The real question is, will the Street low-ball 2021 with guidance emanating from Q4 ’20 earnings releases the next few weeks ?

Looking at the IBES by Refinitiv data, here are the 11 SP 500 sectors ranked from the fastest-to-slowest growth rates for “expected” Q4 ’20 earnings.

Readers need to remember, the “compares” are still pre-Covid-19, which won’t really start until we see Q1 ’21 earnings in 12 weeks.

Expected Q4 ’20 EPS growth:

- Materials: +8.9%

- Financials: +6.9%

- Health Care: +4.2%

- Technology: +4.1%

- Cons Staples: +1.0%

- Utilities: -3.8%

- Real Estate: -12.1%

- Comm Services: -12.3%

- Cons Disc: -21.9%

- Industrials: -42.3%

- Energy: -101.8%

- SP 500: -7.8%

Expected Q4 ’20 revenue growth:

- Health Care: +10.1%

- Cons Disc: +8.2%

- Technology: +6.2%

- Utilities: +4.8%

- Cons Stpls: +4.5%

- Comm Serv: +2.1%

- Basic Materials: -1.1%

- Real Estate: -4.8%

- Financials: -8.8%

- Industrials: -12.2%

- Energy: -34.6%

- SP 500: -1.2%

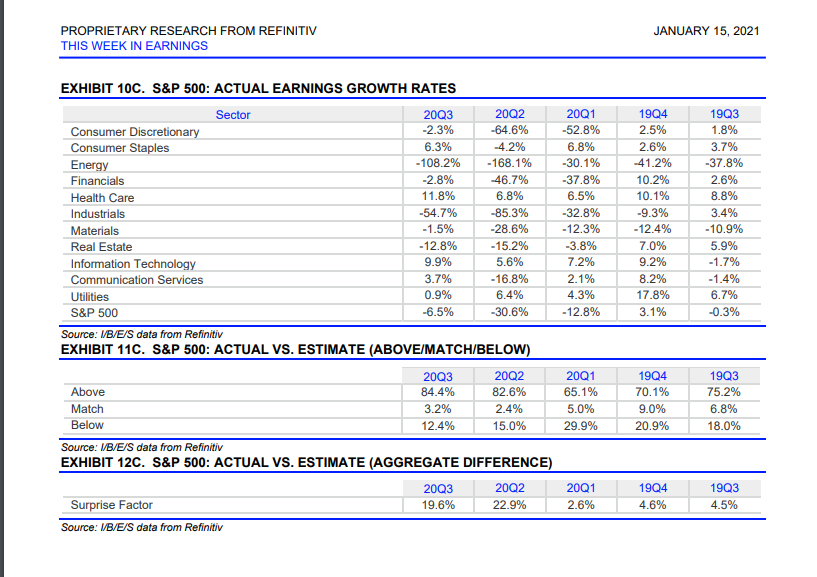

The above table is p.23 of January 15th’s “This Week in Earnings” from IBES by Refinitiv.

The bottom sections shows the “upside surprise” or “beat rates” for Q3 ’20 earnings which were substantially complete by late November ’20.

Note the 22.9% EPS upside surprise for Q2 ’20 and then the 19.6% EPS beat rate for Q3 ’20.

Even though the fiscal stimulus bonus ended late July ’20, the economic momentum likely means that Q4 ’20 EPS and revenue upside could be substantial. Even if the beat rate is just 10% or roughly half of Q3 ’20, it would mean that the Q4 ’20 “bottom-up” EPS estimate would hit at least $40 per share ($37.22 is the current estimate).

The point is Q4 ’20 earnings could still see robust upside to estimates.

It’s clear that the sell-side and Street estimates both SP 500 revenue and EPS estimates have been far too conservative since Covid-19 began.

I wonder if 2021 guidance will be the same as well.

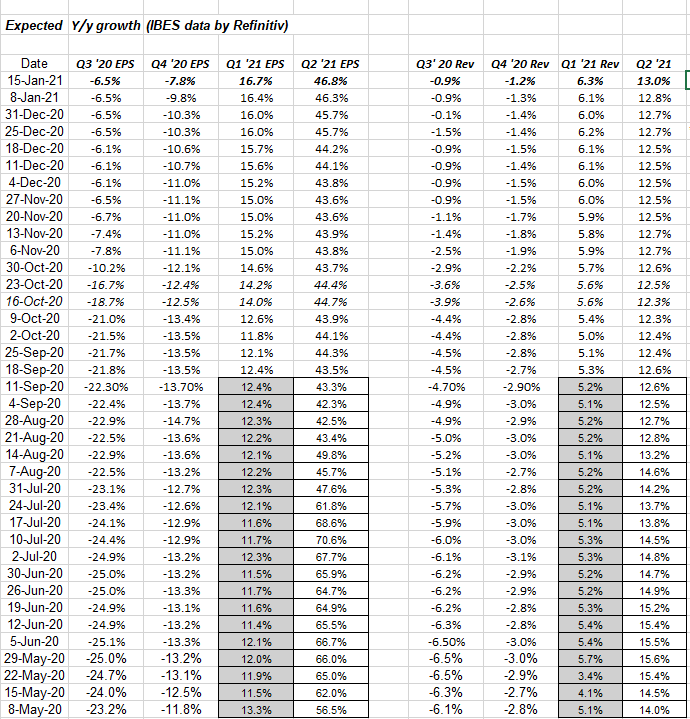

The Table of the Week:

Here is the IBES by Refinitiv data just repackaged to – in my opinion – give readers a better idea of trends in expected quarterly growth rates.

Check the improvement in “expected” Q4 ’20 growth rates for the SP 500 as well as Q1 ’21 and Q2 ’21.

The revisions are moving the right way.

Tax hikes will definitely not help.

Summary / conclusion: While the research and commentary are still being studied from Friday, January 15th’s (2021) bank earnings releases, the upside EPS surprise to JP Morgan’s results is a prime example of how the sell-side has underestimated the actual SP 500 earnings from Q2 ’20 forward.

JPM had a 43% EPS upside surprise, printing $3.79 vs the $2.75 Street estimate. As the 8th largest holding in the SP 500 by market cap, JP Morgan’s results matter.

As an example given the headline for today’s post, here are JPM’s EPS beat rates the last 3 quarters:

- q4 ’20: $3.79 actual vs $2.75 estimate for a 43% upside surprise

- Q3 ’20: $2.92 actual vs 42.23 estimate for a 31% upside surprise

- Q2 ’20: $1.38 actual vs $1.23 estimate for a 12% upside surprise

This coming week, we see another slew of financials reporting including Schwab (SCHW), and Goldman Sachs (GS) Tuesday morning before the open and then Morgan Stanley (MS) and Bank of America (BAC) later in the week, as well as “laggard” Technology like IBM and Intel later in the week.

Unfortunately, I do think the Biden Administration is poised to raise taxes, particularly the corporate tax rate back to the high 20% range.

(Take everything on this blog with a degree of skepticism given the numerous data around “forward” estimates and revision rates. This can change quickly.)

Thank for reading.