Next week, readers will see the “quarterly bump” in the forward 4-quarter estimate with the key metric expected to rise from the $127.98 this week to the low $140 area as the forward estimate period will cover Q3 ’20 through Q2 ’21.

Looking at the forward SP 500 EPS curve, the revisions this week, turned slightly negative reversing some of the progress made the lst 4 – 6 weeks, but it shouldn’t worry too many readers yet.

As readers can see the latest week’s revisions are a little more negative than last week.

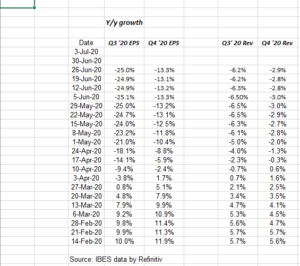

Q3 and Q4 ’20 expected SP 500 EPS and revenue growth:

This chronological progression should be helpful to readers since it shows the quarterly estimates for Q3 and Q4 ’20. Most investors are keyed into Q2 ’20 earnings which start being reported in two weeks.

Summary / conclusion: What was interesting about Nike’s report and it was a line picked up in one of the sell-side research reports, is that the companies with the May ’20 quarter end are reporting the full brunt of the Covid-19 economic impact, versus the first quarter ’20 reports which had a decent January and February in terms of “normal” economic activity, and then the wheels came off the cart in March, ’20. The 2nd quarter earnings reports ended June ’20 will have a horrible April, and then should see slightly better results in May and June ’20.

Those May ’20 quarter end reports – like FedEx (FDX) and Micron (MU) this coming week – both have a May ’20 quarter end (or in the case of FedEx, a May ’20 year-end.

There isn’t much to say this week, other than the big reports start with the Financials around July 10, 20 and I’d expect revisions to be contained until then.

From a “macro” perspective, I do think the President and Congress will agree on a 4th fiscal stimulus package, which Jay Powell has strongly recommended and the faster the better in my opinion. That will likely help sustain consumer spending – like the unemployment kicker did – and should help sustain household income through year-end.

Take everything on this blog with a grain of salt and a high degree of skepticism. These are simply my own opinions.

The blog will gradually return to the old metrics of PE, earnings yield, etc., as the “rate of change” importance fades.

Thanks for reading.