Ed Yardeni has named the mega-cap companies that dominate the SP 500 index, the “Mega-cap 8”. This week we hear from Alphabet (GOOG/GOOGL) on Tuesday, February 1, Facebook (FB) on Wednesday, February 2, 2022. (Technically, Facebook’s new corporate name is “Meta Platforms” but that’s like calling Ron Artest, the NBA badboy, “Metta World Peace” after his name change, but I’m too lazy to spell all that out, even though this just did). Amazon (AMZN) reports their Q4 ’21 on Thursday, February 3rd, 2022. Unlike the 2nd and 3rd quarters, the mega-cap technology companies are being split over two weeks rather than all the reports the last week of July and October of ’21, so investors have a better chance of digesting the fundamentals and the guidance. Merck (MRK) is also scheduled to report Wednesday night, February 2nd, after the closing bell. This blog will cover the Merck numbers too.

Alphabet (GOOG/GOOGL); $1.77 trillion market cap; Market cap weight in SP 500 is 4.11% as of 1/28/22, ranking 4th in the top 10 SP 500 holdings;

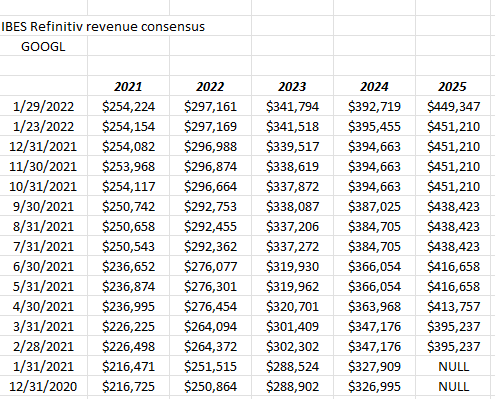

Alphabet reports after the closing bell on Tuesday, February 1, 2022, with analyst consensus per the IBES data expecting $27.32 in EPS on $72.1 billion in revenue for expected y.y growth of 23% and 27% respectively. (Clients are only long GOOGL and that’s the ticker that will be used here.)

Last year, Q4 ’20 GOOGL reported a 40% upside surprise in EPS and 8% in revenue. Last quarter, Q3 ’21, GOOGL reported a 20% upside in EPS on a 3% upside in revenue. What’s worse, in Q1 ’21, GOOGL reported a 68% EPS upside surprise on a 8% revenue upside, so the compares are pretty tough for Q4 ’21 and Q1 ’22.

The current 2022 full-year EPS estimate is $122.06 and is only looking for 3% EPS upside this year, on an expected $297 billion in revenue or 17% calendar year revenue growth. It’s unusual to see GOOGL consensus only looking for 3% EPS growth in a calendar year when the last 11 years saw GOOGL average 18% EPS growth per year from 2010 to 2020. If the consensus EPS estimate is met for Q4 ’21, GOOGLE will have grown EPS a whopping 85% in 2021.

The worries coming into Q3 ’21 were on the advertising side and a slowdown was expected but you’d have to think a material slowdown would be needed for GOOGL to only grow EPS 3% in calendar 2022.

Valuation: with GOOGL trading 10% lower than when it reported Q3 ’21, the stock is trading at 24x and 21x current consensus for 2022 and 2023 and about 20x and 28x cash and free-cash-flow ex-cash. GOOGL’s free-cash-flow yield is 3% – 4% coming into the earnings release. Even if GOOGL grows just 10% – 12% in 2022, the multiple today look appropriate.

YouTube and Google Cloud have been the drivers as search maintains it’s market share, although Google Search is now less than 60% of total Google revenue. In the June ’21 quarter YouTube advertising grew 84% y.y. (Didn’t see what the growth was last quarter. Assume tough comp’s into ’22.)

GOOGL had a $142 bl in cash on the balance sheet as of 9/30/21. Hard to believe if growth stocks struggle with higher interest rates, Ruth Porat, GOOGL’s CFO, won’t put more of that cash to work.

EPS estimate revisions:

Revenue revisions:

Meta Platforms (FB): $839 bl market cap, and FB’s market cap weight in the SP 500 is 1.90% as of 1/28/2022, ranking 5th in the top 10 SP 500 holdings;

When covering the Q3 ’21 quarterly previews for big-cap tech, FB looked ok. Unfortunately, clients are out of the stock almost entirely. Facebook is less than 20 years old (Mark Zuckerberg created “thefacebook” in 2004) and already the business model has gone from social media to metaverse, which is an extraordinarily short period of time to transition from start-up, to hyper-growth, to maturity, if we can call it that. The political football that Facebook has become has attracted regulatory attention – that’s never good, and it’s unfortunate.

