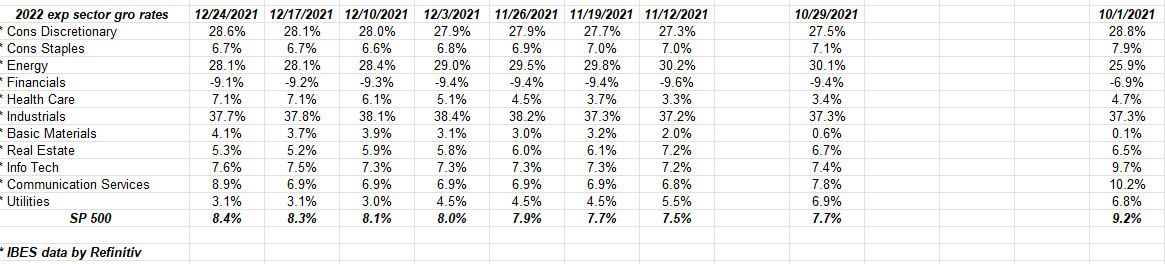

Looking at the above spreadsheet, this blog began tracking 2022 SP 500 sector earnings growth in early October ’21 since, with Q3 ’21 earnings, companies start to make their first pass at 2022 guidance, usually prompted by analyst questions. Most of the 2022 guidance will come in the January ‘ February ’22 period when companies release their Q4 ’21 earnings, but investors get a feel for the year ahead starting with Q3 ’21 results.

Note the “expected” sector earnings growth for ’22.

The Industrial sector – as of this weekend December 24, ’21 – is expected to lead the 11 SP 500 sector in terms of SP 500 EPS growth, and that’s after the sector put up almost 89% growth in 2021. If readers look at this blog post from December 17, 2021, readers can see how 2021 sector growth estimates looked one year ago and then the last 12 weeks.)

The point is estimates can change dramatically, both higher and lower.

The industrial sector, currently about 7% – 8% of the SP 500’s entire market cap, is thought to be economically-sensitive and thus readers have to factor in a Fed that is going to be withdrawing excess liquidity up until June ’22 and then outright tightening monetary policy after that period.

Here are the top 10 names by market-cap within the Industrial sector:

- 1.) United Parcel (UPS): $180 billion market cap;

UPS is expected to earn $12 in EPS on roughly $100 billion in revenue in calendar ’22 as they duke it out with Federal Express in the Ground business, which saw an enormous increase in demand in 2020 with the “staying at home” of mainstream America and then saw the decline in 2021 with the re-opening of America. FedEx (FDX) is the 18th largest stock in the Industrial sector market cap ranking, and just reported a decent quarter in Express, and slightly raised fiscal ’22 guidance. UPS is trading at roughly 18x ’22 EPS for expected ’21 EPS growth of 40% and 8% in ’22, and and just under 2x price-to-revenue for ’22. The onset of Covid in 2020 drove a whole new level of adoption of ecommerce in mainstream America, and UPS and FedEx are poised to benefit, and maintain market share. The risk is a cyclical slowdown and a tempering of ecommerce demand. From a longer-term perspective, it will be interesting to see what EV’s do for the “big brown truck” delivery system. UPS would benefit from a dramatic lowering of the cost of packages to household America. UPS has beaten the SP 500 this year returning 28.7% as of 12/23/21, right in line with the SP 500’s 26% YTD increase.

- 2.) Union Pacific (UNP): $156 billion market cap;

UNP is set to earn $11.37 on $23 billion in revenue according to the latest estimates from IBES data by Refinitiv, thus with the stock trading around $245 per share, the rail giant is trading at 21x next year’s expected EPS growth of 14%. Union Pacific lowered their volume and margin guidance for ’22 slightly in the October ’22 earnings call, although the stock is still trading close to an all-time high. UNP’s stock is up about 20% YTD trailing the SP 500 by about 600 – 700 bp’s.

- 3.) Honeywell Int’l (HON): $141 bl market cap;

Technically, HON is now getting oversold on a daily and weekly basis even though Q3 ’21 saw strong margin upside but it looks like supply chain issues have stalled the stock and have analysts looking at 2h ’22 recovery. The stock is down a -3% YTD in calendar 2021, so if readers are looking for a laggard for their portfolio, and don’t want to chase “mo”, do your homework on HON. What fascinates me about Honeywell, is wondering whether they will follow the path of GE and break up the company. Honeywell describes themselves as an aerospace, technology, and building products company. Morningstar recently raised their fair value estimate on HON to $225 from $211, which leaves the stock trading at a 10% discount to perceived “fair value”. Current estimates project HON earning $9 in EPS on $36.8 bl in revenue for expected y.y growth from ’21 of 13% in expected EPS.

