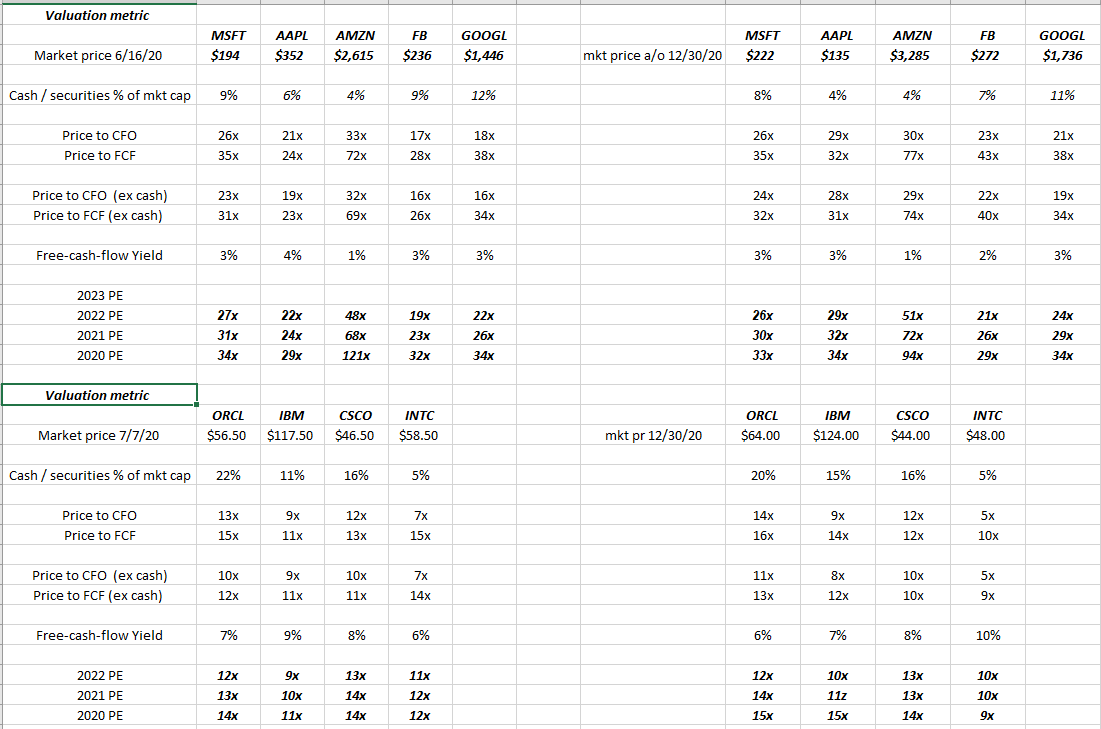

The spreadsheet is internal and draws a comparison of the Top 5 Tech names in the SP 500 versus the 1990’s growth giants or what is called today, “value” Technology.

The big 5 are still within their trading ranges that peaked in early September ’20 (September 2nd to be exact) but I wanted to make the comparison with this article written in mid-June ’20 and see if there were any material changes.

The first major observation is that Apple’s valuation expansion continued, as EPS estimates haven’t changed much since the October ’20 earnings release. This article written in mid-August demonstrates how Apple’s valuation has expanded while EPS has remained relatively constant since October earnings.

The other Big 4 maintain the same approximate valuation as they did when they were ramping this summer.

Value Tech remains value tech as Intel has really cheapened up, understandably so. Most readers probably know of Intel’s issues with 9 and 7 nanometer and how Intel has fallen behind AMD in processing and manufacturing.

Intel spends 50% of their roughly $35 billion in cash-flow on “capex” i.e. building fabs.

Intel’s expected revenue estimates in 2021 and 2022 are actually lower than what’s expected in 2020. Here’s how the current estimates look:

- 2022: $71.5 bl expected

- 2021: $70.0 bl expected

- 2020: $75.3 bl in revenue expected

Estimate source: IBES data by Refinitiv

Summary / conclusion: Growth Tech always looks expensive, and that’s still the case today but the valuations haven’t changed much since this summer for the “Big 5”. Writing bottom-up fundamental analysis for Seeking Alpha, I am more bullish on Oracle after the December ’20 earnings report, but have no change in opinion on IBM or Cisco.

The thing about Intel is – if Bob Swan reduces Intel’s capex by half – the processor giant could repurchase roughly 5% more of it’s stock every year with the $8.5 – $9 billion saved from reducing capex. Of course reducing capex means reducing it’s competitive advantage since manufacturing is (or was) Intel’s competitive edge in it’s business model.

Intel’s in a tough spot.

Microsoft is still client’s largest holding across all accounts, with all of the stocks above above owned in varying degrees. IBM and Intel are the smallest tech positions.