SP 500 earnings have seen a little deterioration in the last few weeks, with this week’s data, coming from the weekly “This Week in Earnings” report published by Refinitiv, as of Thursday night, July 14, 2022. When we get a slew of Friday morning earnings releases as we did today, they aren’t included in the TWIE numbers (revisions, etc.) so it isn’t known until Monday or Tuesday what the impact is on the overall data.

Overall Q2 ’22 SP 500 revenue and EPS growth is expected to come in at +10.8%, and +5.6% respectively. Ex-energy, those two numbers fall to 6.6% and -3.4%.

Energy is expected to have an uber-strong reporting season for Q2 ’22 – you should expect substantial upside surprises in both EPS and revenue – and then, unlike the rest of the SP 500, energy sector comp’s get tougher as you move through Q3 and Q4 ’22, and into Q1 ’23.

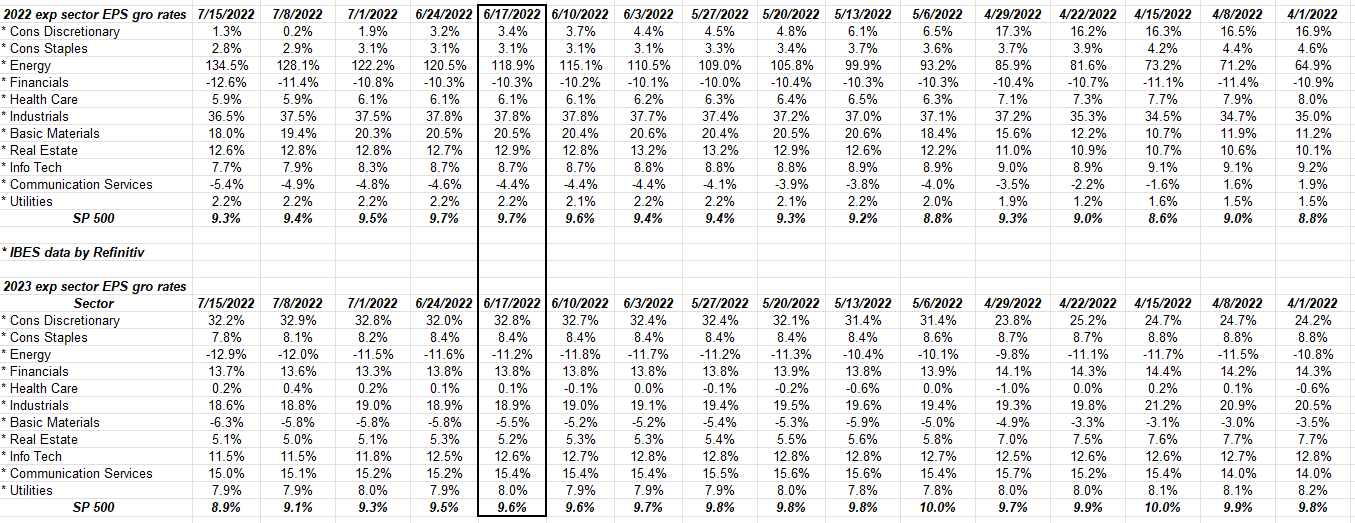

This data set shows – in black border – the week of June 17th, 2022 when SP 500 EPS growth for both 2022 and 2023 peaked.

Note the expected growth rates for energy and basic materials sectors in 2023. That surprised me, although assume it could change by the 3rd quarter of ’22.

Since the week of June 17, ’22 for 2022, note how energy is the only sector with higher expected growth rates for full-year 2022 each week, while the rest of the SP 500 (utility sector is flat) is seeing mild downward pressure. This isn’t all that unusual. Next week 72 SP 500 companies report and thus by next Friday, 7/22, 100 SP 500 companies will have reported Q2 ’22 earnings.

Analysts are cowed right now given the decline in the SP 500 YTD of -19.84% (as of Thursday, 7/14/22), thus there is little reason for an analyst to boost numbers until the results are seen and management can model that higher revisions are warranted. It’s a “show me” market in terms of generating higher EPS and revenue revisions.

According to Briefing.com, Goldman Sachs (GS), Bank of America (BAC) and Charles Schwab (SCHW) all report before the opening bell Monday morning, July 18th, 2022.

Tesla reports next Wednesday, after the close per Briefing.com. Tesla is the first of the “mega-cap 8” as Ed Yardeni calls them, which is the top 8 – 10 market names that dominated SP 500 returns for the last 3 years.

SP 500 data:

- The forward 4-quarter SP 500 EPS estimate fell this week to $239.98 vs last week’s $240.83. This is the third week of the last 4 weeks where readers are seeing a sequential decline in the forward EPS number;

- The PE ratio this week is 16.1x;

- The SP 500 earnings yield is 6.21% this week versus 6.18% last week, and the 4.77% to start the year;

- The Q2 ’22 bottom-up, quarterly EPS estimate sits at $55.11. The last three quarters – starting with Q3 ’21 data, through Q1 ’22, have NOT been able to print above $55 per share.