Consensus estimates for Q4 ’21 are expecting $3.84 in EPS on $33.4 billion in revenue for expected y/y growth of -1% and 27% respectively. Again, Q4 ’20 and Q1 ’21 are tough compares with FB printing 52% EPS and 25% revenue growth in Q4 ’20, and 93% and 50% (EPS and revenue growth respectively) in Q1 ’21.

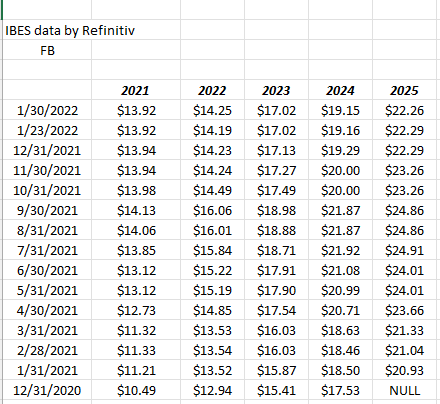

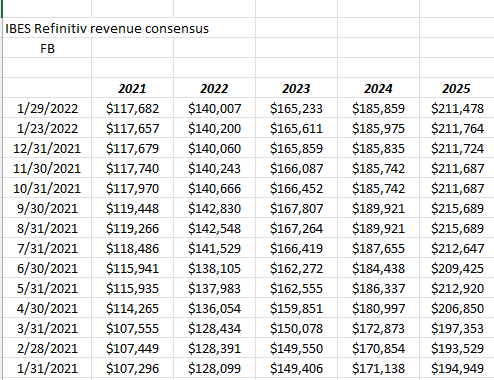

Full-year calendar 2022 is expecting $14.25 and $140 bl for expected growth rates of 2% and 19% respectively.

Like GOOGL, FB is expecting a lean year in 2022 EPS growth, possibly advertising driven.

Valuation: trading at 21x and 18X 2022 and 2023 expected EPS for 2% and 19% EPS growth, FB’s multiple looks rich, but – like GOOGL – I wouldn’t expect FB to print just 2% EPS growth in 2022. Cash-flow multiples are 16x and 24x ex-cash respectively, with a 4% – 5% free-cash-flow yield.

EPS estimate revisions:

Revenue revisions:

The revisions are positive and higher for EPS and revenue. That’s a plus for FB.

Summary: The way FB is having to pivot to the metaverse is unfortunate, given all the negative press it received, and then regulatory attention, but the core business is still there and generating much of the current growth. Like the electric vehicle, secular changes to business models happen gradually, then suddenly, and you’d have to think the metaverse is a long way away. It’s the least favorite of the mega-cap 8 tech names. It’s going to be a few years of transitioning a business model that isn’t all that old to begin with. The revenue and EPS estimate revisions are positive.

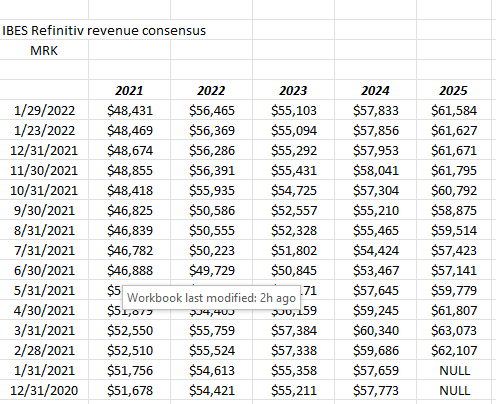

Merck (MRK): $204 bl mkt cap, with no idea of MRK’s market cap rank in the SP 500;

The dynamic around MRK is totally different than mega-cap tech as MRK hasn’t made a new all-time-high in 20 years, peaking in the year 2000 around the large-cap pharma growth phase. Hence the stock has been on the radar screen and has been slowly accumulated for client accounts over the last few years.

Q4 ’21 consensus estimates are looking for $1.52 on $13.1 billion in revenue for expected y.y growth of 15% and 5% respectively. If the Q4 ’21 estimates are met MRK will have grown EPS and revenue -2% and 1% respectively in calendar 2021. The pharma giant was hurt the last two years by the slowdown in elective surgeries.

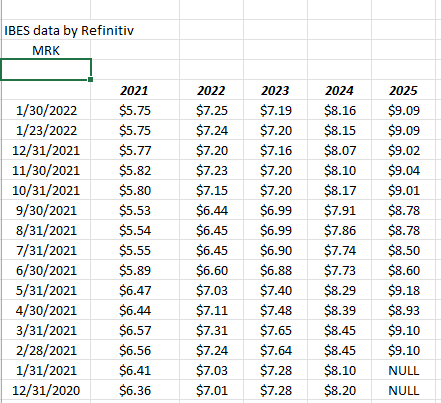

For MRK, 2022 consensus is expecting $7.25 in EPS on $56.5 billion in revenue for expected y.y growth of 26% and 17% respectively. MRK’s expected 2022 growth rates are exactly the opposite of mega-cap tech, at least that’s what’s expected for 2022.

