A number of larger-cap banks and financials report this week. Here’s a quick summary of EPS / revenue estimates and valuation parameters for some of the financials owned and followed for clients:

If there is one theme to consider as we evaluate the financial sector’s results, it would be “keep an eye on the 2022 estimates”. (More on that later in the blog.)

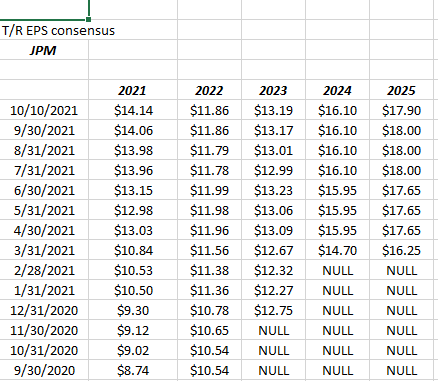

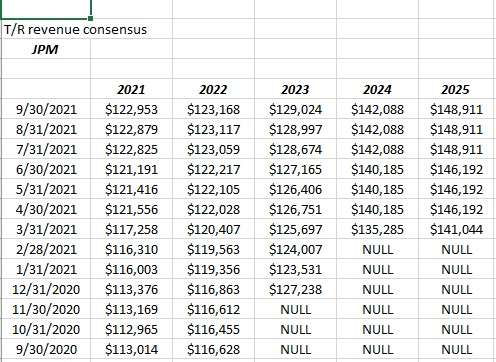

JP Morgan (JPM):

Source: IBES data by Refinitiv

JPM reports their Q3 ’21 financial results before the open on Wednesday morning, October 13th, 2021.

Current consensus for Q3 ’21 is expecting $3.00 in EPS and $29.79 billion in revenue for expected y/y growth of 3% and flat respectively. JPM’s revenue declined 8% y.y in Q2 ’21, while EPS rose 174%. What’s interesting is that the $3 in EPS and the $29.79 is higher than the original estimates for Q3 ’21 shortly after the July ’21 earnings report, so there has been a drift higher in the quarterly estimates.

JP Morgan is currently fully valued, trading at 2x tangible book at $170 per share, and a modest 2% dividend yield as well as 12x and 14x the 2021 and 2022 EPS estimates, although the positive revision trend (highlighted in the above spreadsheets) in JPM’s EPS and revenue estimates is very encouraging and thus with the continued healthy corporate credit markets and bond issuance, and low interest rates, all three of JPM’s segments i.e. consumer bank, commercial bank and capital markets are likely to see decent growth metrics.

What was interesting from the Q21 ’21 EPS release for JPM was that $0.75 of the EPS beat was “reserve-release” related (and this will likely shrink going forward) and management lowered net interest income (NII) on the July ’21 call, and yet we are still seeing improving revisions.

For calendar ’21, JPM is expected to grow EPS 59% this year, while revenue is expected to be up 2%. In calendar 2022, the current consensus is expected 0% revenue growth and a 16% decline in EPS, hence it’s worth watching the 2022 EPS and revenue revisions.

My own opinion is that Jamie Dimon has been one of the top 10 CEO’s in the SP 500 in the last 20 years. The stock’s valuation probably reflects that, As a contrarian example, owning Citgroup (C) since June 30, ’07 has only meant that – as an investor – you’ve only lost 89% of your investment since that date. (Yes, C is still down 89% from June 30 ’07 through Sept 30 ’21, per the Ycharts return calculator.)

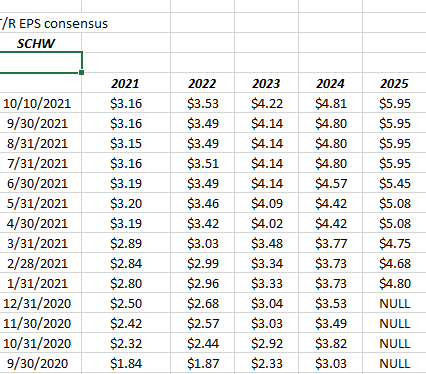

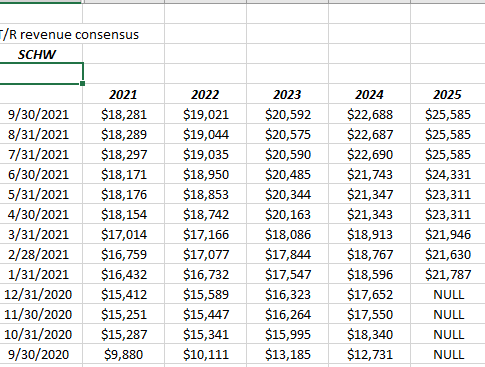

Charles Schwab (SCHW):

It’s interesting that the largest 3rd party custodian to the investment advisory business is always opaque about when their quarterly earnings reports will be released. Briefing.com has Schwab reporting Thursday or Friday morning before the opening bell (October 15th), with current consensus expecting $0.81 in EPS and $4.5 billion in revenue for expected y.y growth of 59% and 83% respectively. The issue with those numbers is that they are not “pro-forma” and include the closing of the TD Ameritrade merger which happened in October, 2020. Going forward, the y/y growth estimates should look more normal, since the AMTD metrics and numbers will be lapping the merger from a year prior.

For instance, looking at Q4 EPS and revenue estimates, the y.y growth is expected at 8% for EPS and 10% for revenue, more in line with historical estimates and both quarters will include TD Ameritrade.

Both EPS and revenue consensus courtesy of IBES data by Refinitiv

While Schwab (SCHW) is thought to be fully valued at $77 per share, 2021 calendar year EPS growth is expected to grow 30%, with the stock trading at 24x EPS. 2022 EPS growth is expected at 12% with the stock trading at 22x that forward estimate.

