As a regular blogger, I try not to be hyperbolic in terms of the market or earnings, but the forward estimate increases I’m looking at this week are nothing short of – well, remarkable – for the numbers and the increases.

It’s hard to know where to start.

Here is a quick rundown of what I’m looking at on the SP 500 earnings spreadsheet updated every week, which incorporates this week’s data as of Thursday, July 29, 2021:

- The “expected” SP 500 EPS growth rate this calendar year is now 44%, versus the “expected” 26% on April 2, 2021 and 23% on December 31 ’20;

- The “forward 4-quarter” estimate jumped to $204.70 this week from last week’s $201.27 and $159.02 as of 12/31/20;

- The PE ratio is now 22x, about where the PE has been all year;

- SP 500 earnings yield: closed at it’s high for 2021 at 4.66%, versus 4.56% last week and 4.23$ on 12/31/20. This is huge – investors are seeing a little PE compression in the SP 500 with big EPS and revenue increases for Microsoft and Google and such and yet the SP 500 was down -0.42% for the week. The SP 500 earnings yield hit 7% the week of December, 2018, after it corrected 20% in Q4 ’18, si in fact I’d prefer to see the forward earnings yield over 5%, but Street consensus has been far too conservative since the pandemic started.

- Although there was no trading benefit from the prediction, the Q2 ’21 “bottom-up” estimate rose over $50 this week (as predicted). Nick Colas over at Datatrek was writing about this as well the last month. Readers have to realize that the Q2 ’21 bottom up estimate was $40 on 12/31/20 and $41 and change on April 2, 2021. It’s up $8 in the last 16 weeks and much of that is Q2 ’21 earnings results.

Why does this matter ? It just shows how conservative sell-side analysts have been since March, 2020.

Let’s look at some sections of the SP 500 earnings data – readers will see the trends quickly:

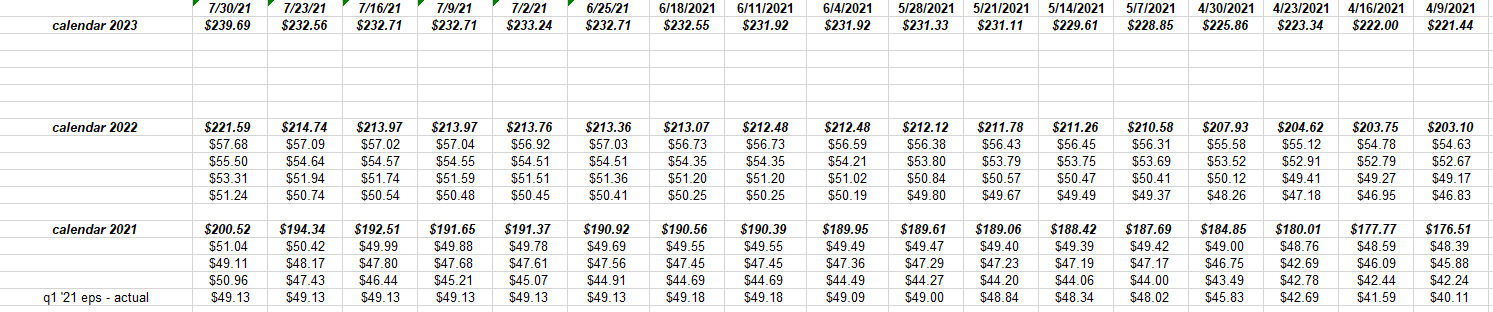

SP 500 bottom-up estimates with the calendar year estimate:

This part of the spreadsheet isn’t shown that often because it’s the base data from IBES / Refinitiv.

In particular, look at “2023” – It appeared the data was starting to rollover, now look at the latest week increase relative to the last 4 – 5 weeks. This is nothing like the patterns seen between 2011 and 2015.

The 2023 SP 500 EPS estimate is up $20 or roughly 10% since early April, 2021, when the traditional pattern is for it to be declining.