Rate-of-change measures:

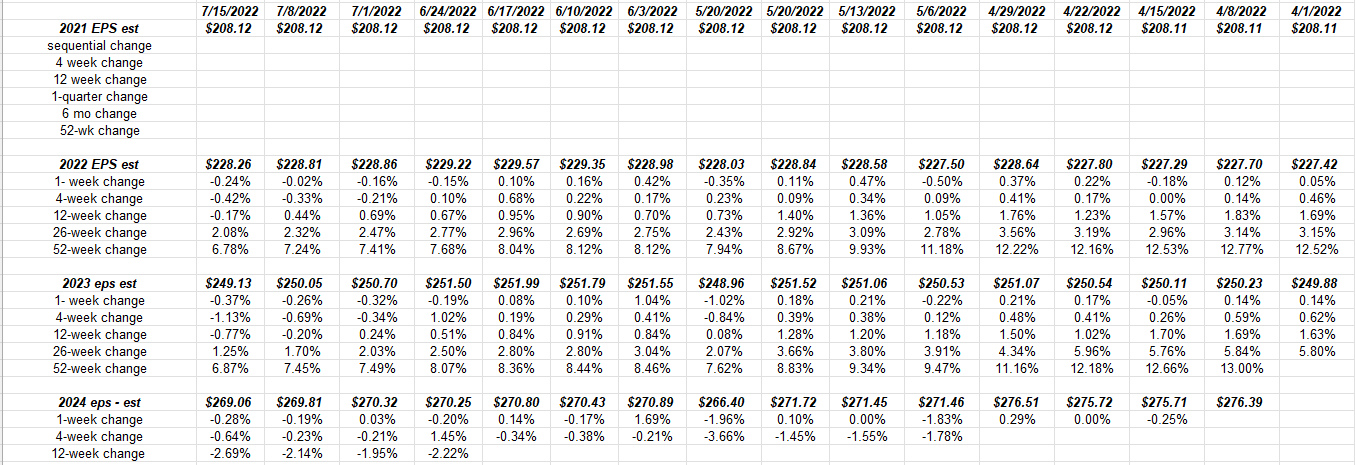

Note that while the absolute SP 500 EPS numbers for 2022 and 2023 have remained constant and within $1 or $2 of the April 1 estimate, the “rate-of-change” is slowing since the compares for the 26 and 52 week change are against 2021.

While 2024’s EPS estimate is down about $7 it’s still too early to draw any conclusions.

Readers should watch the calendar 2023 SP 500 estimate as we move through the 3rd quarter since forward 4-quarter estimate includes the first two quarters of 2023.

Right now, the dollar estimates are stable: that could change when the big five – Apple, Microsoft, Amazon, Alphabet and Meta – all report the last week of July ’22.

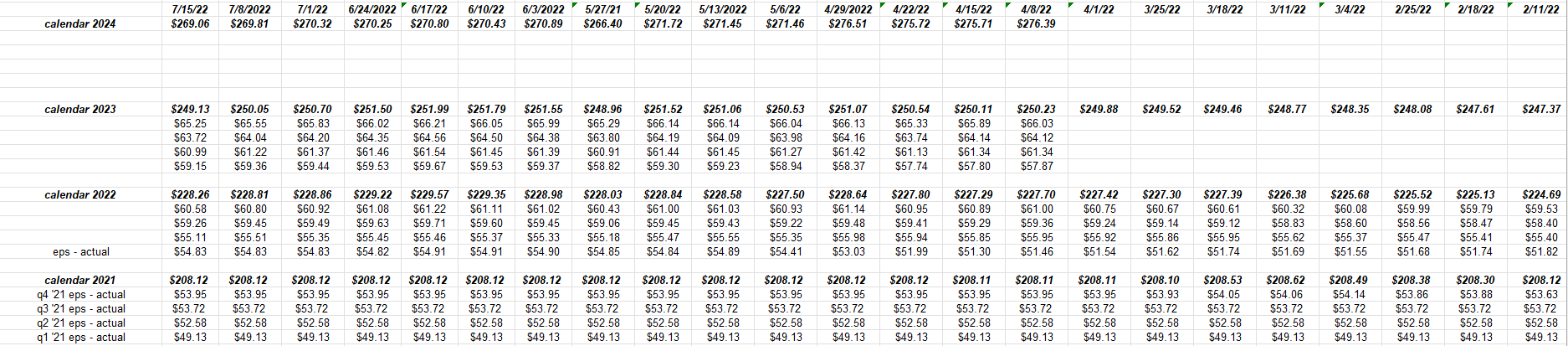

Quarterly bottom-up dollar estimates:

This table shows simply the trend in quarterly bottom-up SP 500 EPs estimates since late February ’22.

