Forward EPS estimates were revised lower again this week, revision action that isn’t encouraging. What’s puzzling is that – when thinking back to the 4th quarter, 2018 correction after Powell had been raising rates since Q4 ’16 – the last monetary tightening cycle – the SP 500 rolled over almost precisely when the “forward 4-quarter estimate” FFQE, rolled over.

In 2022, not so much.

One reason could be that the stock market started correcting almost 75 days before the first fed funds rate hike in 2022, in addition it took about 5 months and 2 weeks to get to the 24% correction in 2022, while the speed of the correction in Q4 ’18 was not even 12 weeks.

Pay attention to price not predictions: the negative revisions are worrisome, but perhaps the earnings correction was fully discounted as of mid-June ’22.

SP 500 EPS data: (source IBES data by Refinitiv)

- The forward 4-quarter estimate (FFQE) fell to $234.05 this week, from $236.83 last week and now stands $7 below its July 1 ’22 peak of $241.22;

- The PE ratio on the forward estimate is now 17.7x

- The SP 500 earnings yield is now 5.65%, down from it’s July 1 peak of 6.31%;

- The Q2 ’22 bottom-up quarterly estimate rose to $57.44 from last week’s $56.09 for a 2.04% sequential increase.

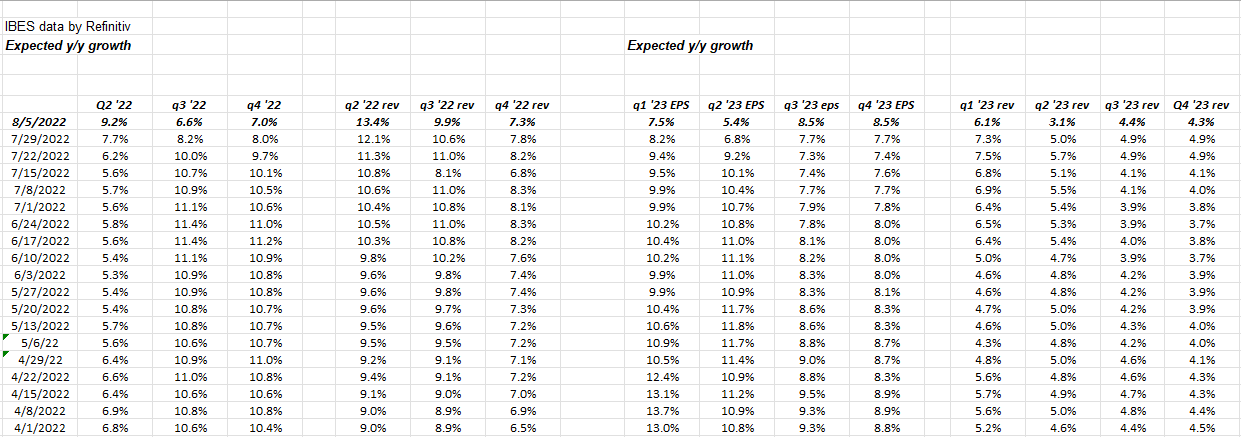

The Street or the sell-side consensus thinks the Q2 ’22 SP 500 earnings data is on the stronger side. That bottom-up quarterly estimate has risen nicely since early July, plus check out this table that is updated weekly from Refinitiv’s Earnings Scorecard:

Columns 1 & 4 are “expected” Q2 ’22 EPS and revenue growth for the SP 500. Now look at Q3 ’22 EPS and revenue growth and beyond and note the changes in expected growth rates since July 1 ’22. The revisions in expected growth rates continue to be lower, but they do jump around.

Bottom-up and top-down quarterly data:

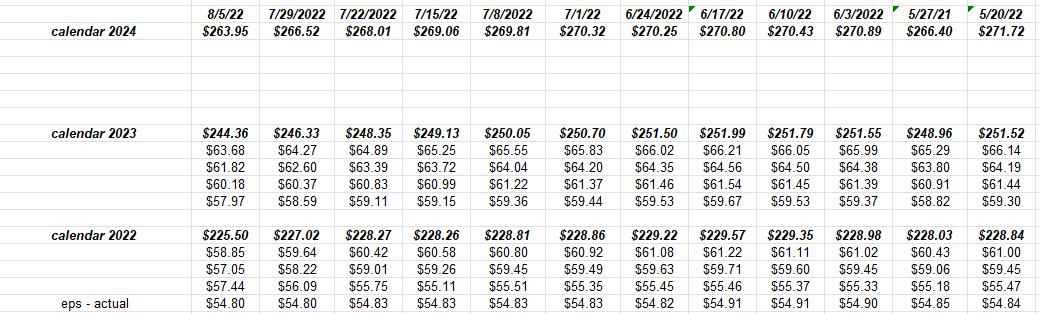

- The 2023 SP 500 EPS estimate peaked at $251.99 the week of June 17th, 2022, and has fallen to $244.36 or 3% as of August 5th, ’22.

