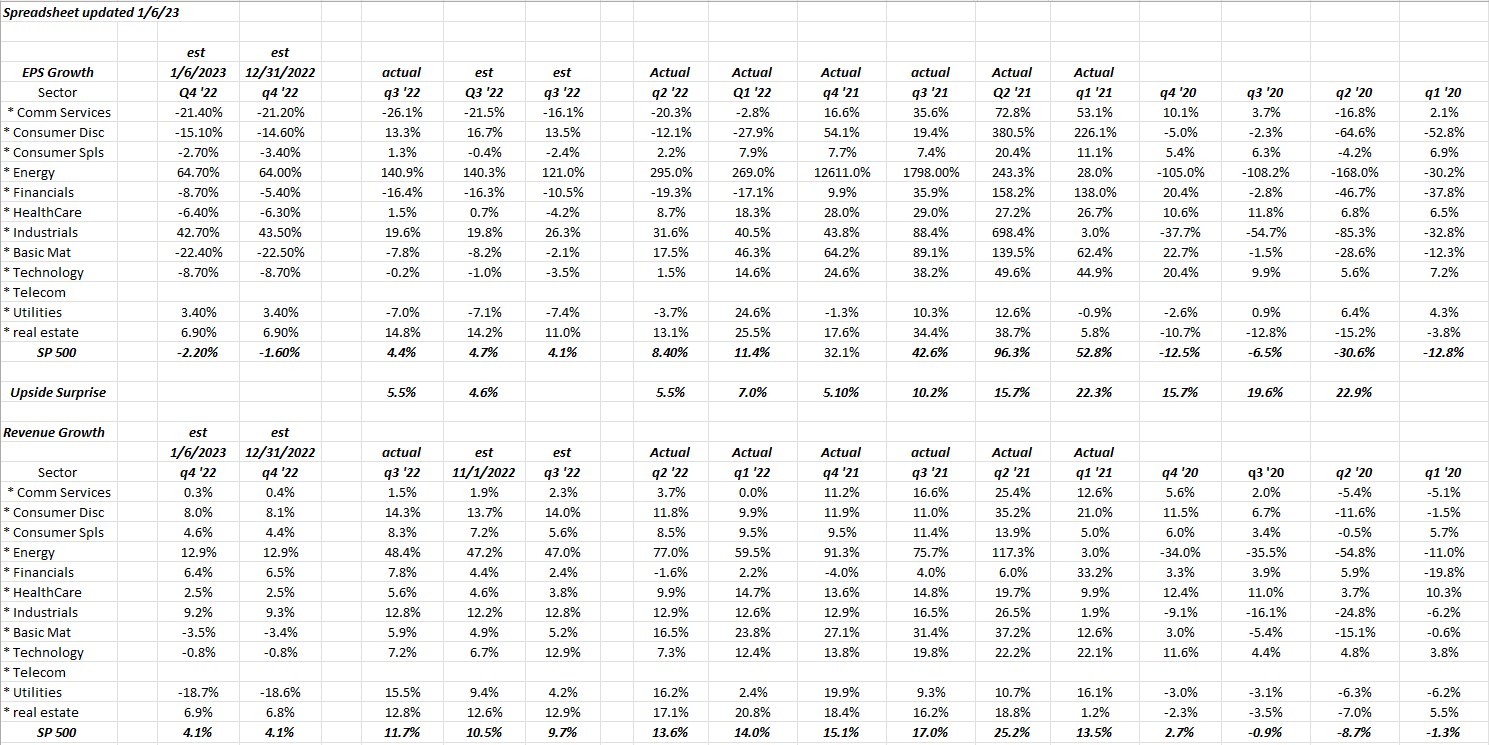

Q4 ’22 expected revenue and EPs growth:

While readers will recognize the Refinitiv reports on expected Q4 ’22 revenue and EPS growth for the SP 500, the excel spreadsheet is this blog’s own work and it shows the actual EPS and revenue growth by sector for the SP 500 starting from Q1 ’20. (The three columns devoted to Q3 ’22 results show how results trended over the quarter, and the two columns devoted to expected Q4 ’22 results show the changes in the last week.)

The purpose of the excel spreadsheet is to show the incredible drop and then growth in SP 500 EPS and revenue in 2020 and then 2021, and then we see experienced the next wave of comparisons – particularly within the tech sector in 2022.

So what’s the point of all this ?

It’s hard to imagine CEO’s and management teams being bullish about 2023’s EPS and revenue prospects given the Fed, and the slowing economic data, but also readers shouldn’t fail to consider we’re still living with the Covid affect and the tough (or very easy compares) within the SP 500 itself.

Technology had ridiculous compares in 2022 versus 2021 numbers, and Alphabet (GOOGL) and Amazon and Apple still face very tough compares in calendar Q4 ’22 versus Q4 ’21.

Energy is just the opposite: note how the expected Energy EPS growth for Q4 ’22 didn’t increase at all in the last 90 days of 2022, and while 60% growth is still pretty robust, the positive revisions have stopped and the “compares” for the Energy sector are much tougher in 2023. (This being said I hate the “percentage” growth; I’d much rather see a dollar EPS figure than y/y percentage growth or declines.)

The expected, overall, +4.1% revenue growth for the SP 500 is the lowest expected, y/y revenue growth for the benchmark since Q2 ’20 or the throes of the pandemic.

Technology’s expected -8.7% EPS growth and -1% expected revenue growth for Q4 ’22, is worse than Q2 ’19 which was the slowdown Jay Powell saw when he did the policy shift during Christmas week, 2018, and it’s the worst expected growth since – well – this blog started tracking quarterly data in 2012.

Technology could be looking at it’s worst y/y growth numbers for revenue and EPS in 10 – 11 years.

Summary / conclusion: Friday’s January 6th’s better-than-expected average hourly earnings in the December ’22 jobs report and the sharp contraction in Services ISM, sure put a bid under stocks and bonds on Friday, January 6th as investors get the first glimpse of what could be a shift in Fed policy. It was interesting that in CNBC’s Steve Leisman’s interview of Raphael Bostic, the Fed Governor, on Friday morning, January 6th, Bostic noted that the Fed isn’t targeting wage inflation but rather “demand” thus the ISM Services weakness, may have meant more to the market reaction than average hourly earnings.

There is more work that needs to be done over this weekend, so this blog post has to be kept short.

The Fed Gov’s are hard on the notion that there are no fed funds rate decreases being contemplated in 2023.

Remember though Powell shifted very quickly in late 2018.

In the market trivia column this week, the non-US markets had a very good start to 2023. Emerging markets tied to China and China itself had a good start to the year. The KWEB or the Krane Shares China Internet ETF was up 14.47% alone this past week, after falling 17% in 2022. At one point in late October ’22, the KWEB was down 47% – 48%. Quite a bounce. David Herro’s Oakmark International (OAKIX) fund was up 6% this past week. European banks are starting to move higher.

Take all this with considerable skepticism. All raw earnings data is from IBES data by Refinitiv, but the excel spreadsheets are the work of this blog, as well as the valuation calculations. Past performance is no guarantee of future results. Capital markets can change quickly, both positively and negatively. Back with more Sunday.

Thanks for reading.