Even looking hard at 2021 data for changes in growth rates and quarterly estimates, there is still little evidence that the “rate of change” of SP 500 EPS is poised for problems.

But – like the old saying – risk comes on in a hurry.

The news after the close tonight that the Fed will start allowing the banks to repurchase stock has sent the Financial shares up sharply after hours. JP Morgan has already said that they are going to repurchase at least $30 billion in common stock in 2021, and Goldman’s stock is up $12 or 5% as the old white-shoe banking giant has a history of repo’ing about 5% – 10% of their outstanding market cap every year. (Here’s the Seeking Alpha article written by me in early October ’20 when the stock was trading around $200 per share.) Here is another seeking Alpha article from this website urging investors to stay with Financials given the excess capital.

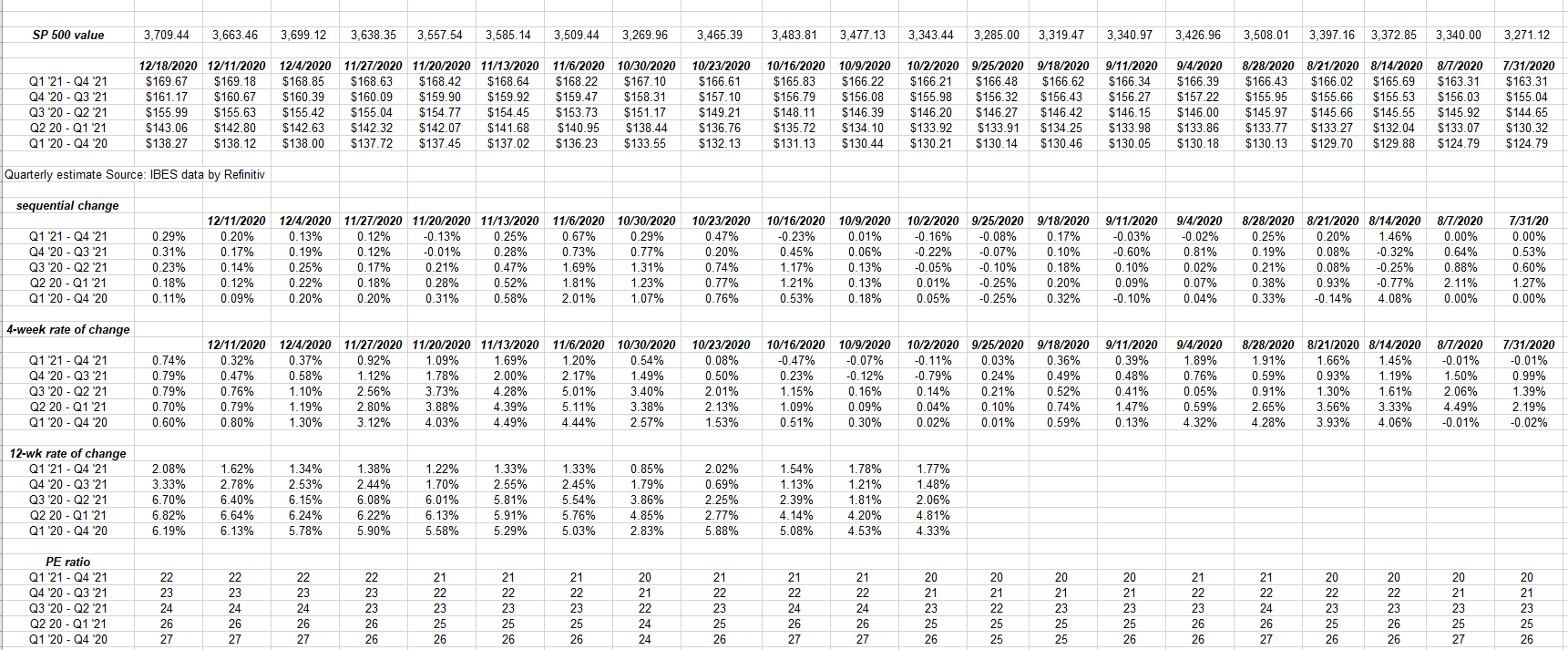

SP 500 data:

- The forward 4-quarter estimate rose again this week to $161.17 versus last week’s $160.66.

- The PE is now 23x versus the 21.5x at the start of the quarter.

- The SP 500 earnings yield is 4.34% as of this week, versus the 4.39% last week.

Forward EPS curve:

The “rate of change” for the forward EPS curve for the SP 500 shows no issues.

Expected growth for Q4 ’20 and 2021 is still subdued, much lower than Q2 and Q3 ’20. Analysts still seem cowed. The lack of stimulus and the election could have something to do with that.

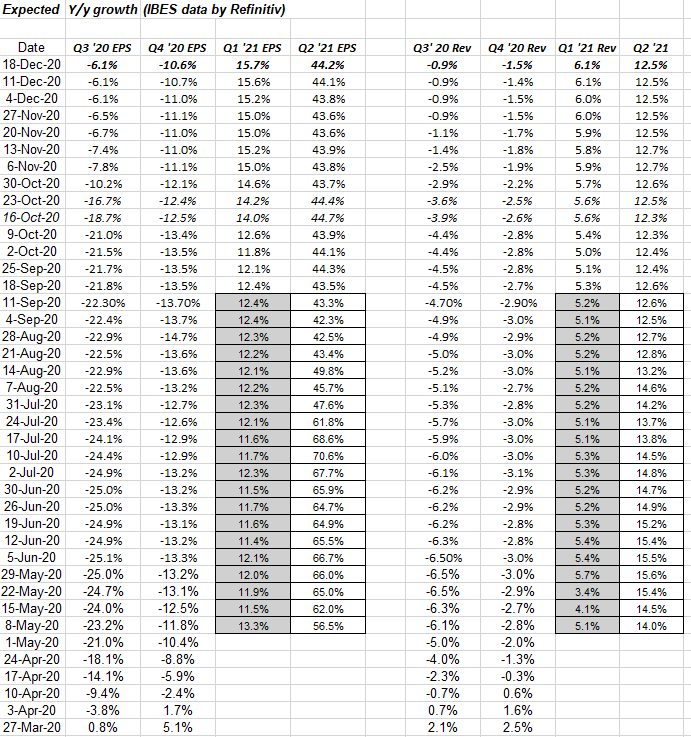

Q3 ’20 – Q2 ’21 expected EPS and revenue growth rates:

This table’s data is from Refinitiv IBES, but the layout is mine and I think it allows readers to get a better understanding of the “expected” EPS and revenue trends for forward quarters.

Expect this table to remain unchanged for the next 3 weeks as revisions might slow (except for the Financial sector).

Summary / conclusion: There isn’t much to say that hasn’t been said for the last 26 weeks. The SP 500 EPS numbers are improving i.e. showing positive revisions. With Tesla now in the SP 500 and the bank repo announcement, the next few weeks could be quiet.

The trends in estimates revisions have remained stable and constant.

The most puzzling aspect to the week is that – even with Jay Powell’s dovish analysis – the 10-year Treasury ended the week at 95 basis points. Listening to the Fed meeting minutes and comments on Wednesday, you would have thought a strong rally was in order after Powell’s thoughts were aired.

Brexit fatigue: the Brit’s voted for Brexit in July ’16, and still the EU and the UK have not hammered out an exit agreement. The negotiations have outlasted the Trump Administration.

Thanks for reading.