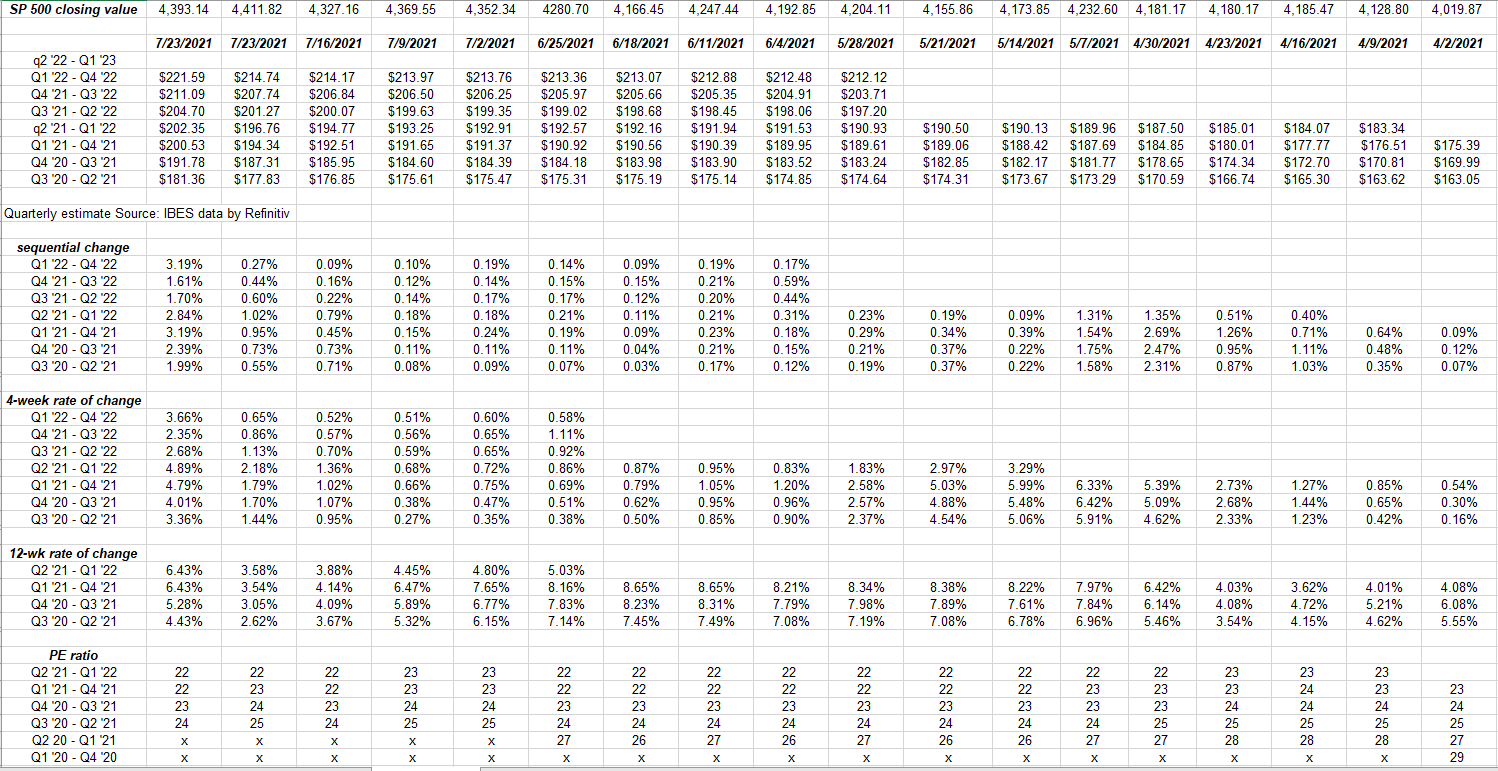

SP 500 forward earnings curve:

This spreadsheet shows the “rate of change” for the rolling 4-quarter SP 500 buckets looking out a few years.

Note the “12-week rate of change”. Like the 2023 top-down estimate in the first spreadsheet, it was worrisome the 12-week rate of change was starting to roll over, but instead the mega-cap Tech stocks this week gave a whole new life to the SP 500 forward estimates and pushed the growth rates higher.

