SP 500 data as of 7/8/22: (Data source: IBES data by Refinitiv’s This Week in Earnings):

- The “forward 4-quarter” estimate for the SP 500 has slide sequentially for the last two – three weeks falling to $240.83 from $241.70 two weeks ago;

- The PE ratio on the forward estimate is now 16x vs the 21x to start 2022;

- The SP 500 earnings yield is 6.18% versus last week’s 6.31%;

- What’s somewhat interesting is that the bottom-up quarterly EPS estimate of Q2 ’22 is $55.51 and has been firm since early May ’22.

![]()

The above data from IBES data by Refinitiv, shows the trend in both 2022 and 2023 quarterly bottom up estimates, from early April ’22. The latest week is as of July 8 ’22.

The bordered areas are the quarters which comprise the current “forward 4-quarter” estimate for the SP 500. Don’t confuse the annual SP 500 EPS estimates with forward 4-quarter estimates, which readers often do.

The “rate-of-change” in forward estimates:

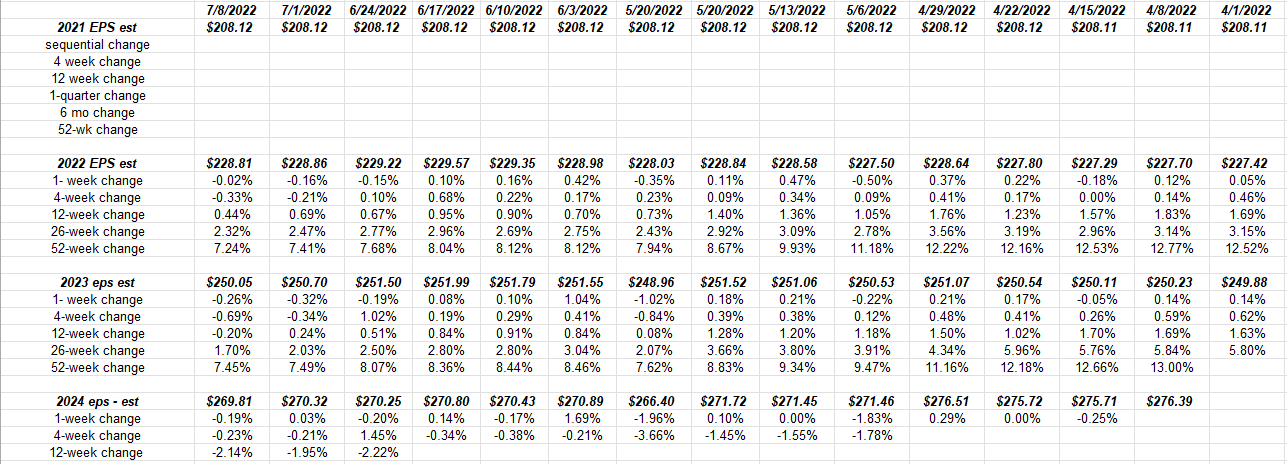

From the IBES data by Refinitiv, this spreadsheet calculates “rate of change” in the forward estimates.

Readers can see the 2022 rates of change are slowing, with some of this expected due to the improvement in 2021 EPS actuals which make for tough compares in 2022.

Note how 2023 SP 500 estimates are stable around $250 in EPS, while 2024’s estimate is has fallen from expected 10% EPS growth to 8% today.

However, it’s premature to make bets on 2024, and even 2023 until we see Q2 ’22.

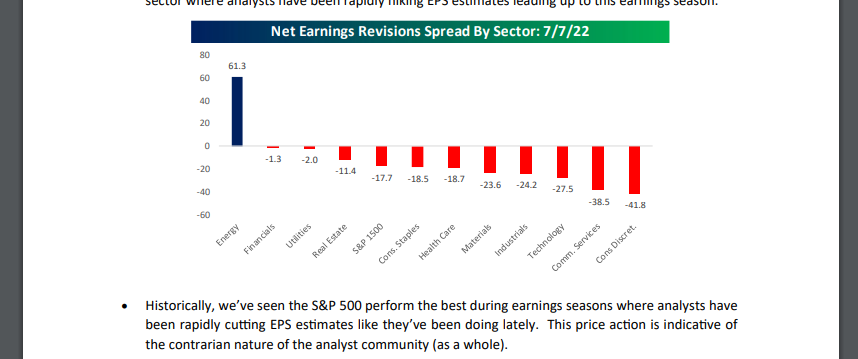

Revisions by sector:

Here’s an important bar chart from this weekend’s Bespoke Report. Note the strength in energy and the weakness in the other 10 sectors. While the revisions could continue into Q3 ’22, the “compares” for these sectors particularly for financials and technology, get easier as readers and investors move through the back half of this year.

Bespoke noted an excellent point in that bottom bullet point: typically when analysts have been this bearish heading into an earnings season, the stocks tend to perform (price action post earnings release) much better than the sentiment would indicate.

