The 60/40 benchmark portfolio was down -14.64% YTD as of Friday, June 24th, 2022, with the SPY being down -17.26% YTD and the Barclay’s AGG being down -10.71%.

The energy sector has been absolutely pummeled the last few weeks and crude oil has still yet to trade above the early March ’22 spike high of $131, but the 6.62% bounce in the SPY per the Morningstar return data, indicates that bearish sentiment became way too one-sided the week of June 17th, 2022.

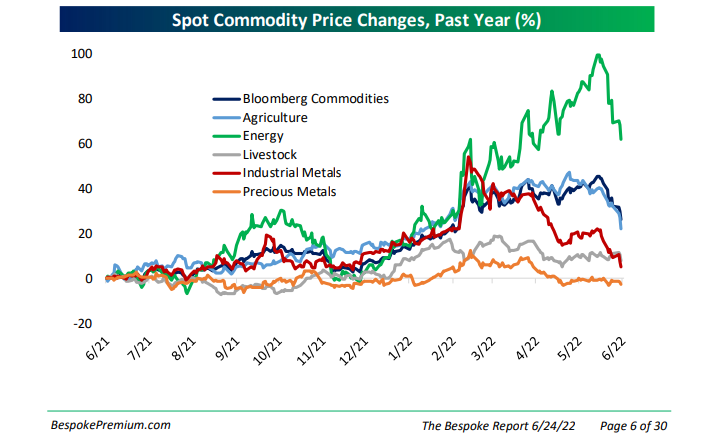

Commodities have also started trading off hard: Ed Yardeni has noted the decline in copper while Gary Morrow (@garysmorrow) write about soybeans (SOYB) and their technical deterioration late last week. What’s interesting about the grains is that Ukraine was supposed to cause a plethora of issues around wheat and the grain complex leading to sustained food inflation, but according to this chart by Bespoke from the Bespoke Report of June 24 ’22, that argument is unraveling quickly:

To be fair to Bespoke, their point of view is that the weakness across all these segments is that the “markets expect demand to weaken materially” which is not a positive for SP 500 earnings and likely means a recession is looming.

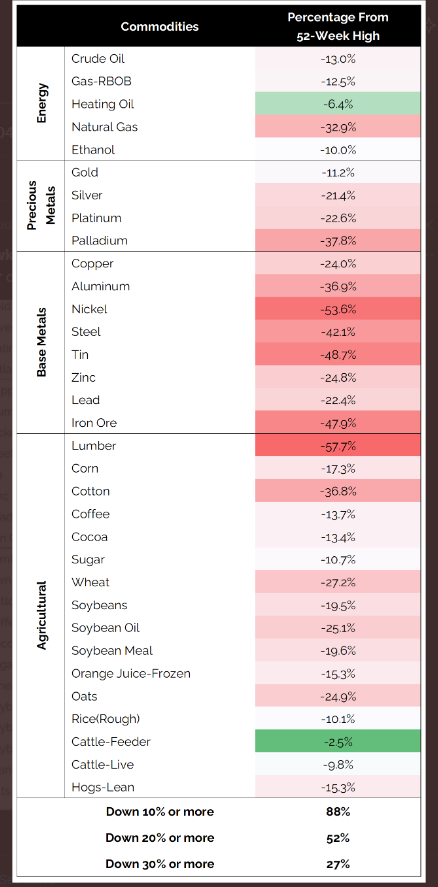

This table from @granthawkridge really got my attention:

One argument says that the fact that the SP 500 closed this week above 3,810 is the recovery of the first key technical level for the benchmark that indicates that perhaps the worst has passed and the equity markets are healing. The next two key levels are the March ’22 lows of 4,157 and 4,161: once those levels are surpassed by the SP 500, investors can begin to think about playing more offense than defense in today’s markets.

Most investors are in the camp that the SP 500 rally this week is just another oversold bounce, like we saw in late March ’22 (about an 11.5% rally for the SP 500 off the March ’22 lows) that eventually rolls over.

SP 500 earnings data:

- The forward 4-quarter estimate slipped a little this week, falling to $235.68 from $236.06;

- With the 6% rally in the Sp 500 this week, the PE jumped to 16.6x versus the 15.5x last week;

- The SP 500 earnings yield fell to 6.06% from 6.42%;

What might be interesting for readers is that – if we assume that we’re already in July ’22 as we will be next Friday, July 1 ’22, the forward 4-quarter estimate will be from Q3 ’22 to Q2 ’23, and that current forward estimate is now $241.70.

So just the simple “calendar roll” every quarter sees a higher forward 4-quarter estimate.

Remember, this changes every week. This post this week is an early look at the typical “quarterly bump” in the SP 500 forward estimate.

Summary / conclusion: The drop in the price of crude oil and the hammering of the energy sector not to mention the accompanying drop in the other commodity groups could be one of two things: a.) sharp correction in an ongoing bull market in energy or commodities, or b.) the beginning of the unraveling in commodities and the energy trade that indicates to many a recession is inevitable.

The question really then is, if b), does the Fed and start to consider that the “neutral” fed funds rate is less than what they are considering currently or they can slow the rate of fed funds rate hikes to get fed funds back to a neutral position ?

If we see a fed funds rate hike of 75 bp’s in late July ’22, and the SP 500 does NOT make a new low, below the June ’22 lows, that’s an important tell as well.

There is a growing and almost uniform belief that the US is headed into a recession. There is also a growing belief that negative preannouncements will start almost as soon as the 3rd quarter begins on July 1 ’22. The jobless claims data is elevated from it’s March ’22 lows near 166,000, but seems to have leveled off – at least temporarily – near 230,000.

Personally, I’m in the middle. The sharp drop in all commodities is worrisome if it’s demand-driven. There is still not much change in forward EPS estimates so it’s tough to get too negative. The SP 500 estimates are looking for 10% growth in full-year 2022 as of this weekend, up from 8% to start the year, so that’s keeping me somewhat optimistic, as is the fact that the last recession was the worst since the Great Depression, so “recency bias” has everyone assuming the next recession will be as bad as the last. (I don’t think of 2020 as a recession, or the start of a new bull market.)

We had 2 years – 2020 and 2021 – where there were gross distortions in the US economy and the financial system, and finally – beginning with the 2nd half of 2022, we will begin to see things “normalize”. Q2 ’22 earnings will be a very tough compare with Q2 ’21, which get easier going forward in 2022 (the compares that is).

The US economy will feel slower going forward only because we will be in a more normal operating environment.

Take all this with deep skepticism. It’s just one opinion. Writing it out every weekend helps the investment process. To hedge a deeper recession as so many think is coming, you can own long-dated Treasuries and the AGG, but you have to get the inflation picture right too. It’s a more complex investment world in 2022. Credit risk finally has some yield, but you don’t want to be long or overweight credit going into a recession. High yield corporate and muni’s actually look great again, if the US avoids a recession, but naturally that’s a big “if”.

The record lows in sentiment – really unprecedented in some cases – is probably keeping me more positive than would otherwise be the case.

Thanks for reading.