Yes, you read that headline right.

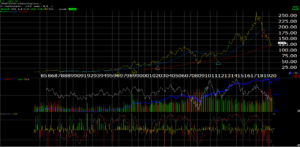

The stock is down from $270 in January ’18 to $135 today or 50% in the last 2.5 years.

The top was cut off on the above chart showing the FDX ticker, but it needed to be truncated to show the long-term oversold nature of FDX stock (bottom panel).

FDX is now as oversold as it was in late 2008, early 2009, and it has been for most of this year. However FedEx has one long-term problem that ultimately needs to be addressed. (See the bottom of the report.)

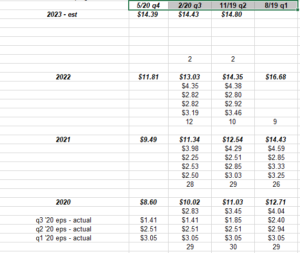

Consensus estimates per IBES by Refinitiv

- FDX is scheduled to report their fiscal Q4 ’20 tonight after the closing bell: Consensus is expecting $1.52 in earnings per share on $16.3 billion in revenue for a year-over-year (y/y) decline of -70% and -8% respectively.

- Current fiscal Q1 ’21 consensus is expecting $1.51 i n earnings per share on $16.5 billion in revenue for expected y/y declines of 41% and 3% respectively.

- Current full-year 2021 consensus is expecting $9.49 and $69.9 billion of revenue, for expected growth for fiscal ’21 (ends May ’21), +10% and +2% respectively.

Consensus EPS over last 4 quarters:

Not shown on the spreadsheet is that fiscal 2020 and 2021 EPS estimates were previously over $20 per share. Exiting the 3rd quarter of 2020, the Q4 EPS estimate was $2.83 but is now $1.52. The Q4 estimate for EPS and revenue has been falling all quarter.

Consensus EPS growth rates:

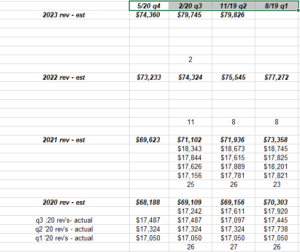

Consensus revenue est’s over last 4 quarters:

The consensus revenue estimate for Q4 ’20 (tonight’s report) was $17.2 billion exiting the March ’20 report thus tonight’s revenue estimate is lower by $1 billion over the last 3 months.

Consensus revenue growth rates:

Readers can see actual trends and growth rates for FDX EPS and revenue for the next few years.

Free-cash-flow: the one long-term problem for FDX:

The bordered area on the cash-flow statement above shows the dearth of free-cash that FDX was generating, even well before COVID-19. The transport giant always had a constrained dividend and a limited share repurchase program because of the limited free-cash-flow, and that issue has only been greatly aggravated with Covid-19 and the global slowdown.

I included the “quality of earnings” segment of the cash-flow statement to show cash-flow coverage of net income (bottom of spreadsheet) and while cash-flow coverage is robust, there is no free-cash coverage of net income.

This is a longer-term issue for Fed-Ex. Long term debt issuance is now 50% of capital and it might constrain FDX’s growth exiting the global recession.

Summary / conclusion: Yesterday, over on Seeking Alpha, Micron Technology’s earnings release was previewed (FedEx’s is being done on this blog due to time constraints) but it occurred to me this morning that FedEx and Micron are far more similar than you think. In positive points of the cycle – for Micron the DRAM / NAND pricing or demand cycle, while FedEx it’s the global shipping and business cycle – both companies make extraordinary profit and returns on capital at the cycle peaks, and then in effect destroy capital at the cycle bottoms. Micron has been fixing that issue, FedEx has not, although Fred Smith said a few quarters back “free-cash-flow is coming” not knowing that the global pandemic and COVID-19 would decimate world economies.

Capex as a % of cash-flow has exceeded 100% for FedEx the last few years and even during the better growth years of 2010 – 2015, and then 2017 – 2018, capex as a percentage of cash-flow was still greater than 75%.

That level of capex to cash-flow is like running a marathon with a piano on your back.

Ultimately, I think the solution for FedEx is that they must become leaner and meaner and boost that operating profit margin from 10% into the mid-teens and then sustain positive returns even during difficult times.

FedEx has been hit with the 1-2 punh of the China Trade War and then Covid-19 so I’m giving them a little leeway to work through the “macro”.

Select clients have small positions in FedEx, with a cost basis from $177 down to $160. We’ll gradually lower the cost basis for existing owners and add to other accounts as the stock stays above the 200-month moving average and some of the Express and Ground metrics start to improve.

The 200-month average must hold technically at $120 – $124 per share. The late March low was $88 – $89 per share.

Thanks for reading.