The regular earnings update will be out Sunday, July 10th.

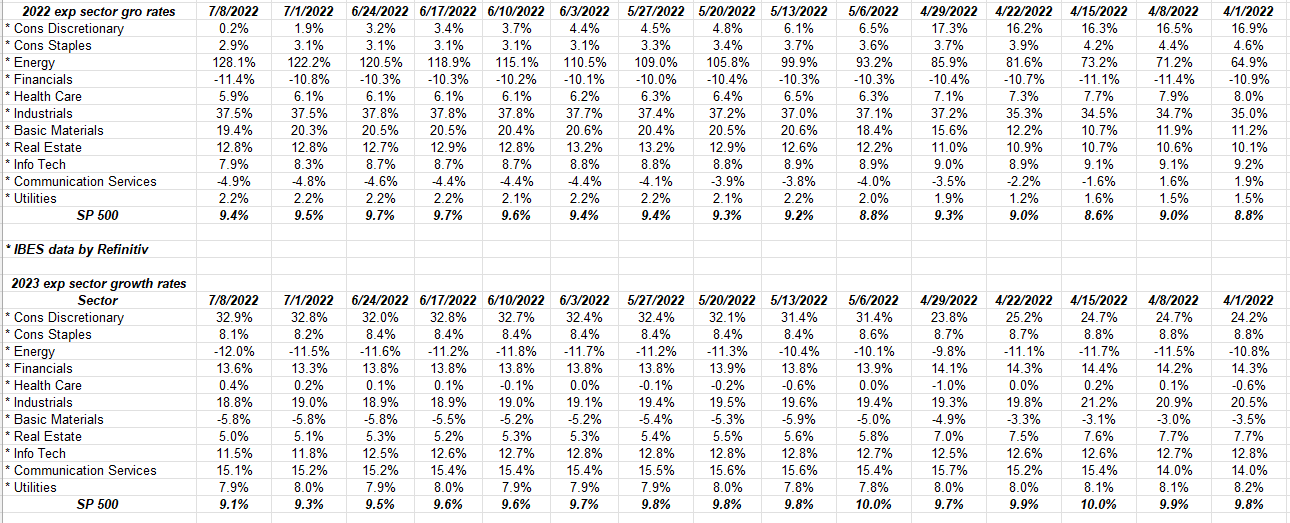

Let’s look at how expected Q2 ’22 revenue by sector has changed since April 29 ’22: (data source is Refinitiv’s This Week in Earnings tables):

- Consumer Discretionary: +12.8% expected 4/29/22, vs the expected revenue growth rate of +15.4% as of 7/8/22;

- Consumer Staples: +3.9% expected 4/29/22 vs the +5.1% expected revenue growth rate as of 7/8/22;

- Energy: +37.5% expected 4/29/22 vs the expected revenue growth rate of +47.1 as of 7/8/22;

- Financials: -3.1% expected as of 4/9/22, vs the +2% expected revenue growth as of 7/8/22;

- Health Care: +7.2% expected as of 4/29/22 vs the +4.4% revenue growth expected as of 7/8/22;

- Industrials: +12.4% expected as of 4/29/22 vs the +14.3% expected revenue growth as of 7/8/22;

- Basic Materials: +14.1 expected as of 4/29/22, vs the +9.5% expected revenue growth as of 7/8/22;

- Real Estate: +13.7% expected as of 4/29/22, vs the +13.8% expected revenue growth as of 7/8/22;

- Technology: +8.8% expected as of 4/29/22 vs the +8.9% expected revenue growth as of 7/8/22;

- Comm Services: +4.3% expected as of 4/29/22 vs the +5.5% expected revenue growth as of 7/8/22;

- Utilities: -1.2% expected as of 4/29/22, vs the +3.9% expected revenue growth as of 7/8/22;

What’s interesting about this data and the change is that Basic Materials, one of the strongest sectors this year thanks to the commodity concentration, is the only sector showing an expected revenue growth rate that’s lower on 7/8/22 vs 4/29/22.

10 of the 11 sectors are expecting higher Q2 ’22 revenue as of 7/8/22 vs 4/29/22.

Energy revenue is obviously higher, but the EPS leverage is what matters there.

The industrial sector has the 3rd highest expected revenue growth of the 11 sector within the SP 500 at 14.3%, behind energy and consumer discretionary and yet it gets little devotion from the financial media.

Look how strong relatively the industrial sector EPS growth looks versus the SP 500 in both 2022 and 2023.

The energy sector faces very tough comp’s in the back half of 2022, with Q3 ’21 showing the energy sector grew EPS and revenue 243% and 117% respectively, while Q4 ’21 shows 97% y.y revenue growth. (The EPS growth in q4 ’21 is 1100% or something ridiculous, which is the exact problem using percentages versus actual EPS.)

Summary / conclusion: none of this is a recommendation to buy or sell and and really it should just provide readers with some perspective before we look at the regular SP 500 earnings update on Sunday. Many sell-side analysts are nervous and some of the SP 500 EPS data has been seeing slight erosion prior to some of the big banks and brokers and money managers reporting next week.

Today’s June jobs report might give some investors peace of mind that investors won’t see wholesale downward revisions in SP 500 EPS. However it’s best to see the actual earnings releases and guidance first.

More coming on Sunday. Thanks for reading.