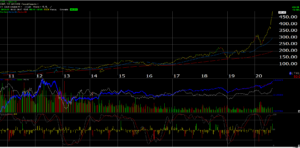

Apple’s weekly chart sits above:

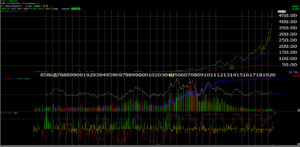

Apple’s monthly chart sits below:

Source: Worden Gold, TC200 Version 7

The charts are somewhat eerily reminiscent of the parabolic moves in Microsoft, Intel, Cisco and many other large-cap tech stocks in the first quarter of March, 2000.

Has Apple “gone parabolic”, as is sometimes heard on the Street ?

Since the majority of client’s Apple was sold in mid-2018 between $160 – $170 as the trade war heated up, and worries over an iPhone ASP nearing $1,000 (antithetical to tech hardware’s Moore’s Law), and Apple’s quality of earnings looked to be fading, the last thing i want readers to think is that this is a “sour grapes” review, but some Apple is still owned in client accounts which are tax-sensitive, thus I can’t help but wonder if now is the time to trim more of the Apple stake.

I write as much for myself to lay out the issues in black-and-white, as I do for readers to give intelligent feedback.

What prompted this review is this tweet on Friday, August 21, ’20:

The author is unknown, hence you have to question every source, but the above charts certainly give some credibility to the tweet.

Apple went public in December, 1980. 40 years later, 60% of it’s market cap has come in the 40th year.

Apple’s Valuation Expansion

Firs let’s start with the cash-flow metrics:

Based on the current share price of $497, Apple’s price to cash-flow and free-cash-flow have risen to 27x and 32x (rounded up) in the June ’20 quarter, from 10x and 13x in December, 2016.

Even Apple’s free-cash-flow (FCF) yield has fallen from 7% in December ’16 to 3% as of the June ’20 quarter.

Many analysts pointed out that Apple was buying back 6% – 7% of their shares of every quarter. That’s a healthy clip, but given the share price appreciation, that 6% – 7% has now fallen to 3%.

The nearby quarter is June 30th, ’20 and the last quarter is December ’16.

Remaining valuation metrics:

Apple’s price-to-sales ratio was 3x in December ’16 and is now 8x today.

PE expansion

Check the acceleration in the PE multiple the last 3 quarters for Apple.

Summary / conclusion: The pending stock split seems to have garnered the majority of the reasoning behind the +70.58% return on Apple YTD (source: Ycharts) but perhaps a better rationale is that Apple has successfully transformed from a tech hardware business where Moore’s Law rules, to a “services” business with much higher margins, but probably overall slower growth.

It’s interesting that Apple’s operating margin has shrunk from 29.8% in December ’16 to 21.9% in the June ’20 quarter, the Services business revenue has also slowed sequentially the last 4 quarters, and yet the stock continues this parabolic ascension.

Mr. Buffett bought Apple perfectly, just as it was on the verge of the services business coming into it’s own and the tech hardware (iPhone business) slowing down.

In mid-June ’20 this blog took a look at the Top 5 Tech stocks and their respective multiples. Apple is $150 higher than 9 weeks ago when this was written.

Take everything you read here with great skepticism and with a critical eye. I truly don’t know where Apple will stop in terms of this rapid move higher, with it’s $2 trillion market cap.

The blog is written since it imposes the discipline to walk through the numbers and do my own homework, rather than simply swallow the general themes that circulate constantly in any market.

As always feel free to weigh in with your thoughts.

Hats off to Tim Cook and the entire Apple team. The retail stores are a fantastic experience from a consumer perspective. The service is always first rate and high quality.

They should slap a “Kick Me Here” sign on my back, the next time I walk out of the Oak Brook store given the sale between $160 – $170.

Thanks for reading.