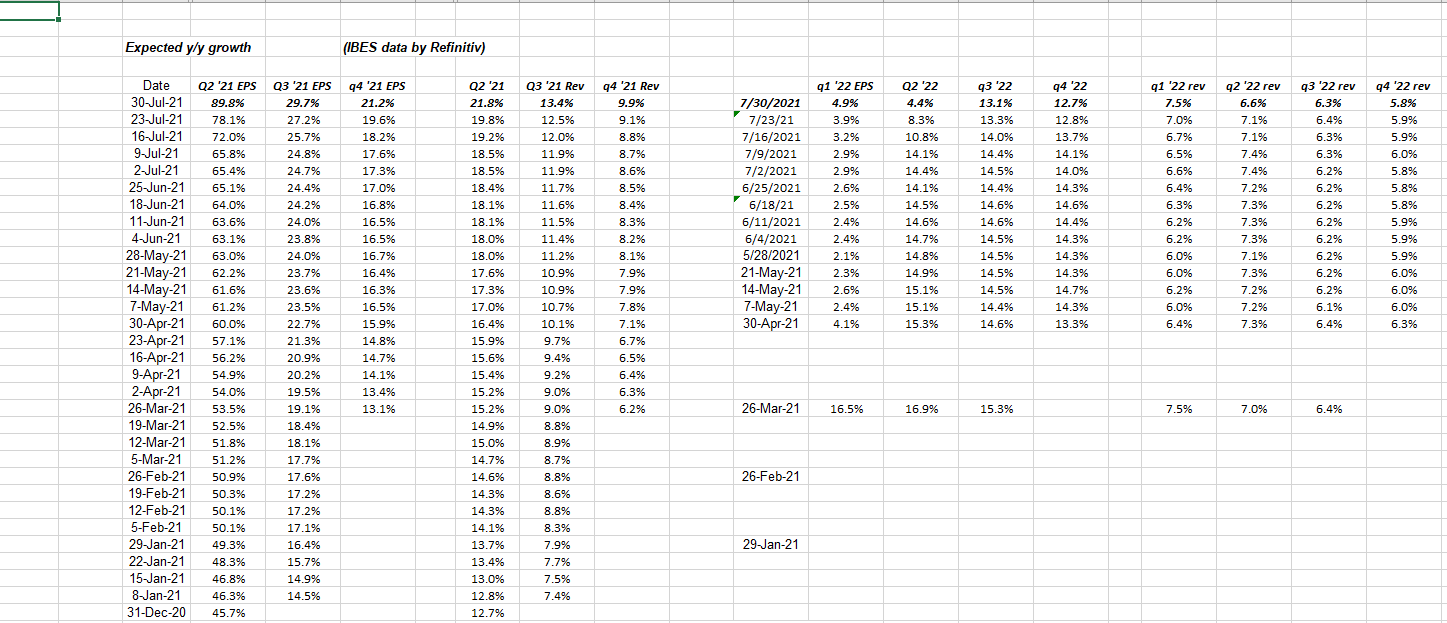

Expected growth rates for Q3 ‘Q4 ’21 and 2022

Looking at one of the favorite slices of data, now how “expected” SP 500 EPS growth for q3 ’21 has now doubled since January 1, ’21 while expected Q3 ’21 revenue has almost doubled but not quite.

This shows readers week-to-week changes in forward data, which is helpful.

Expected SP 500 EPS and revenue growth for 2022 is still in the “indecisive” stage. If you think analysts were weak-kneed about 2021, you have to assume 2022 is even more iffy. One thing for certain is that 2022 will look more normal, and more like 2019.

All the source data on this blog is from IBES data by Refinitiv. Each week I take the data and sort it out on various templates to give readers and investors a longer look at some of the trends.

Summary / conclusion: As the expected 2021 SP 500 EPS growth rate has risen to 44% as of this week, the expected 2022 SP 500 EPS growth rate has come down +11%, which is still decent growth, and really kind of remarkable after a 44% EPS growth year as this year is expecting (and 2021 could come in better or worse). The same effect happened in 2020. The full-year ’20 expected SP 500 EPS decline in July ’20 was -23%, instead full-year ’20 ended up at -14%. As the number rose for 2020 and growth was coming in better-than-expected in 2020. the analysts were not raising their 2021 EPS estimates enough and thus the growth rate was rising at a slower rate.

That was a bad forecast as this year’s earnings growth shows.

Start paying attention to 2022 expected quarterly SP 500 EPS and revenue growth rates. They will likely float around, let’s watch the trends and in particular see if any company is confident enough to give a forecast for calendar 2022.

2022 is an educated guess right now, and yet as of Sunday morning the year is only 5 months away.

The big Tech and the Big 5 SP mega-cap names are being worked on in terms of updating their forward EPS and revenue estimates. We gave a preview last week on 4 of the Big 5 that reported this past week. I updated Microsoft’s forward EPS and revenue estimates this morning and I can assure you, there are no flies on the Microsoft story. Azure is still strong and other aspects of the business keep getting better. Expect another blog post on updating the Big 5 post-earnings in the next few days.

The above trends in SP 500 EPS are very positive. Are we at “peak” SP 500 earnings ? Predictions are easy, being accurate is hard but I would say “no” given the magnitude of some of the revisions seen this week, but unexpected shocks – like Covid – can change everything. We are at peak “growth rates” but unilikely we are at peak earnings.

Take everything you read here with skepticism, and a grain of salt. You can have market corrections as SP 500 EPS estimates are stable or even rising. Today’s stock market is a function of monetary policy and fiscal policy. The Fed and the US government threw A LOT of money at the American people beginning in March ’20.

Someday that will end.

Thanks for reading.