Valuation: Merck sports a 3.5% dividend yield and an 11x multiple for the expected 26% EPS growth in 2022 which is very attractive. The cash-flow and free-cash-flow multiples of 18x and 35x look more like appropriate PE multiples. MRK has a free-cash-flow yield of 3%.

Summary: Keytruda is still the big drug for MRK, along with Januvia (although some slowing of Januvia revenue is expected in 2022) but all this has been lost amidst the Covid drug development. Merck shot higher in mid-October ’21 on news of a Covid pill and it’s potential for EU acceptance and then dropped back down to $70 on news that Mr. Buffett sold his entire position, and the Build Back Better bill was going to allow for Medicare to negotiate drug pricing for the most expensive drugs. There was also news that Pfizer has the one-up on MRK on EU Covid pill purchases. If Merck traded above $85 – $88 on good volume and positive EPS / revenue revisions, the stock will have broken out of a 20-year range, much like Pfizer recently did.

EPS estimate revisions

Revenue revisions:

One aspect of the data caught my eye: both the EPS and revenue estimates revisions are tracking higher for 2022.

This could be a big earnings report for Merck.

Amazon (AMZN): $1.5 trillion mkt cap and #3 market cap rank in the SP 500;

Amazon reports after the closing bell Thursday night, February 3, 2022.

Analyst consensus is expecting (per IBES data), $3.17 in EPS on $137.6 billion in revenue for expected y.y decline in EPS of 79% on +10% expected revenue growth. (The valuation spreadsheet on Amazon goes all the way back Q1 ’10 and I cant find another quarter where AMZN printed +10% y.y revenue growth. Some 15% quarters, but nothing that low in 10 – 11 years. )

Coming into the Q3 ’21 call, operating income guidance was roughly $4 to $7 billion, but was greatly reduced on the Q3 ’21 conference call to $0 to $3 billion or a reduction of more than 50%. Amazon has a history of guiding poorly in the sense that they typically lower expectations and then beat that guidance dramatically. However, Covid, supply chain logistics, labor problems at FedEx and UPS (not to mention Amazon itself) have really lowered expectations.

After Q1 ’22, the compares get easier for the megacap 8, particularly Amazon.

From 2003 to 2021, Amazon had only one year of revenue growth below 20% that was 19% in 2014. Presently, coming into the 4th quarter call, Amazon is expecting 18% revenue growth in calendar ’22 on expected 23% EPS growth. That’s still pretty low for the ecommerce giant, but it’s also a function of the post-Covid world.

Here’s another data set that caught the eye:

- Q4 ’21 EPS – est: $3.71

- Q3 ’21 EPS – actual: $6.12 (31% downside surprise or miss)

- Q2 ’21 EPS – actual: $15.12 (23% upside surprise)

- Q1 ’21 EPS – actual: $15.79 (65% upside surprise)

- Q4 ’20 EPS – actual: $17.26 (39% upside surprise)

- Q3 ’20 EPS – actual: $12.37 (68% upside surprise)

- Q2 ’20 EPS – actual: $10.89 vs $1.50 estimate

- Q1 ’20 EPS – actual: $5.01 (20% downside surprise or miss)

All we’ve done is “round-trip” the Covid bowling ball through the snake in 2020 and now we’re seeing the downside of that. Again like GOOGL and FB, Amazon’s Q1 ’21 presents a formidable compare for Q1 ’22.

EPS revisions:

Revenue revisions:

Have to say, the downward pressure on Amazon EPS and revenue estimates is not good, particularly for a company with a 60x – 70x multiple expecting 23% EPS growth next year.

Amazon’s capex has soared to $67 billion (TTM) versus the $18 – $19 billion as of the end of 2019. Any time Amazon has gone through an “investment period” like this it has yielded substantial revenue growth. Amazon’s “average” revenue growth since 2002 is 29% per year.

That’s going to be hard to maintain.

Sentiment remains very bullish around Amazon and the expected stock performance. That’s worrisome too.

Summary / conclusion: Looking at the above 4 names previewed today, most likely wouldn’t pick Merck as their top stock. All of the above stocks could have good quarters, but “growth” has outperformed too long. Growth stocks could trade sideways for a few years as multiples compress and PE’s expand on long out of favor sectors. That’s not saying this will happen, but it has happened before.

Thanks for reading.

Expected ’22 revenue growth:

- Facebook +19%

- Amazon +18%

- GOOGL +17%

- Merck +17%

Expected ’22 EPS growth:

- Merck +26% EPS growth

- Amazon +23% EPS growth

- GOOGL +3% EPS growth

- Facebook +2% EPS growth

Expected ’22 multiple:

- Amazon: 58x

- GOOGL: 24x

- FB: 21x

- Merck: 11x

Free-cash-flow yield:

- FB: 4%

- GOOGL: 3%

- MRK: 3%

- Amazon: 0%