The familiar litany heard from clients in the late 1990’s and lately today when the subject of trimming winners arises, particularly the Megacap 8 (as Ed Yardeni refers to the top market cap weights in the SP 500) is that “they’ll come back, I’m not worried.”

Having recently had this conversation with a client with me warning that some longer-term portfolio winners will have to be reduced, a list was put together of growth stocks from the late 1990’s that took years to recover their all-time-highs (if at all):

- Microsoft (MSFT): peaked in January, 2000, and did not make a permanent all-time-high until July, 2016;

- Cisco (CSCO): peaked at $82 in April, 2000, and has yet to get back above that key price level;

- Intel (INTC): peaked at $73 in July, 2000, and has yet to make a new all-time-high in 21 years;

- Oracle (ORCL): peaked in September, 2000 at $46 and then didn’t make a new all-time-high until June, 2017;

- Pfizer (PFE): Peaked at $45 in June, 2000, (spinoff adjusted), and just broke out of that 20-year base in 2021;

- Merck (MRK): also peaked at $87.50 in December, 2000, (again, spinoff adjusted) and has yet to make an all-time-high.

- Walmart (WMT) peaked in January ’00 at $70.25 per share, and mever traded above that level until July, 2012;

- Home Depot (HD) peaked at $70 per share in April, 2000, and it too never made a permanent all-time-high until March, 2013, or just around the same time the SP 500 was making new all-time highs for the first time since March, 2000, and October, 2007.

- Bank of America (BAC) hasn’t made a new high since January, 2006 when it printed $55 per share and still looked reasonable on a valuation basis given it’s dividend yield, etc. ;

- Schwab (SCHW) made a new all-time-high in April, 1999 at $51 – $52 per share and never recovered that price until the last 18 months (on a permanent basis), so “Chuck” was under water from 1999 highs for 19 – 20 years.

