The question always is, “Where should investors put their money ?”

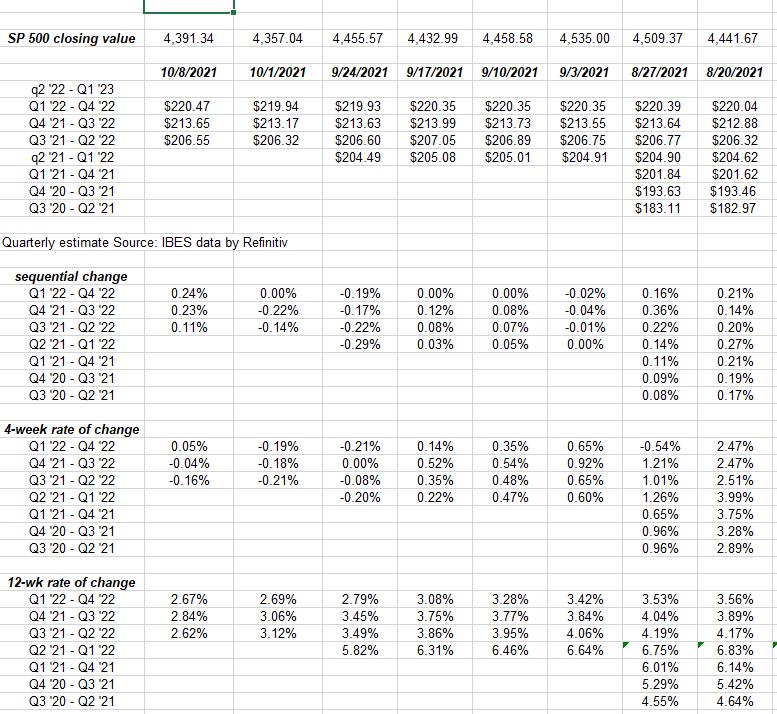

- One of last weekend’s blogs talked about the expected increase in the “forward 4-quarter” SP 500 EPS estimate and we were right on the money: the forward 4-quarter estimate this week was $213.65, up from last week’s print of $206 and change. Last week’s real forward 4-quarter estimate was $213.17 so this week’s estimate shows a return of the sequential increase in the key estimate.

- The PE ratio this week is 20.6 vs last week’s 20.4;

- The SP 500 earnings yield is 4.87% this week vs the 4.89% using the actual 4-quarter estimate last week. The PE ratio is now lower than most of August and September ’21, and the SP 500 earnings yield is now higher, hence the forward earnings estimate has risen faster than the SP 500. Trust me, that can reverse quickly.

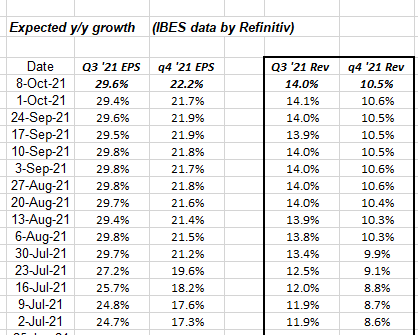

Trend in Q3 ’21 EPS and revenue growth rates:

All data is paid for through a subscription from IBES data by Refinitiv, but this blog repackages that data for readers.

With Q3 and Q4 SP 500 earnings results, readers will see a “return to normal” versus 2020’s Covid-impacted data and then the massive monetary and fiscal stimulus provided by the Fed and Congress.

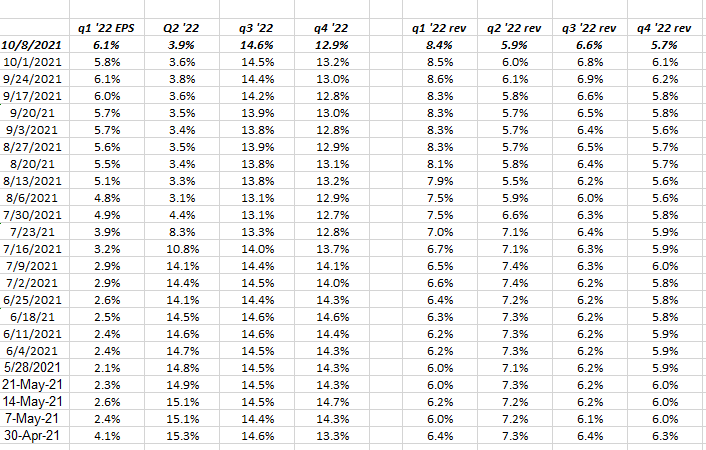

2022 will look like a much more “normal year” in terms of SP 500 y.y EPS and revenue growth rates:

Note how expected quarterly, 2022 expected EPS growth rates have turned higher again this week, while revenue turned lower.

We’ll know more with actual Q3 ’21 earnings results since analysts will ask corporate managements about 2022 on the Q3 quarterly calls. Management doesn’t have to answer, but some will.

Here is one note of caution: “rate-of-change”

Tracking forward estimates, and measuring their “rate of change” over longer time periods note the bottom batch of data shows the “12 week rate-of-change” starting to slow. This could reaccelerate with Q3 ’21 earnings reports but it bears watching.

Summary / conclusion: A number of pundits and bloggers have weighed in on Q3 ’21 earnings expectations and expressed caution over what might transpire, but – while this isn’t advice – the overall pessimism coming into the earnings season is actually a positive. Nick Colas over at Datatrek, Cam Hui over at Humble Student of the Markets, and even Josh Brown talked about Q3 ’21 earnings season on one of his always-worth-watching CNBC appearances near the close of the market every day, but the data is not yet flashing red (or really even yellow) thus far.

The stable-to-upward revisions in forward SP 500 EPS and revenue growth rates is a positive and a characteristic that I’ve put a premium on historically. The typical trend from the start to the end of the quarter (before seeing that quarter’s earnings results) is that the estimates tend to start higher and then get revised down slowly over the 90 days and then we see the actual results, with a typical 3% – 5% upside surprise for quarterly EPS.

The upside surprises for SP 500 EPS since Q2 ’20 have been monstrous. It tells you plenty about analyst’s models. Expect a more modest “upside surprise” for Q3 ’20.

The current bottom-up SP 500 EPS estimate for Q3 ’21 is $48.96. Even if we get a modest post-Covid upside surprise of 10% for the quarter (and we’ll know by the end of October whether this is feasible), that will put the Q3 ’21 estimate above the Q2 ’21 final bottom-up EPS estimate of $52.58.

The Q4 ’21 bottom-up EPS estimate of $51.25 has been relatively stable since mid-August when the worries over Q3 ’21 earnings started.

Clients biggest sector overweights are technology, financials and healthcare at present (which has been the case for some time) and that won’t likely change immediately. Readers should also be aware that energy, basic materials, real estate and utilities are each around 3% of the SP 500 by market cap summing to a 12% market cap weight, while technology, consumer discretionary and communication services are a combined 51% of the SP 500’s total market cap as of this week.

It’s just a personal opinion but I’m wary of energy and basic materials at this point given the run the sectors have had. Watch how the stocks react to what should be very positive earnings reports for energy and commodities.

More to come this weekend on the financials set to report this week.

October is the Wounded Warrior Project’s “300 Mile Bike Challenge” and I’ve readily accepted that challenge, doing 35 miles today and scheduled to do another 50 on Saturday, so if you don’t see any more blog posts this weekend, you should probably assume I went off a bridge somewhere in Western Illinois and have yet to be found.

Total miles ridden after tomorrow should be 187, with three weeks left to ride.

Take all opinions with great skepticism. This blog is not advice but should give readers a good feel for what the trends are within SP 500 earnings.

Thanks for reading.