It’s less descriptive as a data point.

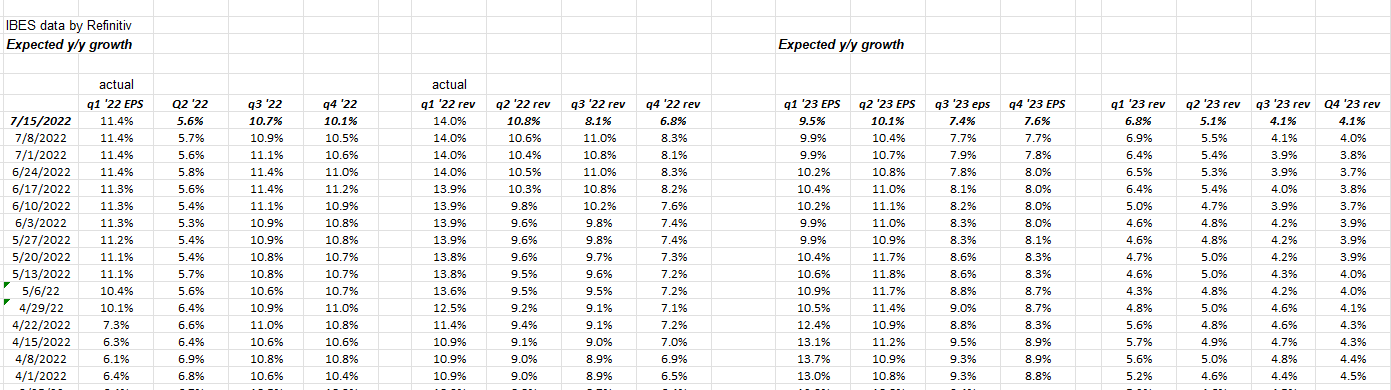

Quarterly expected SP 500 EPS and revenue growth rates:

This is a section from Refinitiv’s “earnings scorecard” that shows quarterly expected growth rates.

Note this week the downward revisions in the expected revenue growth rate for Q3 and Q4 ’22 revenue.

Let’s see if in subsequent weeks that gets revised higher again. These week-to-week data points can jump around.

Summary / conclusion: Linking the SP 500 earnings update from last week here, the bearishness that is a constant these days is – as Bespoke notes – typically a good contrarian indicator heading into the earnings season. No question the sell-side analysts are nervous and historically that’s been good for stock price action during earnings season.

What’s interesting to me is that the May ’22 low of 3,810 is still intact as a weekly low, and the June 17th 6 month low of 3.636.87 also hasn’t been approached. Even with the bad CPI data this week, those two key SP 500 technical levels that I think matter, are still in place.

The inflation story grows old, but the recession story is young. The recession issue might end up affecting the yield curve and bond market.

Tesla’s Q2 ’22 earnings report is a big deal next week since it’s the exact kind of “high PE, high valuation” stock that has not worked this year, after the outperformance of “large-cap growth” the last three years. Netflix too on Tuesday night after the bell, will be interesting. It was never held in size, and it still hasn’t been bought, since I’m not overly excited about the content yet, but the stock is interesting since it’s down from $700 to $189 as of tonight’s close. Frankly, I’d rather be a little late owning it, rather than trying to catch a bottom in a stock like that. That’s one opinion.

So often, readers are looking for a big call but that’s not the case here. I do think analysts are too nervous headed into Q2 ’22 earnings, but even if there is weakness in the forward estimates, has the -19% SP 500 return this year (as of Thursday night’s close) discounted that weakness ?

So many charts are scraping their 200-week moving averages when I went through Worden this week, it was kind of shocking. The industrial sector is expecting good EPS growth this year and yet several names, like Caterpiller, like Deere and Honeywell, haven’t escaped this selling.

These aren’t recommendations, just thoughts on the investing landscape.

The negative sentiment around the coming earnings season is really smothering. I’m looking for reasons to put some cash to work in the next few weeks, particularly around the FOMC meeting, July 27th, 2022 and the GDP report, which is scheduled to be released Thursday, July 28, 2022.

This isn’t 2008, by any stretch of the bearish imagination.

Traveling this weekend to see a client on the West Coast, back Sunday. Would like to publish another update before the end of the weekend.

Take all of the above, with a grain of salt. None of this is a prediction about the capital markets. Past performance is no guarantee or expectation of future results. Watch how stock prices react to good or bad earnings news. That’s key – a bad earnings report that results in a stock rising on heavier volume can possibly indicate a bottom is in for the stock. Price action matters more than sentiment.

Thanks for reading.