The TD Ameritrade merger is – in my opinion – an unambiguous positive, and you only need to look the trend in EPS estimate revisions, starting with the 9/30/20 and 10/31/20 estimates. Note the difference in the two months numbers and know that the merger closed in October ’20.

Just since 10/31/20, the 2021 and 2022 EPS estimates have increased 36% and 44% respectively over the last 12 months.

The other important tell is that the merger was expected to take 9 quarters to integrate: looking at expected Q4 ’21 growth of 4% in EPS and 10% in revenue that should tell investors that management hasn’t yet “levered” the expense integration which would be expected to show faster EPS growth given a sustainable level of revenue growth. In other words, and I’m guessing on this, Schwab has yet to fully realize all the integration “redundancies” of the merger and there is more growth in operating margin to come.

In q2 ’21, Schwab adjusted operating margin came in at 48.9% vs 46.3% (per Morningstar) and two quarters ago, Morningstar raised their long-run operation margin target on SCHW from 45% to 52%. That’s a definite positive.

It’s tough to add to Schwab here, but a pullback to the mid $60’s would be ideal. Schwab long ago threw off the “discount broker” moniker and is now firmly in the asset gathering camp. It’s “net new annualized” asset growth in Q2 ’21 was 6%. Like post-2008, the interest rate environment for Schwab is not favorable as the net interest margin continues to compress.

Schwab’s capital return policy is conservative to say the least. The dividend has been stuck at $0.18 per the quarter the last 7 quarters (understood given Covid) but with TD Ameritrade now nearing half way through the integration, it would be nice to hear about additional capital coming free and the plans for it. Schwab has never been a big share repurchaser, given it’s growth stock label.

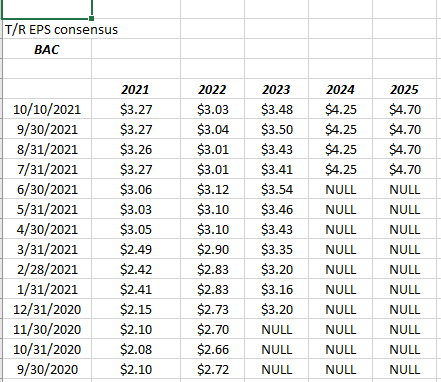

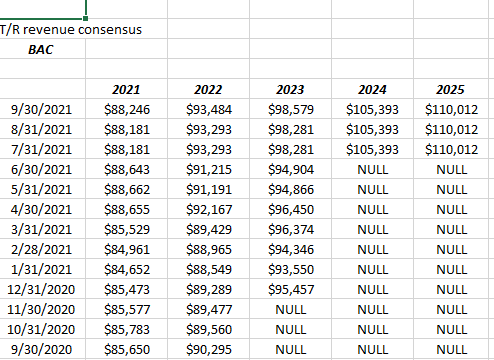

Bank of America: (BAC):

We don’t (yet) have a big position in BAC, but the stock is of interest since it’s still trading about $10 below its 2007 high near $55 per share.

BAC is expected to report their 3rd quarter, 2021 financial results Thursday morning before the opening bell.

Street consensus per IBES data by Refinitiv, is for BAC to report $0.71 in EPS on $21.7 billion in revenue for expected y.y growth of 39% and 7% respectively.

Revision trend:

Source: IBES data by Refinitiv

Much of 2021’s EPS growth for BAC is being driven by that reserve release given the size of BAC’s consumer business. Since 9/30/21, that 2021 EPS estimate has risen 56%, while the 2022 estimate has risen just 11%.

For calendar year 2021, BAC is expected to see 88% EPS growth on 3% revenue growth, while for calendar 2022 BAC is expecting 1% EPS growth on 6% revenue growth, so again, let’s watch the 2022 numbers and how they get revised after the Q3 ’21 earnings.

BAC recently raised the dividend from $0.18 to $0.21 per quarter. The share repurchase in the 2nd quarter was $4.2 billion and judging by one analyst model surveyed, the bank is expected to repo $5.5 billion each quarter for Q3 and Q4 ’21.

At $44 pet share BAC is trading over 2x tangible book of $21 per share, and is trading at 12x and 13x the current 2021 and 2022 EPS estimates, which expect 88% and 1% y.y growth respectively.

The stock is fully valued here at $44 per share but reserve releases will continue as credit losses continue to decline sharply as the job market remains very healthy and the unemployment rate fell to 4.8% on Friday, October 8th.

Financial sector expected 2021 EPS growth rate:

The above spreadsheet from IBES shows the financial sector as the highlighted row. Since early July ’21, the expected EPS growth rate for the financial sector for calendar 2021 as a whole has risen from 46% to 58%.

In terms of financial sector revenue trends, this post from last weekend, might shed some light on where financials stand relative to the rest of the SP 500.

Summary / conclusion: There are a whole slew of financials reporting this week and it’s impossible to cover them all, but the “macro” for the banks and capital return and improving credit losses, etc. certainly looks favorable 3 – 6 months out from here. Taper will actually benefit the banks, particularly if the yield curve should steepen, since it will widen or expand net interest margins (NIM).

The order of preference for readers is the order in which they are listed: JPM first, Schwab second and BAC third. A pullback of 10% for each would make for great entry points.

JP Morgan and Schwab have been top 10 holdings for clients for years.

Take everything you read with substantial skepticism. The numbers and revisions are still trending positive for many financial stocks, but the numbers can change quickly. None of this is advice, just how clients have been positioned or are being positioned so that readers can follow along.

Thanks for reading.