Many thanks to Jeff Miller at www.dashofinsight.com for picking up yesterday’s SP 500 Earnings Update post on his blog this weekend.

———————–

So much of the mainstream financial media focuses on the stock market, and yet the corporate bond markets, and that would include securitized product and even municipal bonds, have (in my opinion) a huge information vacuum for the smaller advisor or individual investor.

The corporate bond market has typically been an institutional market that the largest mutual fund firms and sell-side firms like Goldman Sachs and Morgan Stanley dominate.

The point being that I’ve tried to be alert for good “relative value” analysis in terms of corporate bonds, not so much to be able to buy individual bonds for client accounts, but to improve my own perspective on corporate credit, if only to be able to have informed discussions with clients.

The St. Louis Fed (FRED) has some decent spread-related charts, and even ICE (Intercontinental Exchange) has developed a website dedicated to corporate, structured and municipal bonds that I hope ICE continues to develop over time, with more commentary and continued insights.

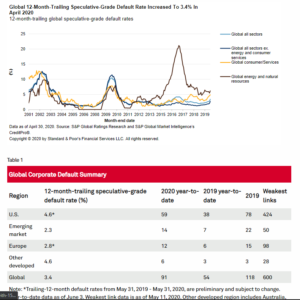

Another helpful source of credit info is S&P Global Ratings. Here is an interesting chart from their early June, 2020 default study:

Every Saturday morning since late March, 20, when a nice percentage of client money market funds was transferred to corporate credit risk, this spreadsheet has been updated with “YTD returns” for the various corporate bond funds being used for clients:

Readers can see the dramatic improvement in returns for these various corporate bonds funds since late March ’20.

The Blackrock Strategic Income Opportunities Funds (BASIX) now has a positive return YTD. The fund is managed by Rick Rieder, Blackrock’s fixed-income CIO. It’s done a fabulous job navigating the challenges presented by COVID-19 and the impact on the US economy.

The weekly Bespoke Letter published this Friday, June 19th, 2020, discussed the improvement in credit spreads with historical context:

Note the 2nd chart i.e. the 50-day rate of change in corporate credit spreads. If you wait around waiting for economic data and default data to improve, you would have missed a big part of the credit spread improvement in both 2008 – 2009 and then again in March -April, 2020.

Summary / conclusion: Ultimately, we will only know the 2020 corporate bond default rate in hindsight, but as readers can see from the corporate spread detail, if you wait around to see the turn in either economic data or Fed policy, you’ll likely miss a good part of the potential return available in corporate bond funds. While it may seem “unsophisticated” to use bond funds for client bond allocations, when dealing with high yield debt and even corporate credit at the lower-end of the investment-grade credit spectrum, the loan covenants and the risk of credit rating downgrades, is – in my opinion – better managed by the larger funds credit staffs and portfolio managers.

Fed Chair Jay Powell noted in last week’s Fed call that the Fed will likely keep interest rates near zero until 2022, but my own guess is much depends on the 2020 Presidential election, and its outcome. The Congressional composition matters too.

This blog and blogger continue to be comfortable over-weighting corporate credit risk and high-yield municipal bonds, but the exposure will be evaluated as the 2020 Presidential election nears.

For me personally, there is little value in the 10-year Treasury trading at 70 basis points. The only redeeming feature of the Treasury yield curve, all of which is underwater (negative yields) in terms of “inflation-adjusted” returns, is that Treasuries are negatively correlated to the SP 500, so in times of sharp corrections like 2008 – 2009, early 2016, and now March – April ’20, even at very low nominal Treasury yields, investors can get total return as money flows to risk-free (credit) assets.

Corporate credit risk stills look good for the next 3 – 6 months.

As always, take the opinions on this blog with a substantial grain of salt and with great skepticism. Evaluate all market opinions in light of your own financial profile.

Thanks for reading.