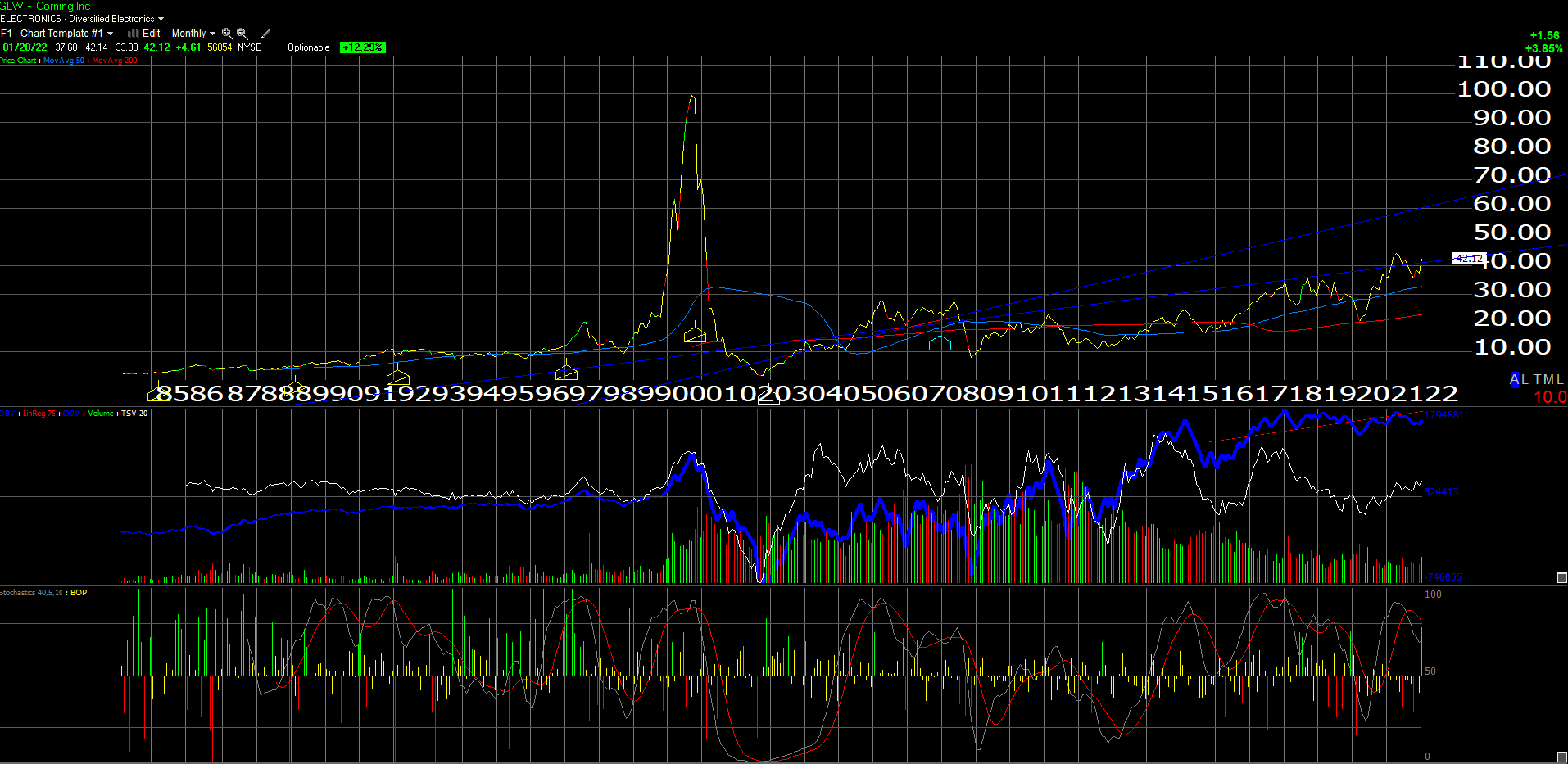

Think about a JDSU, whose chart can’t be found on Worden due to the 2015 split into two separate companies, or even Corning (GLW), whose monthly chart looks like this:

GLW had a good week this week, but the company has a heavy capex burden to bear much like Intel. GLW hasn’t been owned for clients since the early 2000’s. GLW since 1/1/2000 has returned less than 1% a year while the SP 500 has returned 7.4% for the last 21 years.

Summary / Conclusion: While there is a Captain Obvious element to this blog post for professional investors, it’s important for readers to understand and get when stocks are in the news like the “megacap 8” have been for the last 5 years and have had favorable “macro” conditions like very low interest rates and low corporate tax rates and pro-trade policies, conditions inevitably change, and multiples inevitably compress and buying near fevered all-time-highs can risk a considerable degree of client capital.

2022 is going to be a tougher year for growth stock investors, and client portfolios have been under transition for some time (since later in 2020) to spread the capital gains in taxable accounts. But admittedly, having been burned in 2000 – 2002, client portfolio’s have been managed with growth / value blend in mind, with a close eye on portfolio weights and correlations.

Today, 29% of the SP 500’s market cap is contained in the top 10 names in the SP 500 as of Friday, January 28, 2022.

While I personally have high regard for value investors like Oakmark Associates (David Herro and Bill Nygren), and other value investors like Vitaliy Katsenelson and Jim Chanos, it’s the – how shall I say – moral piety of the Jeremy Grantham’s who insist the last 12 years have been a bubble in the SP 500, during a period when the SP 500’s “average, annual return” since January 1, 2010 through 12/31/20 was over 15% per year.

Look, the decade from 2000 to 2009 was the worst decade of return for the SP 500 since the 1930’s. It was a pretty safe assumption, and it didn’t take a Rhodes Scholar to determine that the next decade (2000 to 2019) would likely see a better return for the SP 500, which it did. Even I got that right.

The power of both “PE expansion and contraction” can make growth and value investors look like complete idiots over long periods of time, while company fundamentals remain relatively sound. (Charlie Billelo, the excellent technician whose work is shown on YCharts and on Twitter with regularity, put up a chart of Microsoft’s revenue (in dollars) every year since the 1990’s last week, and Microsoft’s revenue grew in dollars every year from 2000 to 2015, yet Microsoft didn’t make a new all-time-high during that period. That’s a brutal market.)

To really wrap it up, this isn’t a screed for growth and against value investing or vice versa. Growth investors get it right and then can get it wrong, and value investors do the same. As someone who allocates capital for clients, I’ve become very partial to the great Bruce Lee’s fighting philosophy, i.e., “the best style is no style”.

This blog is reducing the growth stock weights, adding to select value names and sectors, and looking for “uncorrelated’ with the last 12 years.

Think for yourself, take everything you read here with a grain of salt, do your own homework, and past performance is no guarantee of future results.

Thank for reading.