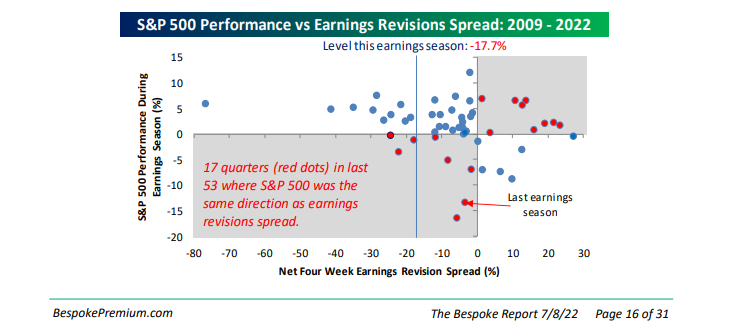

Here’s a better table and note from Bespoke:

As the red typing indicates Bespoke notes that of the last 53 quarters, 17 of the quarters saw the SP 500 move in the same direction as earnings revisions.

Rather than guess, let’s wait and see what the data looks like versus the stock price reaction.

Companies reporting this coming week:

- PepsiCo (PEP) (Monday, 7/11 after the close)

- Delta Air Lines (DAL) Wednesday, 7/13 pre-open)

- JP Morgan (JPM) Thursday, 7/14, pre-open)

- Morgan Stanley (MS) Thursday 7/14, pre-open)

- BlackRock: (BLK) Friday, 7/15 pre-open)

- Citigroup: (C) (Friday, 7/15 pre-open)

- Wells Fargo: (WFC) Friday, 7/15 pre-open)

Source: Briefing.com

While the strongest interest is in the financial stocks like JPM, MS, and C, I’ll be reading PEP’s press release to see what impact currency had, while Delta Air’s press release will be read for a read into jet fuel and what Delta’s forecast is for both revenue guidance and jet fuel cost. The airline stocks, which have never been owned in any size in the last 20 years – with the occasional trade made in JETS – peaked in early ’21 on the reopening and rebound in biz travel trade – but have been selling off ever since. As a big fan of Southwest Airlines (LUV), I don’t fly the others.

This article from June 23rd talks about the tough compares that the big banks and brokers face in Q2 ’22, but also makes a case for the attractive valuations in the sector.

Analysis / conclusion: The general bearish sentiment around the stock and bond markets as a whole, and the Bespoke data noted above, have left me feeling more positive about Q2 ’22 earnings as we start the reporting period BUT, that doesn’t mean every sector will perform well. In particular, the energy sector should have exceptionally strong EPS growth and cash-flow growth and even revenue growth when energy companies start reporting earnings in the next few weeks (most energy companies report around the last week of April, July, October, etc.) so how the price action compares to the results will be interesting. Energy faces very tough compares over the next 4 quarters AND crude oil hasn’t traded above it’s March ’22 $131 spike high.

Financial stocks feel just the opposite to me, particularly big banks and the brokers. JPM is down 26% YTD, versus the SP 500’s -17.5% return as of July 8 ’22, so any fresh money will likely see JPM bought down here, at least a small position, after falling from $170 to $114. Citi (C) is down 21% YTD. Morgan Stanley (MS) is also down 21% YTD, but it’s not owned yet. Some clients have a small position in Citi (C).

The strong dollar and tough compares for the tech sector will likely see tough earnings reports when Apple, Amazon, Alphabet, Meta, and Microsoft report later in July ’22. That’s still a lot of market cap between those 5 companies (21% of the SPY market cap as of 7/8/22).

Oracle and Cisco have big dollar sensitivities and thus the recent continued strength in the dollar could be an issue, but these companies don’t report again until August (CSCO) and September (ORCL).

While not shown the improvement in some of the charts (technical analysis) for the Nasdaq 100 and the mega-cap stocks is encouraging. The SP 500 hasn’t made a new low since mid-June ’22. When companies report this week, and next (and more will be published prior), note if price action moves inversely to prevailing sentiment around the companies / stocks coming into earnings. That can be a very good tell.

CPI data is due out Wednesday, 7/13/22, while PPI data is due out Thursday. Continued moderation in core CPI and PPI components would be a positive. This blog will have another post out prior, but the headline (overall) numbers are still expected to be elevated.

Lots happening this coming week. Take all this written here today with healthy skepticism. Writing this out every week, helps me prepare for economic and earnings data, and gives me a good idea of what the sentiment, technicals and fundamentals are for coming data.

Personally, I’m feeling better about the pending earnings season than a week or two ago. A reader noted Ed Yardeni cut his 2022 SP 500 EPS forecast to $215 versus the expected estimate of $228 and change, which is a 5% – 6% reduction in 2022’s full-year EPS estimate with the SP 500 being down as of Friday, about 17.5%. Is that reduction already in the market ? Possibly.

As always, thanks for reading.