Attached is a table from Briefing.com detailing the economic releases scheduled for this week, with the most important being Thursday, November 10th’s CPI report.

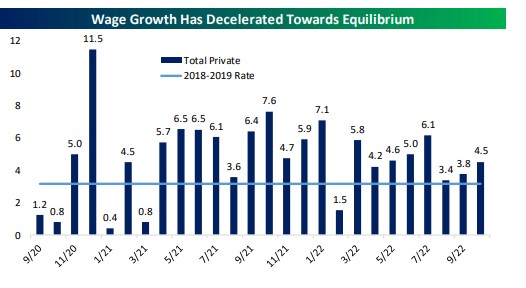

Last Friday’s October payrolls report showed continued cooling in “average hourly earnings”. (Here’s a chart from this weekend’s Bespoke report:)

What’s interesting about the Bespoke graph is that the blue line shows 2018 – 2019 compare. That surprised me.

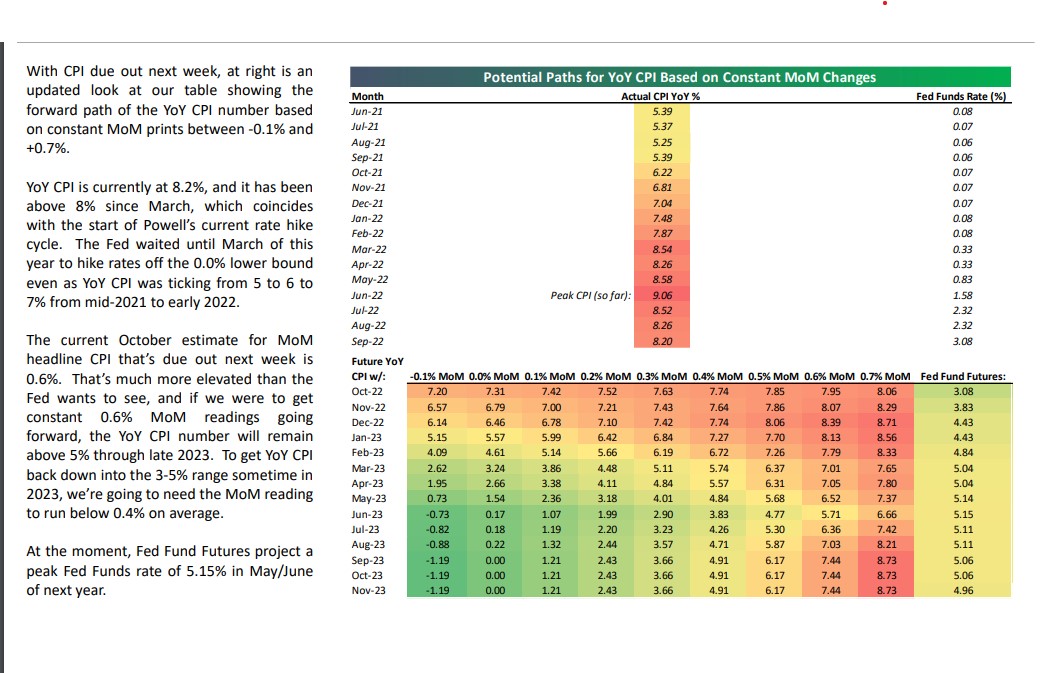

However, here is the Bespoke table on inflation that really caught my eye:

The bar at the top shows CPI decelerating (or disinflating) although still way too high. Peak CPI was in June ’22 at 9.06% per the bar chart in the top half of the page.

More interesting was that it was noted that inflation needs to come in below +0.4% rate in order to get CPI inflation back into the 3% – 5% range.

The Thursday report is expecting CPI to print +0.5% to +0.6%, according to the Briefing.com table at the top of the page.

Summary / conclusion: Expectations coming into Thursday’s CPI and Core CPI print are leaning “heavy” so to speak, meaning the street is expecting another hot number. Also listening to bond fund managers and the cacophony of opinions permeated every day in financial media, it may not be until next summer that we resolve this inflation issue.

The various bond asset classes in the US and Non-US were slightly lower this past week, even though the Fed boosted the fed funds rate to a mid-range of 3.875%.

Inflation matters to bond yields and bond yields matter to stock PE levels and valuations. It’s all starting with the inflation data.

From a trading perspective, this past week was interesting: the dollar started to fall, which seemingly caused gold to rally and you had a good rally across Europe and China. Rumors of a Chine re-opening started late in the week on what looked like a completely tepid comment by Xi.

The VanEck Emerging Markets Fund as well as the EEM and VWO, (the iShares and Vanguard emerging markets ETF’s), while the EMXC (emerging markets ex-China rose 2.1% this past week, so you can get a quick feel for how much was China and how much was the dollar. If China commits vocally to reopening, and the dollar falls sharply, we could see a powerful rally in non-US assets.

The 15-year annualized returns (per Morningstar data as of 9/30/22) for the VWO and EEM are +0.40% and -0.33% bp’s respectively.

Those aren’t typo’s.

Take everything here with skepticism and a healthy grain of salt. Past performance is no guarantee of future results and none of this is a recommendation to buy, sell or hold anything. Writing about all of this imposes a discipline to stay on top of and track the data.

Thanks for reading.