- 4.) Raytheon Technologies (RTX): $123 bl market cap;

YTD Raytheon has returned 21.6%, versus the SP 500’s 27.6% as of Thursday, 12/23/21. Expected to earn $5 in EPS on $70.3 billion in revenue in calendar 2022, EPS is expected to grow 18% next year on 6% revenue growth. What’s interesting is that the stock is down from it’s October ’21 highs near $90, trading under it’s 200-day moving average and is getting oversold on the daily charts. Never having modeled or followed the company for any period of time, any additional commentary here might not be value-added.

- 5.) Boeing (BA): $113 bl market cap;

Looking for out-of-favor, longer-tail businesses, clients have seen Boeing added to accounts in the 2nd half of ’21 in smaller quantities. The aerospace manufacturing giant is still trading well off it’s early ’19 highs near $446 in January ’19. The chart is getting oversold on a weekly basis, which is typically a technical area where I try and take more interest. Does the manufacturing giant still have issues ? Absolutely, but new management and a healthy respect for the FAA with the core manufacturing business remaining intact makes the stock compelling from a 3-5 year perspective. Full-year 2022 consensus EPS and revenue estimates for BA are expecting $4.87 in EPS on $87.2 billion in revenue versus the EPS losses the last two years, and the onset of omicron and more pandemic worries and curtailed flights hurt the sentiment environment, but it’s only a matter of time before business travel improves. China is thought to be well behind their aircraft commitments even though the Chinese have approved the Boeing 737 Max as of early December ’21. Boeing is down 6% YTD versus the SP 500’s 27.6% and is down 14% since Jan 1 ’19 versus the SP 500’s 25% average, annual, return.

- 6.) Caterpillar (CAT): $109 bl market cap;

- 7.) Deere (DE): $107 bl market cap;

- 8.) MMM (MMM): $101 bl market cap;

- 9.) GE (GE): $100 bl market cap;

- 10.) Lockheed Martin (LMT): $95 bl market cap;

(Market caps are an approximation. They can change daily and sometimes materially with news flow and market action. The market cap ranking was provided by Refinitiv as of 12.20.21, so it is relatively current.)

Summary / conclusion: Looking at the top 5 stocks in the Industrial sector, and looking at their performance over the last 3 years or since January 1 ’19, only UPS has managed to beat the SP 500’s +23.25% average, annual return over that period. Ranking the returns by stock price, here is how the top 5 names fall out:

- UPS +32.7%

- SP 500 +24.5%

- UNP +23%

- HON +17.6%

- RTX +11%

- BA -14%

Time constraints prevented me from looking at all top 10 names in the industrial sector for readers.

Clients have been underweight the industrial sector some time, but with a shift towards defensive sectors and stocks, names like Boeing are much more interesting today. Clients are also long FedEx and the IYT, looking for a bounce in the long-suffering airline business, although the latest omicron spread might ultimately set the sector back again. Defense sector stocks can be attractive from a portfolio construction standpoint during economic slowdowns and when Republican’s have a majority in Congress.

From the 10,000 foot perspective, I also wonder if conglomerates won’t continue to struggle as it becomes harder and harder to generate decent returns on capex and investment in an era of low interest rates and incredibly-rapid ascendance and decline of business models.

When the return calculation is stretched back to 1/1/2015, or the start of the last half of the last decade, every one of the top 5 stocks listed above has underperformed the “average, annual” return of the SP 500 over the last 6 years. The next thought then is – to reward shareholders – I wonder if this group will eventually do what GE did and break up the conglomerate. GE had it’s own issues with the size of Ge Capital, and it was owned for clients until the stock traded below $20 on heavy volume long before it bottomed at $6 per share. Still, it’s a good example of what the future might hold for corporations trying to allocate resources across many different businesses.

Finally, just because the industrial sector shows the strongest “expected” SP 500 EPS growth for 2022 doesn’t mean that will materialize. A lot can happen next year to impact actual earnings. The death or rather what will likely be a substantially watered-down “Build-Back-Better” bill, has Morningstar rescinding their expectation of higher corporate tax rates for 2022, which is probably a good call. That might have been the catalyst for the rally this past week and may drive a healthy Santa Claus rally in the next 7 trading days.

Remember, take everything you read on this blog and elsewhere with considerable skepticism. Past performance is no guarantee of future results. These are my own thoughts and are not always actionable.

Thank you for reading.