- The 2022 SP 500 EPS estimate peaked at $229.57 the week of June 17th, 2022, and has fallen to $225.50 or 1.8% as of August 5th, ’22.

What’s interesting about this data is that the SP 50 estimates peaked the week of June 17th, almost exactly coinciding with the peak in the 10-year Treasury yield of 3.50% and the bottom in the SP 500 of 3,636.87.

The CPI and PPI data next week remain very important:

Briefing.com is forecasting Wednesday’s overall CPI to be +0.3%, while CPI – Core is expected at +0.6%, which I had to look at twice to make sure that was read correctly. Thursday’s PPI is expecting +0.3% and +0,4% respectively.

The PCE data last week came in exactly inline, and not better, thus it was a slight disappointment.

Gasoline is 2% – 3% of the average American household budget thus the steady decline in gasoline should be of some help with such a strong July jobs report.

Summary / conclusion: The peak in the forward SP 500 EPs estimates coinciding with the bottom for the SP 500 in mid-June ’22 is quite puzzling since the 2018 tightening cycle showed the Q4 ’18 correction began almost precisely with the SP 500 peak in the forward estimate in late September ’18. (LizAnn Sonders and Bob Doll, who was then at Nuveen, called the top or the coming correction in the SP 500 almost exactly in late September, 2018.)

According to Briefing.com, Home Depot, Lowe’s, Walmart, and Target report their July ’22 quarter starting the week of August 15th, ’22.

With Walmart’s and Target’s excess inventory, you’d think that would have to pull inflation numbers lower as prices are cut to clear that inventory out of their stores, given that Target revenue last year was $106 billion, Walmart’s expected revenue in fiscal 2023 is $597 billon, and Amazon’s expected revenue in calendar 2022 is $522 billion. Between Amazon and Walmart alone, there is over $1 trillion in expected revenue, in a $22 trillion economy.

Maybe it’s too easy an extrapolation, but if Walmart and Target wanted to clear their inventory problem, I wonder what pressure that would put on the CPI. (Just thinking out loud.)

Readers need to remember too, this morning’s July ’22 nonfarm payroll report is NOT in the estimates published today by IBES data by Refinitiv. The team Refinitiv I deal with – great crew, always responsive to questions – have told me for years that the data cuts off as of Thursday night. Would the jobs report alone send revisions positive ? Probably not, but it certainly (you’d think) have an impact on consumer discretionary and those sectors sensitive to consumer spending.

We’re in a bit of a twilight zone in terms of economic data, earnings data, asset class behavior, etc. etc. The dollar reacted logically to the strong July jobs report this moving higher today, and I still think – regardless of who wants to argue with me – that the 20-year high in the greenback in June ’22 made a difference in SP 500 EPS and revenue at the margin, and that it’s weakening matters even more.

Through June 17th this year all we were worried about was inflation, then after that it was recession and falling commodity prices, and now with the July jobs report, the scenario flips to “maybe the US economy isn’t that weak” but we still have to deal with Fed tightening (again) in September and November ’22.

Take all this with substantial skepticism. I’m as puzzled as you are. CNBC is loaded with those bullish and bearish, but there’s nothing wrong with being right in the middle and waiting to see which way the data and the markets break.

Clients and readers know my long-time favorite technician is Gary Morrow (@garysmorrow on Twitter) and he tells me that the 4,115 to 4,222 area on the SP 500 is a key band. It represents February ’22 lows and a key fibonacci level I believe. As someone who isn’t a technician, I am watching the March ’22 lows at 4,161 to 4,157 which were the lows put in for the SP 500 right before the first rate hike on March 15th, and then the strong quarter-end rally to end Q1 ’22. We popped over those levels on Wednesday and then slipped right back below them before the close.

Inflation needs to be “better-than-expected’ going forward though to really help the stock and bond markets since it’s the only think the Fed and Jay Powell care about today.

Be skeptical of everything. Look how many predicted the July jobs report this morning (as in no one). Truth be told, that kind of report is better for stocks in the long run, than bonds.

Thanks for reading.